Partner content: Can West Africa Meet its Growing Potential?

In the recently launched MACIG West Africa 2021-2022, Global Business Reports (GBR) investigates the West African region as it grows in range and relevance for the global mining industry. Here’s why:

Unbeatable gold exploration upside:

“West Africa has been the most prolific contributor to new gold in the last two decades,” said Mark Bristow, President and CEO of Barrick Gold, which operates the 650,000 oz/year Luolo-Guonkoto complex in Mali, as well as the Tongon mine in Ivory Coast.

(Read GBR’s full interview with Mark Bristow here)

The West African region is already the second-largest gold producer after China and, although it absorbs less than 10% of global exploration budgets, it has massively over-delivered with 80 million oz of gold reserves discovered in the last ten years – more than anywhere else in the world.

Hyper-active M&A with more and bigger companies in the region: The last two years came with some head-turning transactions: West Africa created its first supermajor when Endeavour acquired another West African producer, Teranga Gold.

Also, Fortuna Silver stepped into West Africa through the acquisition of Roxgold, a first for a Latin American-focused producer.

“West Africa has been the most prolific contributor to new gold in the last two decades”

Mark Bristow, CEO, Barrick Gold

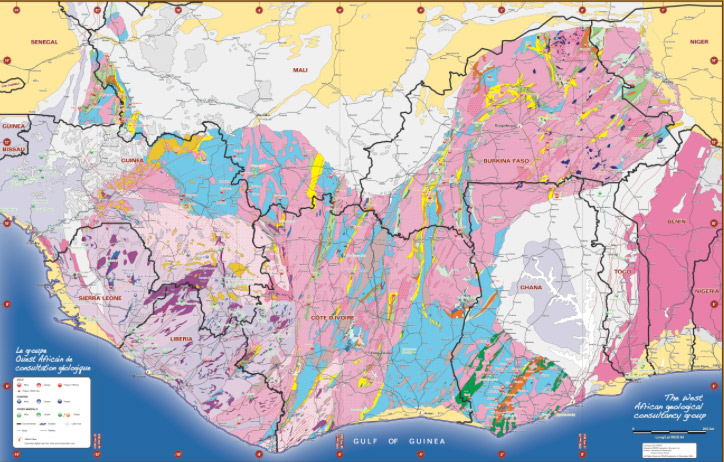

In a gold-depleting world, the underexplored Birimian Greenstone Belt, the geological structure stretching across the region, is a focal territory for new discoveries. West Africa has built a reputation for developing greenfield projects into profitable mines on time and under budget.

During the last two years, several gold mines including Wahgnion, Sanbrado and Yaouré have started production. Next in line to pour first gold in 2022-2023 are Tietto Minerals’ Abujar mine and Fortuna Silver Mines’ Séguéla mine, both in Ivory Coast, as well as Orezone’s Bomboré in Burkina Faso, and Cardinal Resources’ Namdini in Ghana.

Read more on GBR’s MACIG West Africa Report: “The Gold Producers”

More cash opportunities in the gold space: Gold Fields posted a 2020 net cash flow of $252 million from its two Ghanaian mines, a significant growth from $174 million in 2019, while Perseus Mining reported a net profit 48% higher in FY2021 compared to the previous year.

Whereas producers can directly leverage a higher gold price, juniors have improving investment sentiment to leverage. This has, however, been volatile in the last year, with the junior segment feeling gradually more “unloved” by the market, especially in the second half of 2021, but sentiment stays moderately bullish. The TSX and TSXV report the strongest IPO market in the last 15 years and the best half-year in the exchanges’ history for equity financing. The 100 African issuers in 34 jurisdictions, of which most are based in Burkina Faso and Mali, raised over $1 billion in the first nine months of 2021, a considerable upgrade from the $760 million raised the year before.

Read more on GBR’s MACIG West Africa Report: “The Gold Explorers”

More countries and more minerals: The centuries’ long history of gold production in Ghana, coupled with the impressive discoveries-turned-successful mines in Burkina Faso and Mali in the last decade, have helped to put other countries in the region on the gold map, explorers drawing geological parallels along the Birimian belt and beyond – adding Cameroon, Senegal, Equatorial Guinea and Nigeria into the mix.

But West Africa has more than gold. Guinea and Ghana’s bauxite, Mali and Ghana’s lithium or Niger and Mauritania’s uranium are watched with fresh eyes in a post-2020 scenario, where demand for each of these minerals is projected upwards. The financial endorsement that lithium projects have received from both private investors and equity markets, including ASX-listed Firefinch receiving $130 million to bring Goulamina lithium project in Mali into production, or IronRidge Resources’ fully-funded Ewoyaa project on track to become Ghana’s first lithium mine, set a positive precedent for non-precious metals in the area that has been mostly searched for gold.

Read more on GBR’s MACIG West Africa Report: “West African Metals in the Energy Transition.”

So what does it take for West Africa to rise to its potential and what is hindering its growth?

In the full report, GBR addresses recent regulation trends and what newly enforced local content policies mean for operators, international companies and local players; The nature and impact of the recent violence and political instability; The practicability of alternative energy sources; And the availability, adequacy and competitiveness of local services and equipment companies.

The MACIG West Africa Report also includes exclusive interviews with Mark Bristow, Sébastien de Montessus, Stuart Gale, and many others, together with interviews with the Ministries of Mines in Burkina Faso, Niger and Nigeria for recent policy updates.

About Global Business Reports (GBR)

Global Business Reports is an international publishing house with 20 years of experience producing in-depth industry reports. Sectors covered include mining and metals, chemicals, energy, oil and gas and life sciences. For more information, visit gbreports.com

The preceding Joint-Venture Article is PROMOTED CONTENT sponsored by Global Business Reports and produced in cooperation with MINING.com. Visit Global Business Reports for more information.

Comments