Bear market leaves bond investors with few places to hide

It’s been a harrowing 12 months for global bond investors, culminating in a fall into a rare bear market. And there are few signs of a reprieve soon.

Double-digit losses have been the norm for fixed-income investors in 2022, whether it be by bond duration, type of debt or industry of issuer. More declines may be on the horizon as central banks press on with efforts to tame the highest inflation in decades.

“There is still some pain to come,” said Pauline Chrystal, a portfolio manager at Kapstream Capital in Sydney. “The Fed, in particular, is very committed to prioritizing inflation as opposed to being concerned about recession.”

Here is a look at how losses have been shared out across the different debt classes:

Treasuries globally have performed worse than corporate bonds and securitized debt securities since early 2021. US government bonds have been under pressure of late as the Federal Reserve embarked on its most aggressive tightening campaign since the 1980s, and resolved to continue raising rates to bring inflation back to its 2% target.

Government debt has been the worst hit, given a sizable chunk of the market was offering negative yields a year ago. The stockpile of notes with sub-zero yields exceeded $15 trillion then, with investors paying to hold 10-year German bunds and Japanese bonds, along with two-year Italian securities.

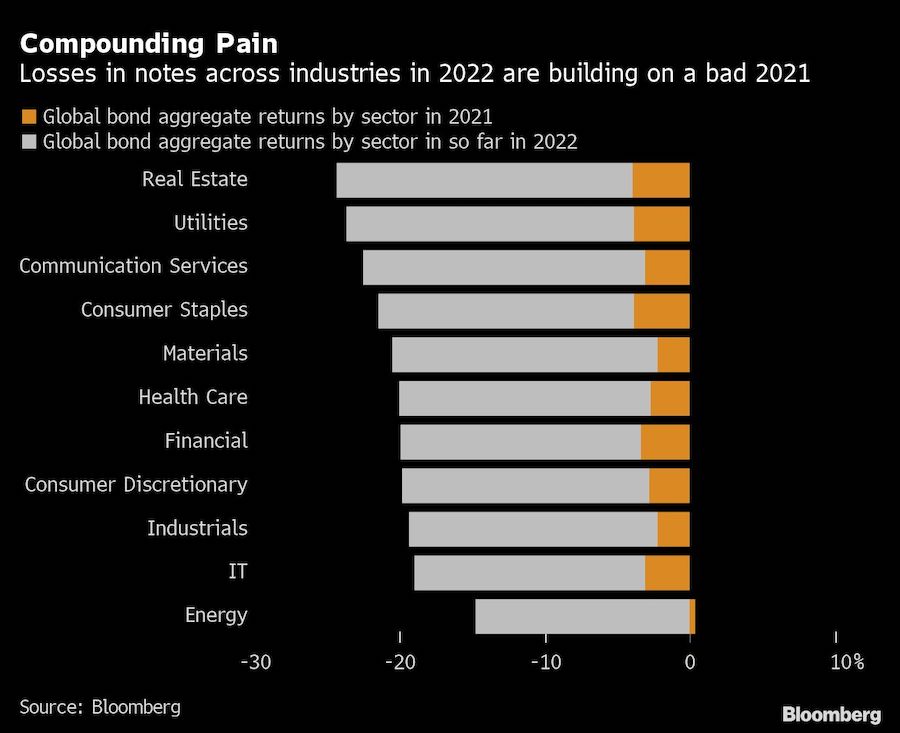

Across almost all sectors, losses in 2022 have come on top of those racked up last year. Energy-related bonds have suffered the smallest declines during the slump.

Bonds denominated in European currencies have underperformed in 2022, after the continent’s energy crisis increased the odds of a recession. Large swings in currency markets, driven by the highest inflation in decades in many nations, have compounded losses for investors tracking a dollar portfolio.

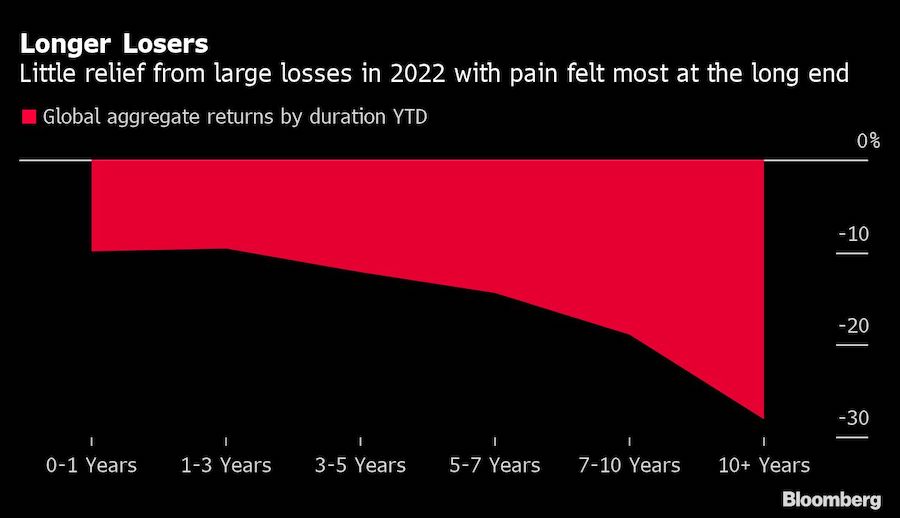

Even shorter-duration bonds haven’t been spared, although their year-to-date losses of close to 10% are far below the near 30% drop for notes with maturities of above 10 years.

High-yield bonds have lost less globally than their investment-grade peers since early 2021. This suggests that investors aren’t pricing in a deep recession, and the notes offer some value as a buffer against rising benchmark rates.

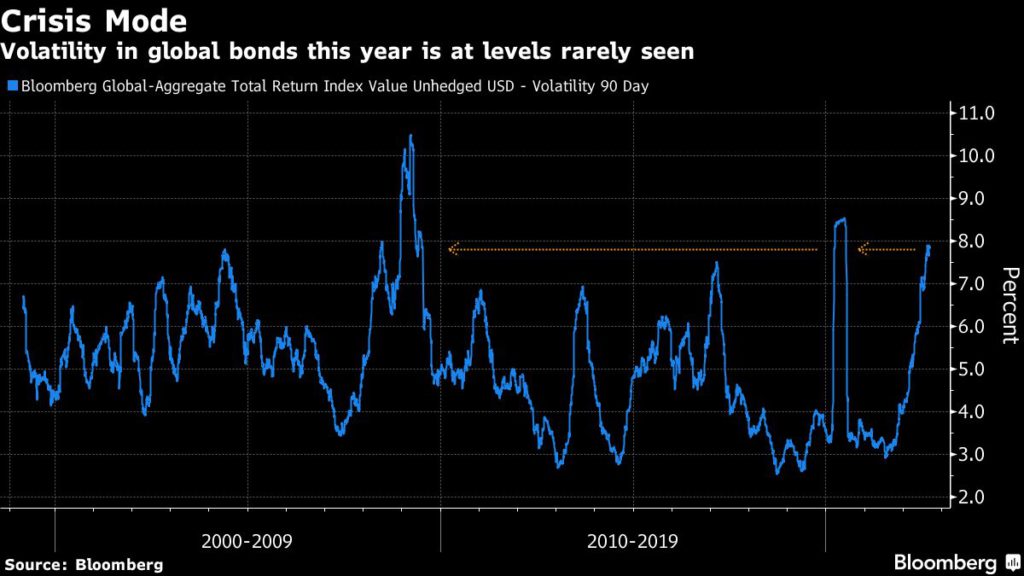

The global increase in borrowing costs has whipsawed debt markets, with volatility soaring to levels last seen in July 2020. With central banks yet to declare victory in the battle against inflation, bond investors may have to gear up for more turbulence ahead.

(By Finbarr Flynn and Garfield Reynolds)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments