Zinc, it never rains but it pours

The Great Zinc Drought might be said to be broken, but those calling the end of this protracted dry spell going back to 2006 have been proven foolish before. However, this time around the degradation of the zinc mining space through mine closures, lack of a pipeline of new projects (or even old mines to reopen) and virtually zero exploration since 2011 means that the landscape is not only parched it is veritably scorched earth.

Zinc fell from about $0.90 per lb in the late ’80s to $0.40 per lb in 1993, then spent the rest of the decade constricted to a range between $0.40 and $0.55.

After the Tech Crash in 2000, it sunk below $0.40 per lb until 2003 when it began to regain traction. In 2004-5 it broke out above what appeared to be a multi-year $0.50/lb resistance and within two years quadrupled. In late 2006 it broke above $2 per lb.

If one enquires of a gold bull as to what the top performing metal of 2016 might be, they will immediately claim their own as the winner when in reality the best performing major metal is in fact Zinc. It was only a couple of weeks ago crossing the US$1 per lb threshold and it is now a long way from the US$0.67 at which it bottomed in the second half of last year.

As the preceding chart shows, Zinc has found resistance in previous years around the $1.10 per lb level and has then retreated. However, the supply situation has never been as bad in the last ten years as it is now.

It seems but a distant memory, but last October the obituaries were being written for Glencore, the world’s largest Zinc trader with over 60% of global traded volumes. Now those fears are well in the past and Glencore, like Zinc, has arisen from its grave.

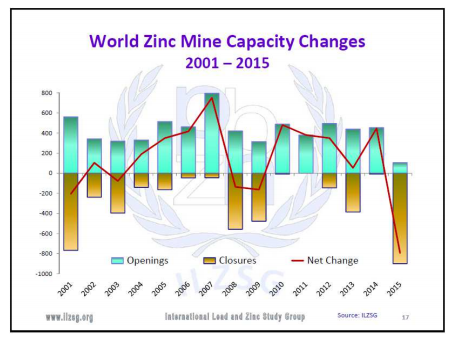

A key component of this turnaround has been scheduled mine closures (shown below) combined with temporary mine closures (by the likes of Glencore) to get the market back in balance.

Then if things couldn’t get worse in 2016 we are seeing:

- Glencore has reduced zinc mine output by 500k tpa in Australia, Kazakhstan and Peru

- Reduced output at HZL’s Rampura Agucha operation in India due to technical difficulties

- CBH Resources and Perilya to reduce production at Endeavour and Broken Hill mines in Australia

- Suspension of output at Al Masane in Saudi Arabia

In its recent results announcement, Glencore reported mining 506,500 tonnes of the metal in 1H16, a reduction of 223,800 tonnes from the same period of last year. Most observers think the company is not in a rush to reopen capacity until prices are even more rewarding. It should be remembered that Glencore as the largest trader and one of the largest miners in Zinc is in a “head you win, tails you win” situation with rising prices even if it keeps capacity closed until prices are, say $1.15 or $1.20. Even then it can eke capacity back into operation to not upset the balance of supply/demand and weaken prices.

Below we can see mine capacity changes this century. The year to contrast with is 2008, a bad year for every metal where the opening/closing ratio was not even vaguely as unbalanced as now with an even greater accentuation of the closures in 2015.

Heavy underinvestment has taken its toll on the pipeline of new projects, to the effect that there aren’t any to speak of. Therefore the International Lead and Zinc Study Group have projected shrinkage in supply for 2016, just as prices have started to surge. Here is their projection.

It may not be a large decline but 2016 is the second negative year in a row and reflects declining production from existing mines, exacerbated by mothballing or production cuts as a response to weak prices. The latter two actions can be reversed given time, but exhausted mines are removed permanently from the equation.

The industrial end-users of Zinc are now facing the long awaited perfect storm in zinc, where a modicum of demand growth encounters a chasm in the production pipeline. However, we should rephrase that as there is NO production pipeline to speak of. This is the major metal where least money has been spent since 2006 in new discoveries or development than any other metal.

Zinc is of course linked inextricably with the fortunes of Lead, where prices have lagged and production has also been impacted by closures of mines (and repurposing of refineries, such as Nyrstar’s actions at Port Pirie).

This trend is feeding through to LME warehouse levels as the chart that follows shows. Statistics (always rubbery out of China) suggest that Shanghai stocks are not what they were either with a considerable shrinkage.

Added to this is the estimate for the trade study group of a 3.5% rise in demand in 2016 and we can see a supply crunch that is motoring the price along nicely. With such a tailwind, and end-users scrambling to write contracts to guarantee supply, the price has recently breached the $1 per lb level, where it has consolidated, and looks almost ready to challenge the previously impenetrable $1.10 barrier.

What will happen is that no major in the mining industry shall consider new investments until prices breach $1.20 and even then they would rightly (on previous bad experience) want to see them hold there before getting over-excited about launching projects. This means an ever-worsening supply situation. For existing producers this will be a deeply profitable and long overdue development. The mood will fire up the hunt for juniors that have respectable projects by investors and by potential predators.

Rain image is a Creative Commons image by Jane

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments