Russell: Were China’s August commodity imports strong? Depends on your time frame

(The views and opinions expressed herein are the views and opinions of the author, Clyde Russell, a columnist for Reuters.)

China’s imports of major commodities appeared to show signs of strength in August, but the gains in volumes are more nuanced and illustrate the difference between a short-term view and longer-term fundamentals.

Imports of crude oil, natural gas and iron ore all recorded strong gains in August from July, while coal was down from the previous month but up a massive 35.8% from the same month in 2020, according to official customs data released on Sept. 7.

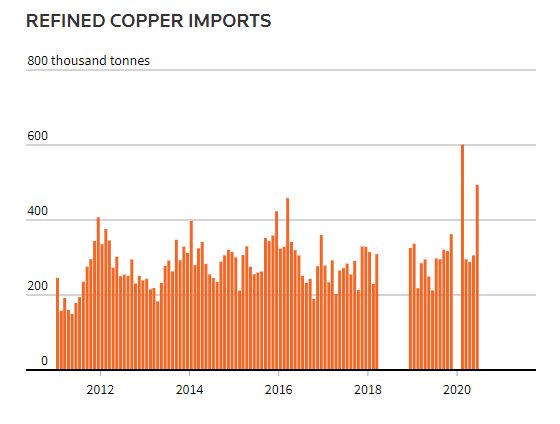

The outlier was unwrought copper, with imports falling to the lowest in two years, dropping 41.1% from the same month in 2020 and 7.1% from July.

China is the world’s biggest importer of crude oil, coal, iron ore, copper and also of natural gas, if pipeline and liquefied natural gas (LNG) are combined.

The August trade data for major commodities is an example of how it’s possible to maintain different views on the outlook for a commodity, depending on the time frame selected.

It is possible to be bearish short term and bullish long term, or vice versa, and this doesn’t necessarily imply holding contradictory viewpoints.

Copper is a good example of this. China’s unwrought copper imports were 394,017 tonnes in August, the fifth straight monthly decline and the weakest since June 2019.

Those figures seem unambiguously weak, but they also need to be put into context.

There is some evidence that China’s strong economic rebound from the coronavirus pandemic has lost some momentum, and this will have dampened demand growth for copper, a key component in construction and manufacturing.

But there are other factors driving the soft imports, namely the sale of strategic reserves as Beijing acts on its view that London-traded copper’s rise to a record high earlier this year wasn’t justified by fundamentals.

It would appear that China has sold just enough of its copper reserves in the three auctions held so far to lower import demand, and also snap the rally, which saw the London contract peak at a record $10,747 a tonne on May 10, before sliding 13.9% to close at $9,747 on Wednesday.

In the short term, China’s copper imports may well remain subdued, given the economy and the likelihood of ongoing auctions of strategic reserves.

But over the longer term, China is likely to require increasing amounts of copper to drive its ambitious renewable energy targets, to switch its vehicle fleet to electric power and to build more new housing in cities.

Therefore, the softness in China’s current copper imports will likely be reversed at some point in the future, most probably when Beijing ceases to intervene in the market, or boosts stimulus spending in order to ensure growth targets are met.

Contrary coal

In some ways coal is the opposite of copper, with recent strength in imports likely to reverse over the longer term, even if there is resilience in coming months and into the upcoming northern winter.

China’s coal imports were 28.05 million tonnes in August, down from July’s 30.18 million.

While there was a dip in August volumes, it’s worth noting that July and August were the two strongest months this year for coal imports, and that they have now risen for three consecutive months.

But the robust outcomes are the result of short-term factors, including domestic output constraints as mines were shut for safety inspections, and strong power demand amid a hotter-than-usual summer and lower hydropower generation.

It’s likely that domestic output will recover in coming months, but it’s still uncertain if it will do so by enough to lead to lower imports, especially if power demand remains solid through the winter peak period.

However, beyond the coming months, the outlook for China’s coal imports starts to look less positive, given Beijing’s plans to use more domestic coal and increasingly shift power generation and household heating to cleaner forms of energy.

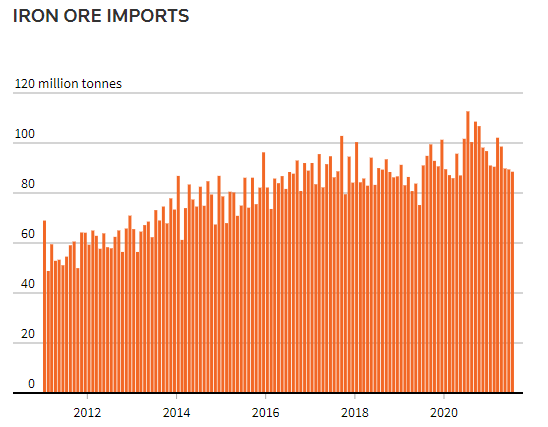

Iron ore imports also showed strength in August, rising for the first month in five to reach 97.49 million tonnes.

But the gain is more likely related to an easing of supply constraints, given prior weather-related disruptions and port work in top exporter Australia and coronavirus-related issues in number two Brazil.

For iron ore, the key to the outlook is how determined Beijing is that annual steel output will be limited to no more than 2020’s record 1.065 billion tonnes.

Steel output dropped 7.6% in July from the prior month to 86.79 million tonnes, but it will have to decline more for the rest of the year to stay below the 2020 level, given production was 649.33 million tonnes in the first seven months of the year.

For LNG, while demand for natural gas remains strong, the current high spot prices may deter Chinese utilities from buying additional volumes beyond what they have contracted.

But China’s policies to use more of the cleaner-burning fuel are unlikely to change, meaning the longer-term outlook for LNG remains solid, and the country is almost assured of supplanting Japan as the world’s biggest buyer of the super-chilled fuel.

Overall, China’s imports of major commodities in August were not as strong as some commentators thought, but rather showed that the paths of individual commodities are starting to diverge from each other.

(Editing by Richard Pullin)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments