Beating inflation: Are the Fed’s dreams gold’s worst nightmare?

While investors remain happy-go-lucky, fundamental data for gold and silver is now worse than in 2021. Is this the last chance to come back to earth?

As another week comes to a close, the winds of change are blowing across the financial markets. However, while many investors and analysts can see only sunny days ahead, fundamental storm clouds should rain on their parade over the medium term, and it’s quite possible that it’s going to happen shortly.

To explain, this week culminated with the USD Index soaring above 100, the U.S. 10-Year real yield hitting a new 2022 high, and Goldman Sachs’ Financial Conditions Index (FCI) hitting its highest level since the global financial crisis (GFC). However, the PMs paid no mind yet. In fact, investors across many asset classes continue to ignore the implications of these developments. So far.

With sentiment poised to shift when the economic scars begin to show, the “this time is different” crowd may regret not heeding the early warning signs. For example, the Bank of Canada (BoC) announced a 50 basis point rate hike on Apr. 13., and with the Fed likely to follow suit in May, the domestic fundamental environment confronting the PMs couldn’t be more bearish.

Please see below:

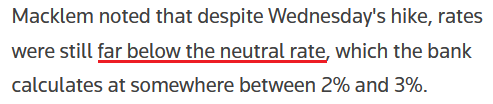

Moreover, BoC Governor Tiff Macklem (Canada’s Jerome Powell) said: “We are committed to using our policy interest rate to return inflation to target and will do so forcefully if needed.”

Furthermore, while he added that the BoC could “pause our tightening” if inflation subsides, he cautioned that “we may need to take rates modestly above neutral for a period to bring demand and supply back into balance and inflation back to target.”

However, with the latter much more likely than the former, the BoC’s decision is likely a preview of what the Fed should deliver in the months ahead.

Please see below:

To that point, while investors continue to drown out officials’ hawkish cries, I warned on Apr. 13 that the Fed knows full well about the difficulty of the task ahead. I wrote:

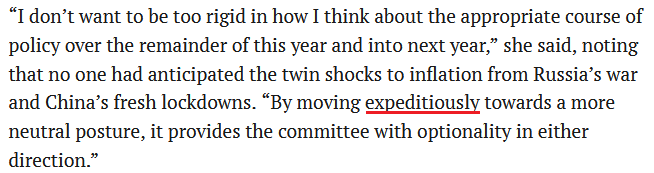

Fed Governor Lael Brainard said on Apr. 12: “Inflation is too high, and getting inflation down is going to be our most important task.”

She added: “I think there’s quite a bit of capacity for labor demand to moderate among businesses by actually reducing job openings without necessitating high levels of layoffs.” As a result, she’s telling you that Fed officials will make it their mission to slow down the U.S. economy.

With phrases like “capacity for labor demand to moderate” and “reducing job openings” code for what has to happen to calm wage inflation, the prospect of a dovish 180 is slim to none. As such, this is bullish for real yields and bearish for the PMs.

More importantly, notice her use of that all-important buzzword?

And:

Moreover, where do you think she got it?

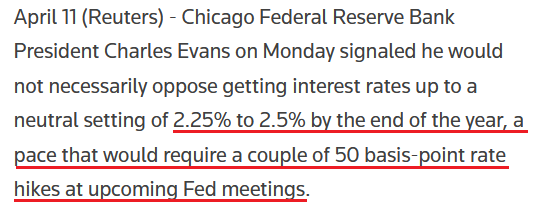

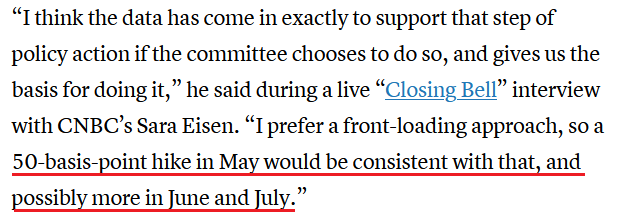

Echoing that sentiment, Chicago Fed President Charles Evans (a relative dove) said on Apr. 11 that more than one 50 basis point rate hike could be on the horizon. “Fifty is obviously worthy of consideration; perhaps it’s highly likely even if you want to get to neutral by December.”

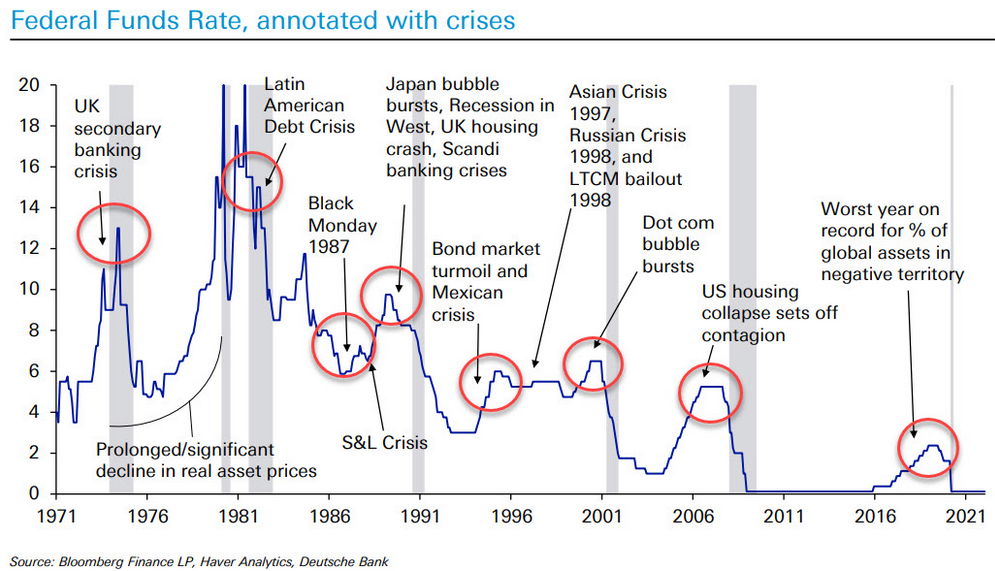

As a result, with the USD Index and the U.S. 10-Year real yield already soaring, what do you think will happen if the Fed pushes the U.S. federal funds rate “to neutral by December?”

Please see below:

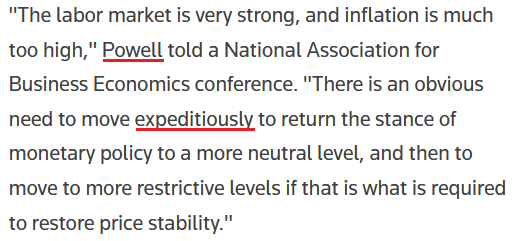

Even more hawkish, Fed Governor Christopher Waller said on Apr. 13: “I think we’re going to deal with inflation. We’ve laid out our plans. We’re in a position where the economy’s strong, so this is a good time to do aggressive actions because the economy can take it.”

He added: “I think we want to get above neutral certainly by the latter half of the year, and we need to get closer to neutral as soon as possible.”

As a result:

Now, if we presented these quotes to the permabulls, they would say: “So what? We already know that the Fed is going to raise interest rates.”

However, while a higher U.S. federal funds rate is now the worst-kept secret, the impact on U.S. economic growth is far from priced in. With investors assuming the Fed will normalize inflation without hurting the U.S. economy, they are positioned for an unrealistic outcome. Stagflation, anyone?

Moreover, with the gold and silver prices ignoring everything the Fed throws at them, they’re attempting to re-write the history books.

However, with Brainard and Waller telling you that their goal is to create a bullish environment for the USD Index and the U.S. 10-Year real yield, the PMs have fought this battle before and lost this battle before.

To explain, I wrote on Apr. 6:

Please remember that the Fed needs to slow the U.S. economy to calm inflation, and rising asset prices are mutually exclusive to this goal. Therefore, officials should keep hammering the financial markets until investors finally get the message.

Moreover, with the Fed in inflation-fighting mode and reformed doves warning that the U.S. economy “could teeter” as the drama unfolds, the reality is that there is no easy solution to the Fed’s problem. To calm inflation, it has to kill demand. As that occurs, investors should suffer a severe crisis of confidence.

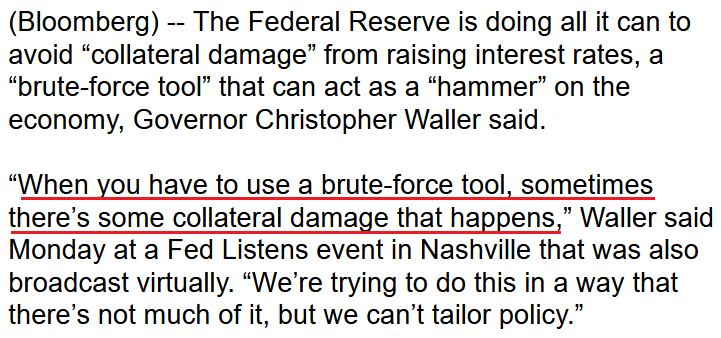

To that point, Fed officials aren’t even pretending anymore. Waller said on Apr 13:

“All we can do is kind of push down demand for these products and take some pressure off the prices that people have to pay for these products. We can’t produce more wheat, we can’t produce more semiconductors, but we can affect the demand for these products in a way that puts downward pressure and takes some pressure off of inflation.”

Likewise, Waller was even more realistic when he spoke on Apr. 11: He said:

“With housing, can we cool off demand for housing without tanking the construction industry? Can we cool down the labor demand without causing employment to fall? That’s the tricky road that we’re on.”

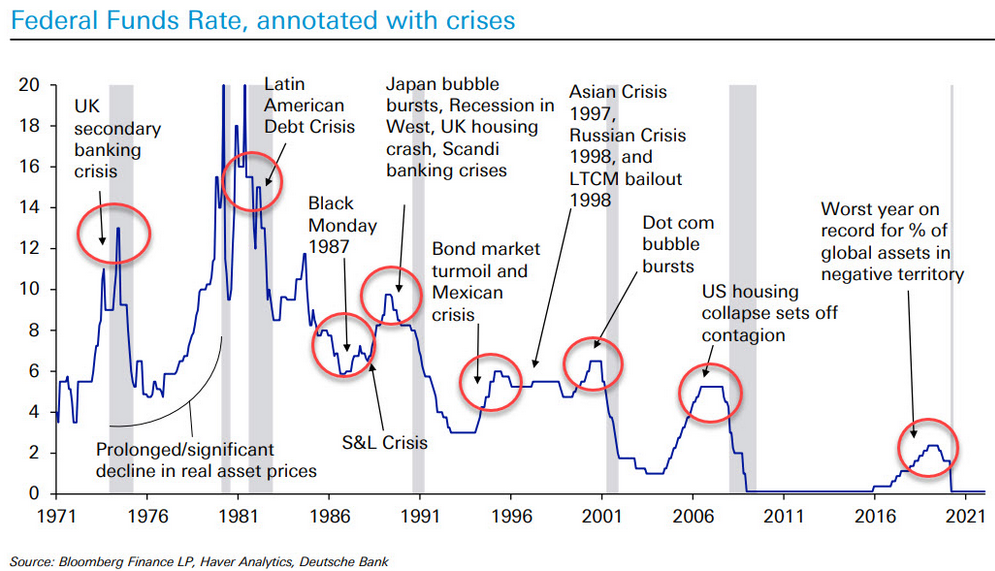

As a result, while Fed officials understand how difficult it will be to normalize inflation, investors remain in la-la land. However, when the “collateral damage” eventually unfolds, the shift in sentiment should result in the profound re-pricing of several financial assets.

Please see below:

Thus, investors’ uninformed state of denial will likely seem obvious in the months ahead. (Yes, I know, it’s difficult to remain rational while surrounded what’s irrational, and that’s the very thing that makes investing “simple, but not easy”). Moreover, while Macklem cautioned that the BoC could “pause our tightening” if inflation subsides, the same rule applies to the Fed. However, with inflation still raging, the Fed and the BoC are unlikely to change their hawkish tones anytime soon.

Case in point. The U.S. Bureau of Labor Statistics (BLS) released the Producer Price Index (PPI) on Apr. 13.,and with outperformance across the board, green lights were present for all of the wrong reasons. For context, the gray figures in the middle column were economists’ consensus estimates.

Please see below:

Likewise, the NFIB released its Small Business Optimism Index on Apr. 12. The report revealed:

“The NFIB Small Business Optimism Index decreased in March by 2.4 points to 93.2, the third consecutive month below the 48-year average of 98. Thirty-one percent of owners reported that inflation was the single most important problem in their business, up five points from February and the highest reading since the first quarter of 1981. Inflation has now replaced ‘labor quality’ as the number one problem.”

How about this divergence?

“Owners expecting better business conditions over the next six months decreased 14 points to a net negative 49%, the lowest level recorded in the 48-year-old survey.”

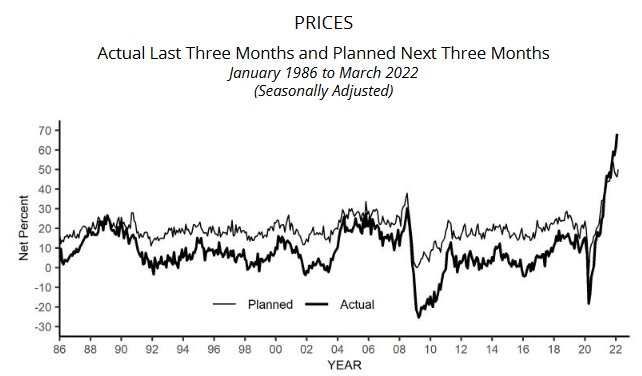

“The net percent of owners raising average selling prices increased four points to a net 72% (seasonally adjusted), the highest reading recorded in the series.”

Moreover, “a net 50 percent plan price hikes (up 4 points).”

Please see below:

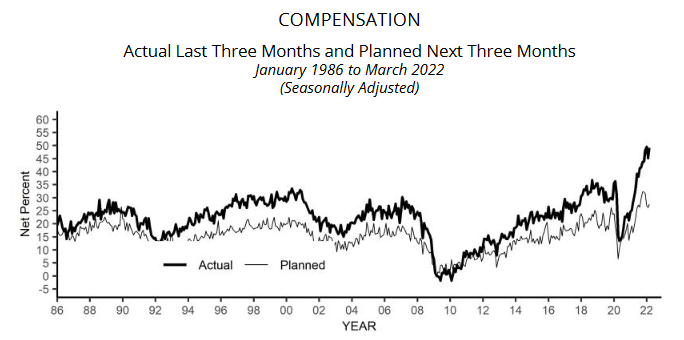

On top of that, “a net 49 percent reported raising compensation, down 1 point from January’s 48-year record high reading. A net 28 percent plan to raise compensation in the next three months, up 2 points from February.”

Please see below:

Thus, while the Fed hopes to rein in inflation, U.S. small businesses plan more price hikes and wage increases than in February. Therefore, officials’ hawkish intentions are not nearly hawkish enough. As a result, the medium-term outlook for the U.S. federal funds rate, the USD Index and the U.S. 10-Year real yield couldn’t be more bullish. As mentioned, let’s not forget how optimism often turns to pessimism when the drama unfolds.

The bottom line? Investors lack the foresight to see how the Fed’s rate hike cycle will likely unfold. Moreover, with Fed officials warning of the “collateral damage” that occurs when they curb demand to reduce inflation, the permabulls have simply closed their eyes and covered their ears. However, when sentiment is built on a foundation of sand, it often collapses when reality re-emerges.

In conclusion, the PMs rallied on Apr 13 as momentum remains the name of the game. However, while sentiment remains robust, gold, silver, and mining stocks’ fundamentals are worse now than at any point in 2021. As a result, history shows that not only are the current prices unsustainable, but profound drawdowns are required for the PMs to reflect their intrusive values.

What to Watch for Next Week

With more U.S. economic data to be released next week, the most important ones are as follows:

- Apr. 21: Philadelphia Fed manufacturing index

With the regional data providing early insight into April’s inflation dynamics, continued price increases will put more pressure on the FOMC.

- Apr. 22: S&P Global’s U.S. manufacturing and services PMIs

Unlike the Philadelphia Fed’s index, S&P Global’s data covers the entire U.S. As a result, the performance of growth, employment, and inflation will be of immense importance.

All in all, economic data releases impact the PMs because they impact monetary policy. Moreover, if we continue to see higher employment and inflation, the Fed should keep its foot on the hawkish accelerator. And if that occurs, the outcome is profoundly bearish for the PMs.

(By Przemyslaw Radomski)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

{kind=link}

{kind=link}

Comments