Which Junior Gold company will be the next takeover target?

In light of Goldcorp’s strong pursuit of Osisko over the last month, we had put together an extensive research on the resources of major and mid-tier gold miners. With that article, we uncovered some interesting information on the supply side as well as posited guesses as to who may be the next to make strategic acquisitions.

Building on this, our analyst team at Tickerscores decided to take a look at our database to see which gold companies we thought would make the most attractive takeover targets.

Are Companies Priced to Buy?

It’s hard to know how cheap a company is trading at without putting it in some form of context. For example, how did the attempted Osisko buyout compare to other recent transactions? Also, how does the offer for Osisko compare to the valuations of other companies out there?

First, let’s look at an expensive transaction that took place at the “top” of the market. In August 2010, Kinross bought Red Back Mining for $7.1 billion (a 17% premium). Red Back owned the Tasiast and Chirano mines. This ended up being a $3 billion writedown for Kinross so, as you can imagine, the project economics aren’t the most robust: the project had a $1.1 billion NPV with an 11% IRR at $1,500 gold. Kinross ended up paying approximately $390/oz, which is at the expensive end of the spectrum of M&A activity.

A more reasonable buyout is New Gold’s recent acquisition of Rainy River Resources in 2013. New Gold paid $310 million and the Rainy River project has an NPV of $438 million with only a 13% IRR at $1,300 gold. That means New Gold only paid around $50/oz of gold, but it should be noted that the mine still has to be developed so that partly explains the cheap price.

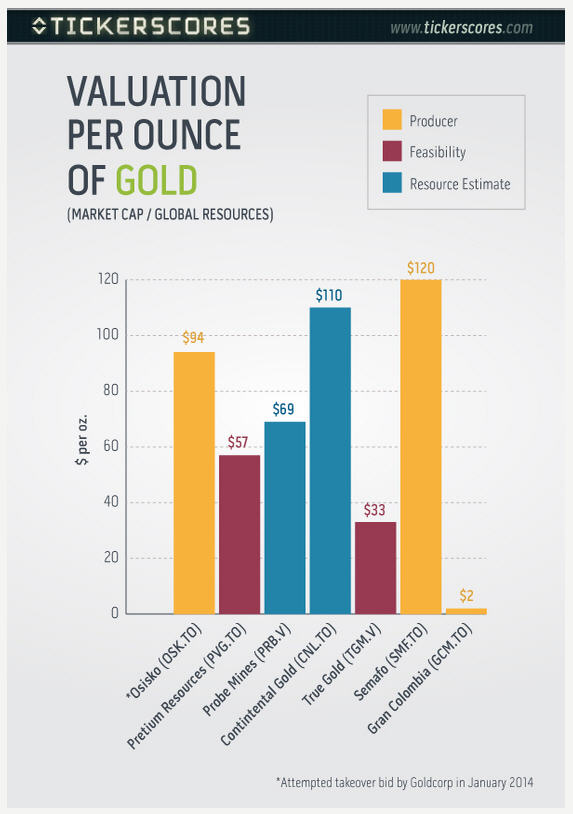

Lastly, if we look at Goldcorp’s initial offer for Osisko, we get a price of $94/oz. If the transaction were completed at that price, Goldcorp would get the Malartic Mine that currently produces roughly 120,000 ounces per quarter (~480,000 / yr) as well as two development stage projects (Hammond Reef and Upper Beaver).

What Else is Out There?

The majors have all learned an important lesson: a company that makes money at $1,200 gold will still make money at $1,900 gold, but a company that can only make money at $1,900 gold will be in trouble at lower levels. Companies cannot directly control the price of gold, but they can control their costs by being efficient and taking on quality projects with size and grade.

Here are some companies with high-grade, multi-million ounce deposits that could be potential takeover targets. In the graph below, they are compared by $/ounce of gold, but keep in mind this is just one way to compare these companies. As an example, a company could have many ounces of gold, but that gold could be uneconomic to extract. That is why we will look at the project economics and jurisdictions as well.

Takeover Targets Close to Home

Here are some companies with projects in North America that could be good targets. In the bottom of a market, majors will likely look at these types of projects first as they are generally in the safest jurisdictions.

Pretium (British Columbia, Canada)

Pretium arguably has one of the best deposits in the world. Pretium is in the feasibility stage, and has 13 million oz @ 13.5 g/t. The project’s NPV is $2.6 billion with a 42% IRR and a payback period of 2 years. They have a current market cap of approximately $745 million. This means they are trading around $57/oz.

Probe Mines (Ontario, Canada)

Probe is in the development stage with an initial resource estimate of 4 million ounces averaging 1 g/t. Probe has recently discovered a high-grade system that is not included in this resource estimate that likely makes it a highly sought after takeover target. The high-grade system allows the producer to target these ounces first, bringing the mine to profitability sooner.

Probe has a market cap of $277 million which gives a value of $69/oz. If Probe adds even 25% or 1 million ounces to the deposit, it could make it an even more attractive target. This is likely, since the last resource estimate was in January 2013 and does not include any of the new drilling at the high-grade system. Probe is expected to have a PEA come out this quarter.

Also of note: Agnico-Eagle currently owns 7.5m shares which is roughly equal to 10% – this makes them a potential suitor.

Stepping Out of the Comfort Zone

Here are some great projects, but they are in less ideal jurisdictions.

Continental Gold (Colombia, South America)

Continental has 5.4 million ounces that average nearly 10 g/t. Continental is trading at $110/oz. The only hurdle is that Continental is located in Colombia.

True Gold (Burkina Faso, Africa)

True Gold has 3.3 million ounces that average 1.04 g/t. It is a heap-leach operation in West Africa that on average will produce 97,000 ounces per year for 8.5 years. The project economics are robust, at $1,250 gold the project NPV is $178 million after-tax with a 43% IRR and a 1.4 year payback period.

Some Producers Worth a Look

Here are some producers that are already permitted and producing, which reduces the takeover risk.

Semafo (Burkino Faso, Africa)

Semafo operates out of Africa in Burkina Faso. They have 9.6 million in global ounces, currently produce 38,000 ounces per quarter and their all-in costs are approximately $1,270 / oz. They currently have a market cap of $1.1 billion, which translates to approximately $120/oz.

Gran Colombia Gold (Colombia, South America)

Gran Colombia is on track to produce 80,000+ ounces this year. They have approximately 1.9 million very high grade ounces (12 g/t) at Segovia and 14 million lower grade ounces (~.93g/t) at Marmato. At a current market cap of $34 million, they are trading at only $2/oz.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

{kind=link}

Comments