Barrick falls behind rivals as No. 2 miner misses boost from bullion boom

Most of the world’s top gold miners have seen their shares surge this year as bullion prices hit repeated record highs. Not Barrick Gold Corp.

Missed production targets, higher operational costs and political turbulence at mines in Africa and Asia have investors turning increasingly sour on the world’s second-biggest gold producer. On Thursday, Barrick posted gold output that missed analysts’ estimates for the 11th straight quarter.

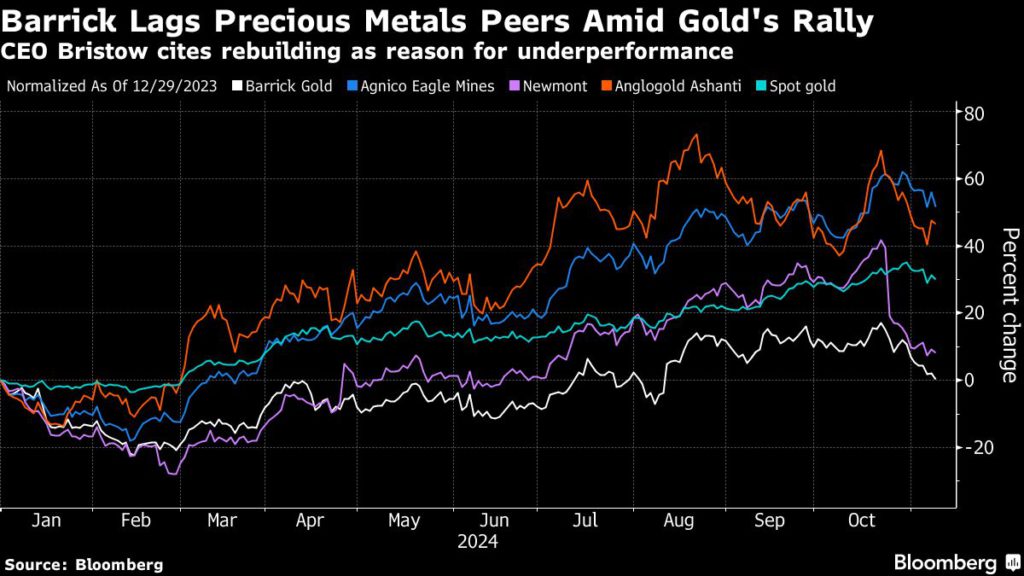

Barrick is one of several miners that have struggled to capitalize on the bullion boom amid higher mining costs and weaker output. But among the largest precious metal producers — Newmont Corp., Agnico Eagle Mines Ltd. and AngloGold Ashanti Ltd. — Barrick has routinely underperformed, with its shares virtually unchanged since the beginning of January. Gold, meanwhile, has soared 30% in the period.

Chief executive officer Mark Bristow’s explanation: “We’re rebuilding the business.”

Barrick has spent years working to improve its balance sheet after amassing debt from acquisitions. Bristow, who joined as CEO in 2019 as part of the Canadian company’s takeover of Randgold Resources Ltd., has paid down that debt while exercising restraint in dealmaking. He has also pursued diversification into copper.

Bristow’s explanation doesn’t seem to be winning over investors. Some of Barrick’s top investors have sold off shares while boosting stakes in competitors. Blackrock Inc., one of Barrick’s biggest shareholders, reduced its stake while buying into Agnico Eagle and Newmont, according to regulatory disclosures in November. Other major investors like Van Eck Associates Corp., First Eagle Investment Management LLC and Capital Group Inc. also trimmed their holdings in recent months.

Barrick isn’t alone in drawing scrutiny from shareholders whose expectations have been lifted by gold’s rally. Larger rival Newmont suffered its biggest one-day stock drop since 1997 last month after posting disappointing quarterly earnings.

Bristow said investors are undervaluing Barrick’s stock. “It’s our job as managers to make sure that the market properly understands us,” he said in an interview.

Barrick’s strengths lie in its complex of productive mines in the US, along with huge operations in Papua New Guinea and Mali. It has diversified through expanding in copper just as the global energy transition boosts demand for the wiring metal. The company has relatively little debt.

Still, Barrick has faced setbacks in its attempts to match production to cost targets. Its Nevada operations, co-owned with Newmont, need significant infrastructure repairs, and labor costs have increased.

“We’re still not as efficient in Nevada as we are in some of our African mines,” Bristow said. “But we’re getting there.”

Africa is also a chief concern among investors, notably in Mali, where the military government is threatening to withdraw the company’s right to operate a mine. In the Dominican Republic, an extension to Barrick’s Pueblo Viejo mine has taken longer than expected to complete.

Operating issues at the Nevada mines and Pueblo Viejo will “persist into 2025 and are expected to have an impact on production,” Bank of Nova Scotia analyst Tanya Jakusconek wrote in a Friday note.

The setbacks have ceded territory to rivals. Newmont solidified its position as the world’s top producer with its acquisition of Newcrest Mining Ltd. last year, significantly boosting its production of gold and copper. Agnico Eagle, once a small gold producer, surpassed Barrick’s market capitalization for the first time early this year. Barrick’s annual gold output, meanwhile, is at its lowest level since 2000.

Barrick has regularly missed Wall Street’s expectations for important measures such as revenue and gold production in its quarterly results — including last week’s financial disclosures.

“Barrick has a lot of challenges to overcome,” said Rick Rule, a US investment adviser and shareholder. “At the very least, it would be useful if the quarterly performance matched guidance.”

(By Jacob Lorinc)

More News

Contract worker dies at Rio Tinto mine in Guinea

Last August, a contract worker died in an incident at the same mine.

February 15, 2026 | 09:20 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

John Doe

Nowhere does this article address whether Barrick’s poor performance threatens Mark Bristow’s job security. If he gets to keep the CEO role forever regardless of profitability, how about an article discussing the company’s credibility?