Why Mexico’s oil reform is a huge opportunity for investors

When a massive country de-nationalizes its entire energy sector and opens its oil and gas doors for the first time ever to foreign companies, the opportunities are staggering.

Welcome to the ‘new’ Mexico, and welcome to the early stages of an oil and gas game that will be bigger—from an investor’s perspective—than anything in history.

Mexico’s move to implement historic energy reform legislation in December 2013, and follow-up legislation in 2014 that further solidified the comprehensive de-nationalization, provides an unprecedented opportunity for oil companies looking to tap into Mexico’s huge energy potential.

Mexico has ended the now 75-year monopoly of state-owned Petroleos Mexicanos (Pemex), and admitted in no uncertain terms that it needs foreign partners and investors. All of this has prompted the US Energy Information Administration (EIA) to revise its 2040 forecast for Mexican oil and gas production upwards by a whopping 76 percent.

All of this, says International Frontier Resources Corp. CEO Steve Hanson, means that “over the next four years, we will see accelerated growth for a country with massive oil and gas resources, excellent infrastructure, a transparent investment framework, and a new hunger for foreign partners. In short, it is the largest energy opportunity in the world today–and the door has just been opened.”

From the supermajors to the small-caps, the interest is expansive and the competition is only set to intensify. With this in mind, we’re looking at three companies that are taking optimal advantage of Mexico’s wide-open playing field both offshore and onshore. These companies know how to play it and why being a first-mover on this scene is so important:

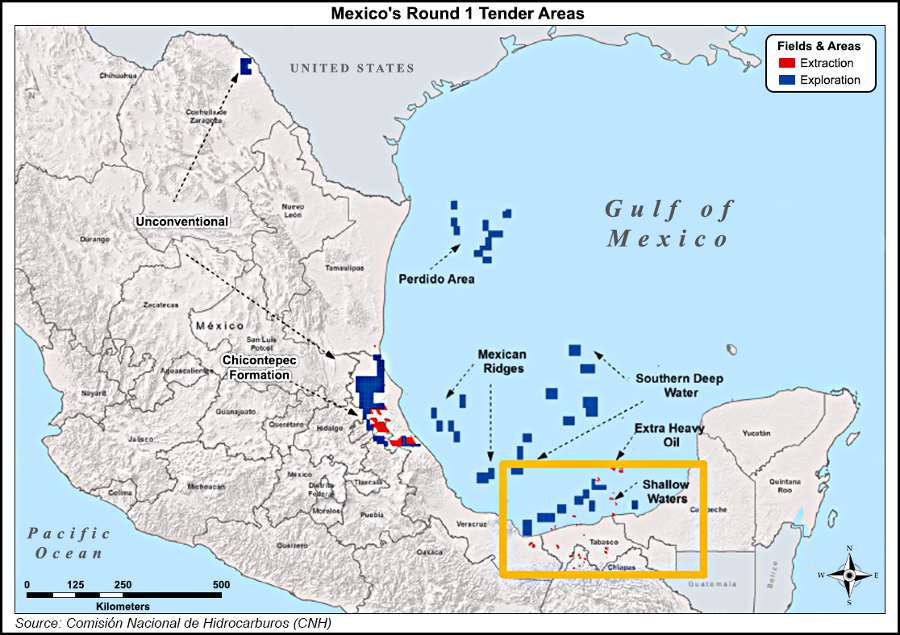

Exxon Mobil: The Supermajor Run on Mexico’s Offshore Bounty

For Exxon, 5 December is crunch time for getting into Mexico. In August, Exxon Mobil Corp. (NYSE:XOM) joined Chevron Corp. (NYSE: CVX) and Hess Corp. (NYSE:HES) to jointly bid for rights to drill in Mexico’s deep waters in an auction set to take place on the fifth of December. So far, the three have a joint operating agreement, the details of which remain a mystery. A total of 21 companies have registered for this auction–including major international players Shell (NYSE:RDS.A), Italian ENI (NYSE:E), and BP (NYSE:BP)–which will put up 10 offshore areas.

These offshore blocks are said to be Mexico’s most lucrative, keeping in mind that some 76 percent of the country’s potential oil resources are in the deep-waters. The reserves in these 10 blocks are said to be worth an estimated US$10 billion.

But where it gets really interesting is that this massive interest in Mexico’s offshore potential was already signed on before Pemex announced a string of new offshore discoveries in September. A total of six new oil deposits in the Gulf of Mexico—two in deep water and four in shallow—up the ante on the auction even further. The combined reserves of the two deep-water discoveries alone are estimated at 140-160 million barrels of oil equivalent (proven, probable and possible, or 3P, reserves).

Then we have the Trion discovery in the northern Gulf of Mexico, also up for auction on 5 December. The bidding rules have recently been changed for Trio, paving the way for a single operator to work alongside Pemex for 60 percent of this massive project. Trion is estimated to have 3P reserves of 480 million barrels of oil equivalent, and it covers 1,250 square kilometers just south of the US-Mexico maritime border.

This is one of the most intense exploration areas in the world right now, and the Mexican government is hoping to bring in around US$7 billion in investment from this auction, not including Trion.

But this is for the investor who is looking to play Mexican oil at the highest level, and for the long term. Exploration of these areas up for grabs can take around eight years and another two years to take it to production. Deep-water exploration is expensive—even if Mexico is one of the cheapest venues to operate in—so this is a long-term game that could ride out today’s depressed oil prices.

Pan American: First Foreigners to Start Drilling Offshore

The first non-Pemex operator to get to drilling offshore Mexico since the reforms were implemented was Argentine Pan American Energy, whose owners include British giant BP Plc (NYSE:BP), China’s CNOOC, and Argentine conglomerate Bridas.

Pan American beat out five other offers for the Hokchi shallow water block last year, and on 30 October began drilling operations, targeting a depth of 2,867 meters below the drilling rig floor. The block is some 27 kilometers off the port of Dos Bocas in the state of Tabasco. Initially, Pan American and its Argentine partner will invest over US$212 million in a four-well plan over two years.

What’s next in Mexico’s shallow waters? Next year, will see Pemex farm-outs in the Ayin-Batsil (shallow waters) and Ogarrio and Cardenas-Mora, both high-potential onshore areas.

Stay tuned as Pan American drills deeper.

International Frontier Resources (V.IFR): First Move Onshore

One of the ‘first movers’ in Mexico’s onshore bonanza was International Frontier Resources, which secured the Tecolutla Block in Mexico’s first onshore licensing round. And this is where the idyllic partnerships come into play: The joint venture behind this onshore play is Tonalli Energia, a 50/50 deal which brings together Canadian oil and gas company IFR and Mexico’s Grupo Idesa, a leader in the Mexican petrochemical industry.

The JV won the Tecolutla block, otherwise known as “Block 24”, and signed a historic license contract with the Mexican government on 25 August.

It’s not just the block that’s important, it’s the fact that it places the JV among the first on the scene: This gives this small-cap a very large-cap strategic operating presence in the Tampico-Misantla Basin and a solid foothold into Mexico’s lucratively liberated oil and gas sector.

The ‘new’ Mexico is a great venue for an ambitious junior. What makes it even more attractive is the fact that production in Mexico is among the cheapest in the world. So even if we are looking at today’s depressed oil prices, Mexico still makes economic sense; there is still a profit to be turned here, while at the same time setting up investors for a long-term financial bonanza when prices rebound.

Development costs in Mexico’s oil patch, according to Deloitte, come in at an average of $23 per barrel. But it gets even better than that: Roughly 60 percent of the country’s production comes from areas that cost around $10-$21/per barrel to develop.

While Mexico’s deep-water offerings are mouth-watering, and a foreign company has already started drilling in the shallow waters, the massive onshore conventional fields are cheaper and easier to develop, making for an attractive, easy way to get a foothold in this ‘new’ venue.

Mexico has multiple large conventional onshore oil fields with significant upside once we start talking about modern technology brought in by foreign partners, and the ability to take exploration farther into tighter reservoirs to increase recoverable reserves.

Mexico was producing around 2.8 MMOBPD in 2014—87% of it crude oil. By the end of that same year, Mexico had 9.8 billion barrels of proved oil reserves. Of that 2014 production, 25% came from onshore fields.

On the Tecolutla block, Tonalli is planning to work-over existing wells to get production on stream while preparing to drill their first well. And to this end, the company is bringing new technology to take peak production to new levels. While Tecolutla is oil-weighted, Tonalli is open to pursuing both oil and gas opportunities, and this first block is just the beginning of a plan to make an aggressive move on Mexico’s next onshore offerings.

Natural gas isn’t off the table, particularly because Mexico is a net importer and IFR’s JV partner, Grupo Idesa, is itself a huge user of natural gas.

In August, Mexico launched the tender of 12 new onshore exploration and production contracts as part of its second phase auction. Nine of these contracts are in the Burgos basin and three are in the Sureste basin. Winners will be announced on April 7th, 2017. Look out for this company in round two of Mexico’s onshore auction.

Next year, we should see at least seven additional onshore opportunities, with another 64 blocks up for grabs in 2018—not to mention 86 natural gas contracts. All told, we’re looking at 59,600 km2 acres of conventional and unconventional exploration in more than 200 onshore blocks and 150 Pemex farm-out blocks.

It’s all about partnerships—and from an investor’s perspective, this is where it really matters. Mexico’s strategy is intended to “dramatically expand” the use of partnerships in exploration and production over the next five years—opening up an amazing number of opportunities. In the next two years alone, we’re looking at 160 very specific opportunities for foreign companies.

Schlumberger CEO Paal Kibsgaard recently told investors that a “momentum shift” is coming in Mexico, and drilling should begin to pick up speed next year.

Right now, there is nothing bigger than Mexico when it comes to oil and gas sales. We’re talking about North America, large oil reserves, good infrastructure, and discoveries that are already in development. As such, the waiting list is going to be a long one, so the first movers are key.

With undeniably high-quality crude coming in at prices below today’s Brent or WTI, this is a gold mine for foreign oil and gas companies, and a gold mine for investors who figure out the game.

By James Stafford of Oilprice.com

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments