A European stock trader’s guide to an era of scorching inflation

Rampant inflation has been at the core of this year’s equities selloff and it’s not going away. Now comes the hard part: positioning for it.

In theory, steeply rising prices should favor cheaper, so-called value stocks such as banks, while denting growth shares. Interest-rate hikes to keep prices in check mean bigger profits for lenders, while hurting the likes of technology stocks by creating a larger discount for the present value of future profits.

Yet with a recession on the horizon, it’s not so simple. Firms whose products are most at risk of a cost squeeze such as retailers, leisure providers and homebuilders are viewed as being most susceptible to slowing economies, while those with better pricing power, like consumer staples and health care, are trading at big premiums to the broader market as investors flock toward safer havens.

“There’s an inflation recalibration going on and that comes with severe, important consequences from an equity market perspective,” said Wouter Sturkenboom, chief investment strategist for EMEA and APAC at Northern Trust. “Investors are looking at this world through a new lens and it’s more inflation-focused and more risk reduction-focused,” he said in an interview.

In the circumstances, any signs of an easing in prices are likely to be taken positively. “It’s the direction of inflation that matters for share prices,” said Liberum Capital Ltd. strategist Joachim Klement. “Every decline in inflation reduces some of the cost pressures companies face.”

Here’s a look at how Europe’s inflation crisis is playing out across sectors.

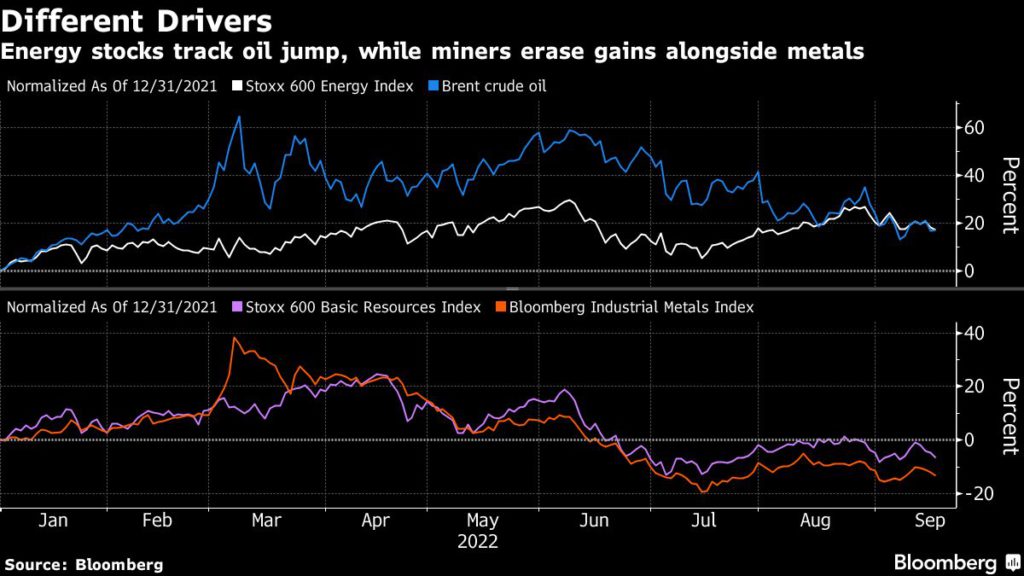

Commodities

Energy is the only European sector in the green this year, boosted by the surge in oil prices. And analysts aren’t ruling out further gains. Credit Suisse Group AG lifted price targets across the sector on Friday, citing top pick Shell Plc and TotalEnergies SE as stocks that may outperform further.

Renewable stocks, meanwhile, are seen as long-term winners as countries invest heavily to reduce reliance on fossil fuels and imports from Russia.

For mining stocks, the outlook is less certain. While they tend to outperform during periods of elevated inflation, gains may be curtailed by concern about China’s demand for metals due to the country’s housing downturn and the economic impact of its Covid-zero policy, according to Morgan Stanley analysts including Alain Gabriel.

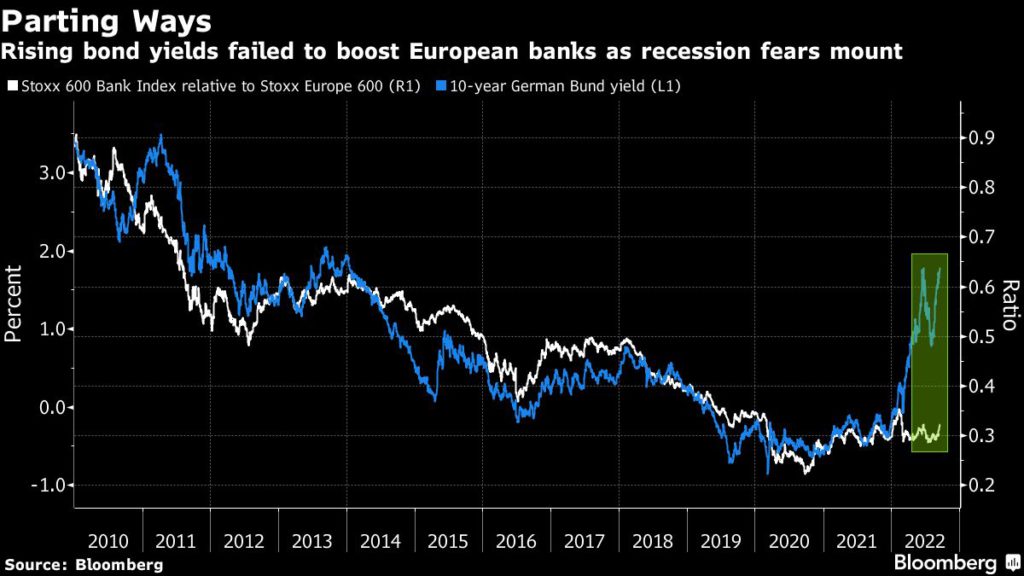

Banks

The sector, which falls into the value category, is emerging as an inflation winner, showing the best performance among industry groups in Europe this month. Higher interest rates to cool prices mean bigger profits on lending.

Bank of America Corp. analyst Alastair Ryan says the sector could see an 88 billion-euro ($88 billion) boost to net interest income boost from expected rate hikes. “This very large revenue increment is why we remain positive on the banks in the face of troubles elsewhere,” he wrote in a note.

On the flip side, lenders face worries over the volume of bad debts that could materialize during the impending recession, which may explain why rising bond yields haven’t provided a bigger boost than they have.

Staple goods

Pricing power is key during inflationary periods. Firms that are able to shield their margins as costs rise — like consumer staples, health care and grocers — are likely to be favored, says James Athey, investment director at Abrdn Plc.

Yet inflation also poses risks to European staples. According to Morgan Stanley analysts including Pinar Ergun, consumers in the region are more vulnerable to rising living costs than elsewhere in the world due to an unstable geopolitical backdrop and the energy crisis.

“Investors appreciate the defensiveness of the sector, but at current valuation levels, many opportunities have become prohibitive,” they said.

Retail

Retailers are the worst-performing industry group in Europe this year, and inflation has a lot to do with it. With budgets crimped by the cost of everything from food to energy to mortgages, consumers don’t have as much left for shopping, while rising costs are eating into profitability too.

It’s “a gloomy picture for retail stocks,” said Charles Hepworth, investment director at GAM Investments. “Disposable incomes of most consumers have been massively squeezed, and trade-down substitutions into cheaper brands are hardly the best fillip for any hope of a consumer-led recovery,” he wrote.

Luxury apparel may be among safer bets. Sophie Lund-Yates, an analyst at Hargreaves Lansdown Plc, favors firms such as LVMH, with customers of its Louis Vuitton brand “less likely to be hurt by the downturn in real wages.”

Technology

As a core part of the growth category, technology stocks have been at the forefront of this year’s global equity rout due to surging bond yields. And despite its underperformance, the sector “remains very expensive,” according to Barclays Plc strategist Emmanuel Cau.

“With burgeoning signs of lower demand coming from semiconductors, demand destruction may be the next shoe to drop,” Cau said.

Construction, real estate

Construction faces a precarious outlook. The industry is “anxiously waiting to see how the double headwinds of squeezed budgets and rising rates will impact demand,” says Danni Hewson, analyst at AJ Bell. Homebuilders like Barratt Developments Plc and Persimmon Plc have plunged more than 40% this year, while Hewson says suppliers to the sector could also be at risk. HeidelbergCement AG and Travis Perkins Plc are among stocks to watch.

Meanwhile, Goldman Sachs Group Inc. analyst Jonathan Kownator warned on Friday of escalating macroeconomic risks for commercial real estate, downgrading Land Securities Group Plc, British Land Co Plc and Aroundtown SA. The sector has a very high negative correlation with bond yields, he said.

(By Joe Easton, Sagarika Jaisinghani and Michael Msika)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments