An eye-watering squeeze in copper ore is firing up the bulls

An unprecedented squeeze in the market for copper ore has fired up bullish investors and helped drive prices to the highest in nearly two years.

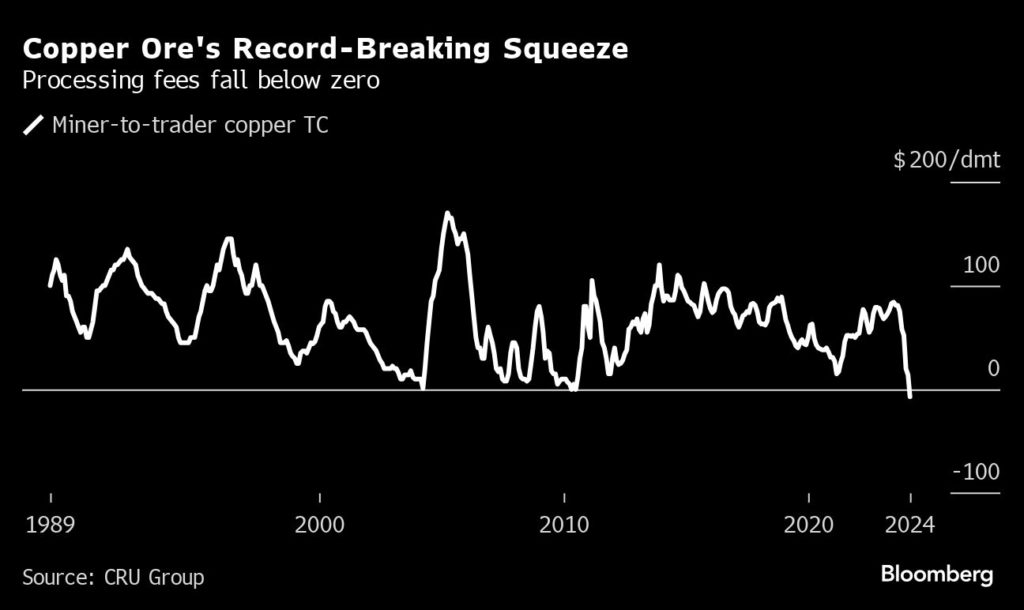

The market for semi-processed copper ore, known as concentrates, has never been as tight as now, according to several veteran traders with decades of experience. Across the market, traders and smelters are paying roughly the same price for copper ore as the copper contained in it would fetch once processed — a highly unusual situation that points to a shortage of immediately available supplies.

“Copper has been coiled up like a spring,” said Craig Lang, principal analyst at CRU Group. “I have a lot of conviction in the copper price increasing. It’s a direct follow-on from the impact of raw materials shortages.”

The dramatic move in copper concentrates has helped inspire a chorus of bullish investment bank forecasts and a wave of buying by investors. As miners, traders and hedge fund managers descend on Santiago in Chile for the annual Cesco Week gathering, the question being fiercely debated on trading floors and in boardrooms is: could this be the big one?

While the trade in concentrates is a niche market only accessible to miners, smelters and physical traders, investors have lifted the number of bullish positions they hold in copper derivatives on the London Metal Exchange to the highest since at least 2018. Bullish positions in New York have also jumped, although they remain far below the record level seen in 2020.

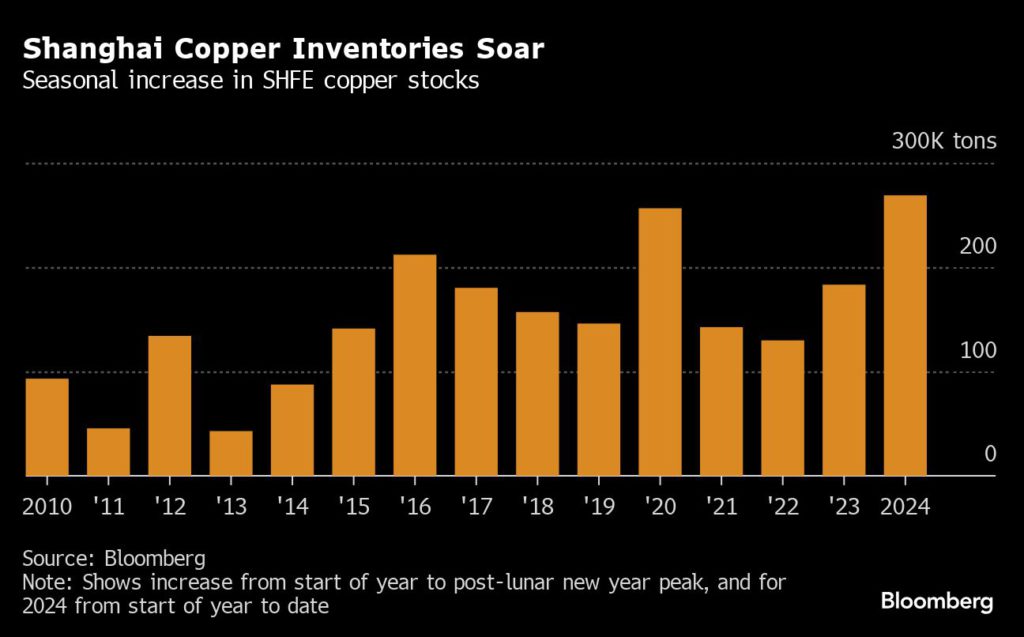

Still, even some longstanding copper bulls aren’t sure that this is the beginning of a major move higher. Copper touched a 22-month high of $9,590.50 a ton on Friday, but remains 12% below the record high of $10,845 reached in March 2022. And while demand for copper ore is red hot, traders say that the real-world market for refined metal is much softer, particularly in China.

Copper inventories in Shanghai have risen by the most ever in the seasonally sluggish period over lunar new year, and premiums for copper metal in the world’s biggest consumer have plunged 73% since December. On the LME, spot prices are trading at the biggest discount to three-month forward prices in at least 30 years – a situation known as contango that is indicative of a well-supplied market.

“Ironically we have been rallying at a time when refined metal stocks are at recent highs,” said David Lilley, chief executive of hedge fund Drakewood Capital Management Ltd.

For several years, investors, traders and mining executives have been touting the potential for copper to soar as demand is driven higher by the energy transition, while investment in new mine supply struggles to keep up. Together with signs of improving manufacturing sentiment, the extreme move in the copper concentrate market has led some to ask if now is the beginning of a bull run that could see copper smash previous records.

“We believe copper’s second secular bull market this century is taking hold,” Max Layton, head of commodities research at Citigroup Inc. said in a note to clients this week, predicting prices would average $10,000 a ton in the final three months of 2024 and $12,000 in 2026.

The squeeze in copper ore has been building for several months, driven by the surprise closure of First Quantum Minerals Ltd.’s Cobre Panama mine, followed by downgrades to production guidance from Anglo American Plc. Codelco, the world’s top producer, has also seen production slump to quarter century lows.

An index of deals compiled by CRU shows the discount for copper ore – known as treatment and refining charges, or TC/RCs – has fallen to a record low in data going back to 1989. In some cases traders have been paying a premium, according to CRU’s Lang.

Still, the market tightness is also a function of a huge planned increase in copper smelting capacity, with new plants planned everywhere from China to Indonesia and India.

In theory, that shouldn’t necessarily be bullish for the price of copper. More smelters mean more metal, and the rise in capacity should have been enough to keep the market for copper metal well supplied over the next year or two. But most analysts and market-watchers expect some smelters to be forced to push back project launches, bring forward maintenance, or even curtail existing production.

The spot TC/RC rate “is clearly below the costs of almost all smelters in the world, which is why this situation is not sustainable,” said Ivan Mlynarz, chief executive officer of Chile’s state-owned Enami.

History suggests that the plunge in TC/RCs could be a prelude to a sharp rally in prices.

In past periods of copper concentrate tightness, the low point for TC/RCs was followed by cuts to metal production with a lag of two to three months, said Lang. Within eight months of the low point, refined copper stocks dropped by an average of 38%, he said. Within 11 months, the copper price increased by an average of 20%.

In fact, nadirs for TC/RCs in 2004 and 2010 were followed by some of the most dramatic copper bull markets ever.

“The extremely tight concentrate market indicates it will be hard to maintain refined metal production at sufficient levels to meet demand as the year progresses,” said Lilley. “In markets like this, that are primed to blow but feel a bit early, sometimes a trigger gets provided unexpectedly.”

(By Jack Farchy and James Attwood)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments