Why gold is priced rationally – and how it obtains a real return

It doesn’t pay interest, its highly volatile, and even Fed Chairmen publicly state they don’t know how its priced – gold remains a mystery. Perhaps not.

Gold is generally thought of as a non-income-earning asset held as a hedge when market or political risk perceptions rise. Its role in portfolios has never been clearly defined. In fact, I show in my new peer-reviewed Journal of Investing paper that the price of gold is fully rational, based on fundamental principles, obtains a real return, and is clearly linked to the valuation (P/E) of stock markets (earlier Journal of Investing article).

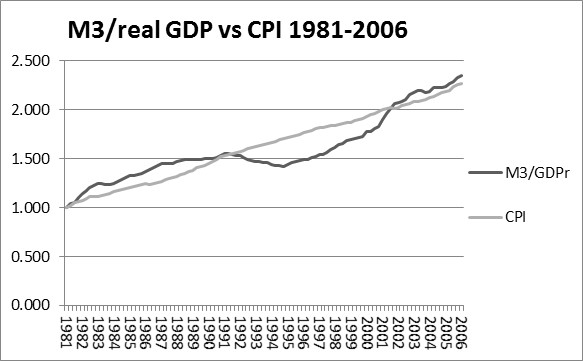

Fiat money itself is not thought of as an investment asset for the simple reason that it loses purchasing power at the rate of inflation. Fiat money-based investment assets pay a return in fiat money – stocks and bonds for example – and must return, in fiat money, more than inflation after taxes to provide a real return in the form of capital gains, dividends and interest. Figure 1 shows the indexed ratio of M3/real GDP against the index of the CPI.

Figure 1: M3/Real GDP vs. CPI 1981 – 2006

A simple regression of this relationship has an R-squared of .83. The striking relationship offers empirical support for the premise that the excess of broad money supply growth in relation to real GDP growth is the source of inflation – loss of purchasing power of goods and services per unit of fiat money.

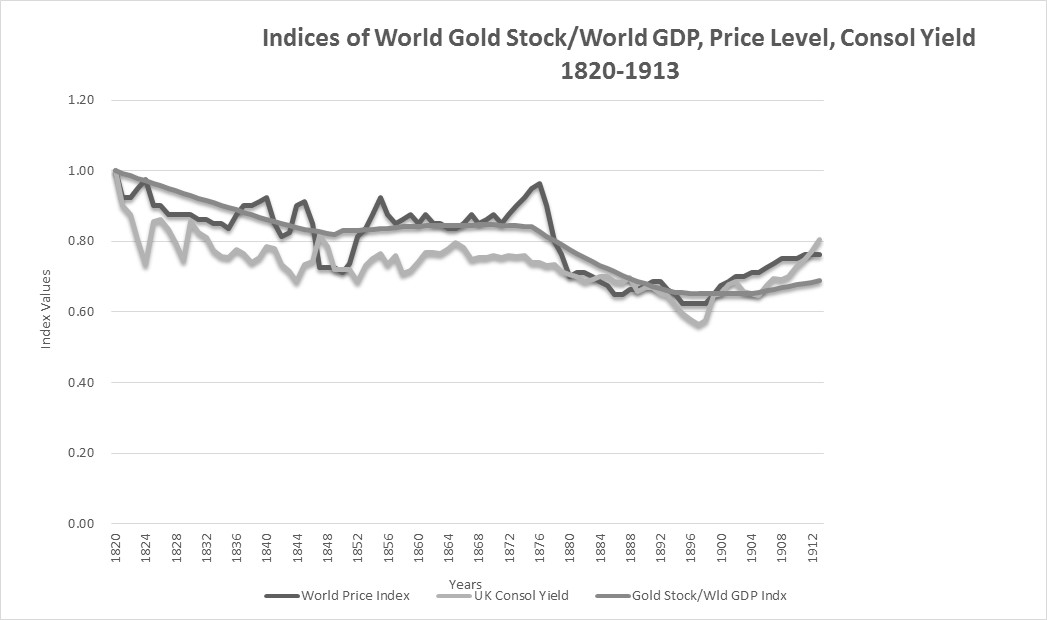

The author has constructed a similar measure for gold, as a global asset, over a time period with reasonably good data for the total above ground world gold stock, world real GDP, and the world price level – the critical ingredients for an empirical test in Fig. 2.

Figure 2: Pure Gold Standard World CPI vs. World Gold Stock/World Real GDP 1820- 1912

Over the 93-year period, the world price index (available from Barsky-Summers (1988)) clearly moves with the ratio of above ground gold stock to world real GDP (regression R-squared of .73). The divergences in the mid 1840’s and mid 1870’s correspond respectively to the U.S. banking crisis and depression and the UK Great Depression. Both historic and more recent gold mine production data (World Gold Council) show a clear and consistent pattern of above ground gold stock growth of about 1.2%; which closely matches world population growth. This of course means that world real GDP grows faster than world gold stock at the rate of real per capita productivity growth (GDP growth comprising inflation, population growth and per capita productivity growth).

This indicates that gold, in the roles of a medium of exchange and investment should therefore gain in real purchasing power (in terms of a basket of goods and services) per unit at the rate of world real per capita productivity growth; in contrast to fiat money which loses purchasing power at the rate of inflation. Roy Jastram (1977) however, finds that gold appears to play the role of a constant rather than accretive store of value.

Jastram studies the price and purchasing power of gold in terms of British and US currencies. He also does not consider the relevant ratio of world gold stock to world real GDP. Erb and Harvey (2013, 2015) also evaluate the price of gold in dollars; not in terms of global purchasing power.

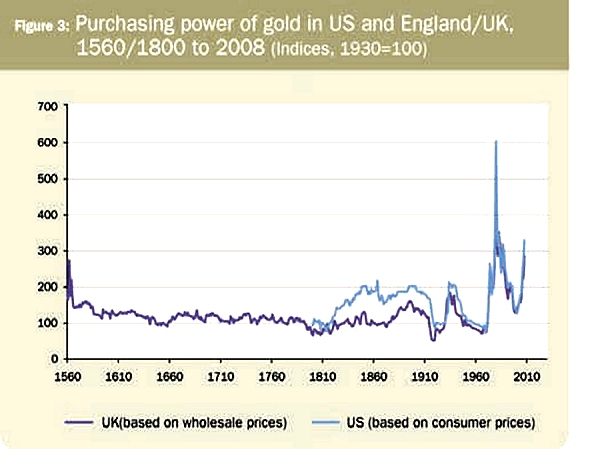

Several exhibits follow which illustrate the actual historical path of gold’s global purchasing power. Figure 3 shows a seemingly constant gold price in terms of U.S. and British currency over long periods of time. Fig. 4 however, shows the large gains in share of world GDP made by the U.S. and the UK over the same period.

Figure 3: Jill Leyland in the LBMA’s Alchemist Issue 56

Figure 4: Ian Bremmer of Eurasia Group

Actually, the currencies of the both the U.S. and UK greatly appreciated against those of the rest of the world. The price of gold remained relatively constant when measured in these currencies, but in fact gained in purchasing power in terms of global goods in services, as expected. Thus, as a store of global purchasing power per unit, gold obtained a real return using the only measure of “real” that counts: purchasing power of global goods and services.

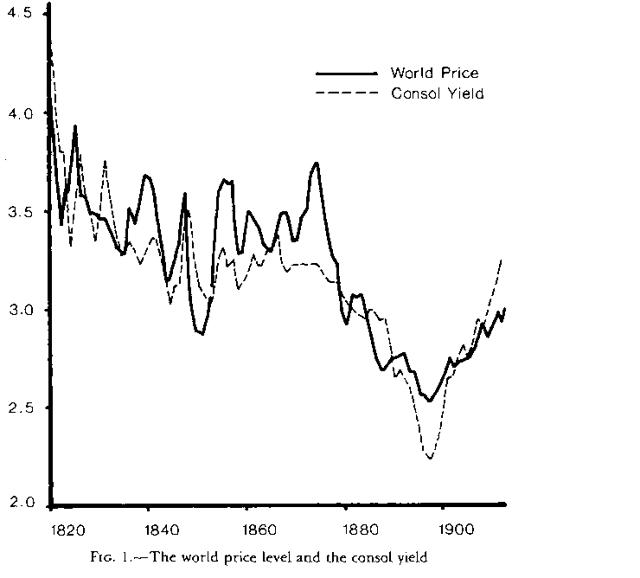

The Gold Standard period provides a hint regarding how gold is actually priced globally. In Fig. 5 Barky-Summers show the UK consol yield in relation to the world price level. This relationship is known as “Gibson’s Paradox”.

Figure 5: Barsky-Summers (1988)

Standard Finance theory states that the rate of interest should vary directly with the expected rate of inflation – not the level of prices. However, during 1820 to about 1910, the British government’s consol bond – a perpetuity paying fixed interest-only and convertible into a fixed amount of gold during an era when currency was fully convertible to gold at a fixed rate, paid a yield that varied directly with the national general price level (and even more so with the global price level).

The observation is a paradox for example, because a constant expected general price level implies zero inflation and thus should cause a fall in interest rates from a prior period of positive inflation expectations. Under the gold standard, a constant price level did not influence the yield of the consol. The consol yield varies with the price level; thus a doubling of the CPI doubles the yield and so on. A flat CPI – zero inflation – surprisingly, leaves the consol yield unchanged.

A number of eminent scholars have addressed Gibson’s Paradox including Irving Fisher, Thomas Sargent, Robert Shiller and Jeremy Siegel. Among the most notable is the work of Robert Barsky and Lawrence Summers in their “Gibson’s Paradox and the Gold Standard” paper (1988). They posit that gold prices varied inversely with changes in real interest rates – which effect, however, they cannot consistently find under fiat monetary systems as they state in their paper. Under their theory, real rates first change, then impact the price of gold, which then translates to a change in the price level in terms of gold.

Barsky-Summers view the nominal rate as essentially the real rate because of the lack of serial correlation of inflation and because nominal rates showed no predictive power for future inflation; thus they assume no inflation premium was embedded in nominal rates; making them essentially real. Therefore, they assume that a rising consol yield was evidence of a rising real required interest rate which in turn caused gold, which they viewed as a durable good, to fall in price because of the rising return available from alternative assets.

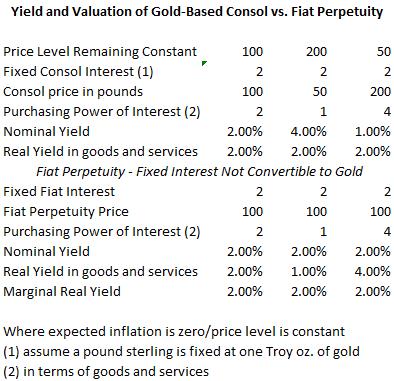

However, Fig. 2 shows that the world price level was in fact a direct function of gold stock and world GDP – totally independent of any real interest rate causality. A close look at the yield in terms of purchasing power evidences a constant real yield in terms of purchasing power of the interest payment in relation to the nominal consol price (Fig. 6).

Figure 6: Consol Yield and Fiat Perpetuity Yield Under Varying Price Levels and Zero Expected Inflation

Note that if a 2% consol yield at time 0 bought 2 units of goods and services (a 2% real yield in terms of goods and services) and the price level doubled, the nominal yield doubled and the purchasing power of the fixed interest fell in half, as did the consol price; which left the real yield a constant 2% (1 unit of goods and services purchasing power over half the price as before). If in fact gold is required to obtain a real inherent yield equal to its long term average of about 2% which is the long term rate of real per capita, and thus per Troy oz., productivity growth rate outlined in section 1, then a constant new doubled price level results in a doubled nominal yield in order to maintain the required constant 2% real yield. The logic holds for any combination of price level and associated consol yield where the price level is a function of gold and real GDP.

In order for gold to have a real yield, the world price level in terms of gold must be falling at the rate of per capita productivity growth. Thus a constant price level means gold is failing to earn its required return and so the yield of the consol cannot fall. This is because gold must inherently obtain a real yield; in contrast to fiat investment instruments which obtain a fiat interest or dividend payment or a growing share of equity earnings in relation to which price is set. A fiat perpetual bond, if it is to offset purchasing power erosion of the principal due to inflation, and earn a real after-tax return of say 2%; must yield (2% + i)/(1-t) where (i) is the expected inflation rate and (t) is the effective tax rate.

During the Gold Standard, the valuation of gold was clearly based on the requirement that gold earn a constant real yield in relation to a basket of goods and services. Building upon this, a very effective theoretical and empirical gold valuation model in terms of fiat currency can be built. Gold may be valued according to at least five functions:

- Gold’s cumulative real value results from its cumulative above ground stock relationship to world real GDP;

- It’s cumulative additional nominal value derives from world fiat inflation;

- A change in fiat inflation expectation should result in a directionally consistent change in gold price in fiat currency since gold’s real yield is unaffected by fiat inflation;

- A change in medium to long term market required real yield in relation to 2% (the long term real per capita productivity growth rate and long term real gold yield) should cause an inverse change in gold price;

- The local or national gold price should also be an inverse function of changes in the global real purchasing power of the local currency

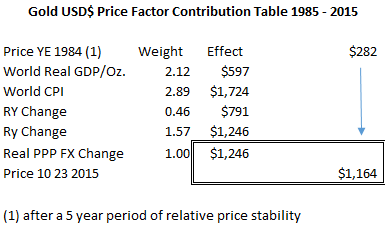

This resulting model is shown in the author’s current Jrnl. Of Investing paper and cannot be reproduced here for copyright reasons. The model results in the following factor contribution table of the change in the U.S.$ gold price from 1985-2015:

Figure 7: Gold USD price factor contribution 1985 – 10/2015

Where the global real yield of gold has more than doubled gold’s real price (2.12 factor) and the decline in world long term real interest rate (Ry) has added another 1.57x to the real price; while much lower global expected inflation rate (RY) has reduced its price in fiat terms by .46. These factors demonstrate why simple correlations of the price of gold to exchange rates, GDP, inflation and other macro variables are wholly inadequate to describe it valuation.

Fig. 8 shows the valuation model’s predicted vs. actual gold price, point to point, using only then-current economic expectations.

Figure 8: Gold Price Compared to Enhanced Required Yield Model

This model exhibits an average absolute variance from 1978 – 2015 of 12.02% with R-squared of .967; and 8.3% absolute variance from 2005 to 2015.

Predicting the price of gold is relatively simple for world real GDP, gold stock growth and inflation-related price gains; but much more involved for changes in the world expected inflation rate, local real exchange rate and the long term real interest rate. These last three factors account for the volatility of real gold prices. Understanding the valuation determinants of gold enable its proper context in portfolio allocation decisions as investors assess their views of the direction and magnitude of change of valuation determinants as they impact various asset classes. The author’s earlier paper shows precisely how the valuation of gold and the change in the P/E ratio of stock markets are linked and driven by the same principles.

INTELLECTUAL PROPERY NOTICE: computer applications of the disclosed gold valuation method in the United States of America or by United States of America domiciled persons or entities may not be deployed without an executed non-exclusive patent license agreement with the author and US patent 8095444 owner.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments