Uranium fundamentals remain but near term is flat

The spot uranium price of US$25.54/lb. for Q3/16 was lower than our estimate of US$27.00/lb. (-5.4%). With utilities well covered for 2016 and finding material in the mid-term market to satisfy intermediate needs. Our view continues to be that utilities will focus their buying in these shorter term markets until they are no longer rewarded with low prices to do so.

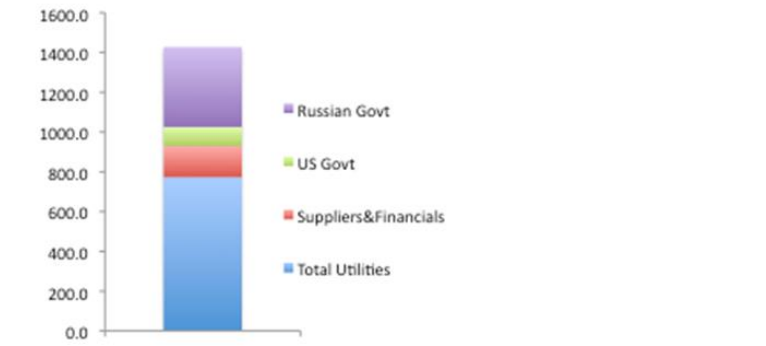

The key issue is global inventories and this has been the main subject of focus for the past month in the uranium space. Ux Consulting (“UxC”) recently estimated that there is the equivalent of 1.4 billion lbs of above ground uranium stockpiled in various forms.

UxC 2016 Global Uranium Inventory Estimate

Given that our estimate for 2016 uranium demand is 174M lbs there appears to be about eight years of supply available. Indeed the post-Fukushima shutdowns and slowdowns in countries such as Japan and Germany have contributed to this. Combine this with the fact that the utility demands for the near-term are well covered (UxC estimates that uncovered demand for 2016 is only 3.4M lbs or 2% of projected demand) and that they can procure uranium cheaply in the mid-term market as trading houses are taking advantage of low borrowing rates to facilitate a carry trade and we have the current situation where low demand is meeting lots of perceived inventory. As a result the uranium spot price dipped briefly below US$20/lb recently. We see this situation persisting for the better part of a 12-month period before uncovered requirements whittle inventory levels low enough for a meaningful upward price response in the spot market. Or if borrowing rates rise to a point where the carry trade no longer makes sense for traders to supply into the mid-term market.

Rob Chang, Managing Director and Head of Metals & Mining, Cantor Fitzgerald

While the 1.4 billion in inventory appears to be a massive number we need context. We have little data on what inventory levels have been historically but we can surmise that they were actually higher. This is because we have been in a global supply deficit since the mid-1980s. Despite this, we did see U3O8 prices top out at US$136/lb in June 2007 when uranium inventories must have been higher than what they are today. The difference between now and then is likely that we were not aware or as focused on the global inventory levels at that time and focused more on the growth of nuclear.

We continue to believe a violent increase in the price of uranium is coming and we look no further than the following data points. According to data publicly released by UxC, 73M lbs of uranium demand remain uncovered for 2020, which is 38% of its projection for that year (34% of Cantor’s forecast). The figure grows to 174M lbs uncovered by 2025, which is 80% if UxC’s projected demand (77% of Cantor’s forecast). For context, the 174M lbs figure is Cantor’s forecast for uranium demand for all of 2016 and is about 8M lbs greater than UxC’s total expected production from new and existing mine production in 2025 – of which some of that production is pledged to the committed portion of the 2025 demand.

Let us stress this last point. The amount of uncovered demand alone in 2025 is more than the total production from all sources in 2025. The fact of the matter is the low price environment has choked off exploration activity for uranium and we are at the point where there are not enough uranium projects in the pipeline that can adequately meet the upcoming demand. As such, global inventories will be dramatically whittled down.

Utilities will be (and some already have been) looking to secure long term contracts to cover these requirements. However they will learn that few producers (if any) will be willing to contract substantial amounts of material at the current long term contract price of US$37/lb. This is because the marginal cost of production of current producers is in the US$40-50/lb range. Moreover, the incentive price required to start-up the large African uranium mines that have the resource size needed to produce uranium for future supply and demand equilibrium is likely in the US$80-90/lb range. This is the reason why the Chinese are commissioning the start-up of Husab in Namibia, which some African uranium mining experts have noted that its all-in sustaining costs are likely

>US$60/lb .

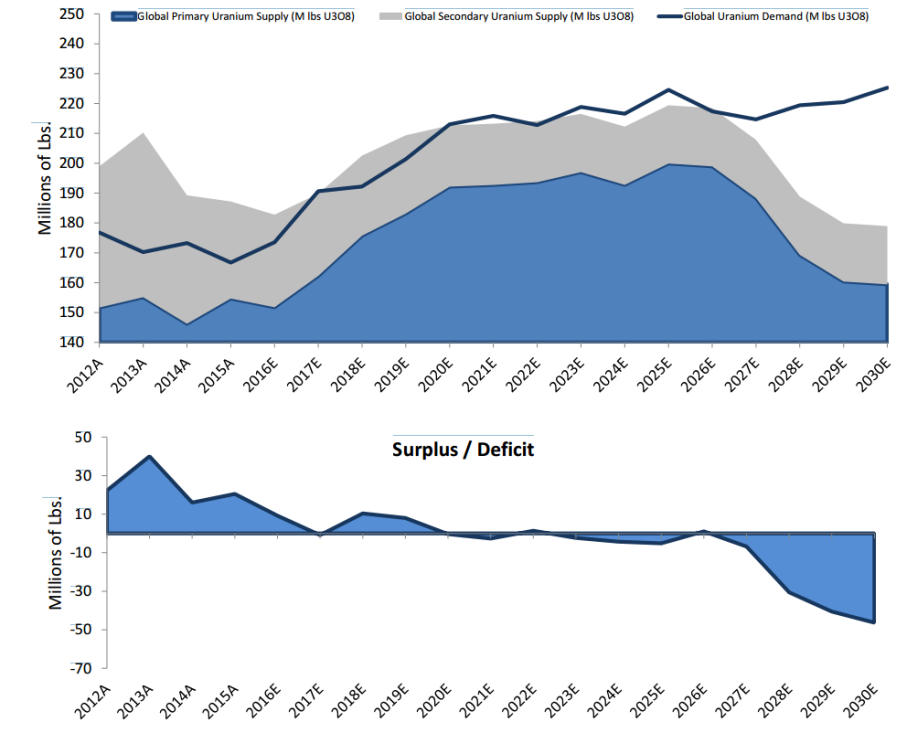

Cantor Fitzgerald Canada Research continues to present two supply and demand models:

The first is our traditional supply and demand model that is very conservative in that it assumes all uranium producers will produce at their forecast production levels and that all new uranium projects will start on-time and exactly according to their expected ramp up forecasts regardless of market price. These include projects that have break-even costs estimated in the US$70/lb level and higher.

Uranium Supply & Demand Forecast – Conservative

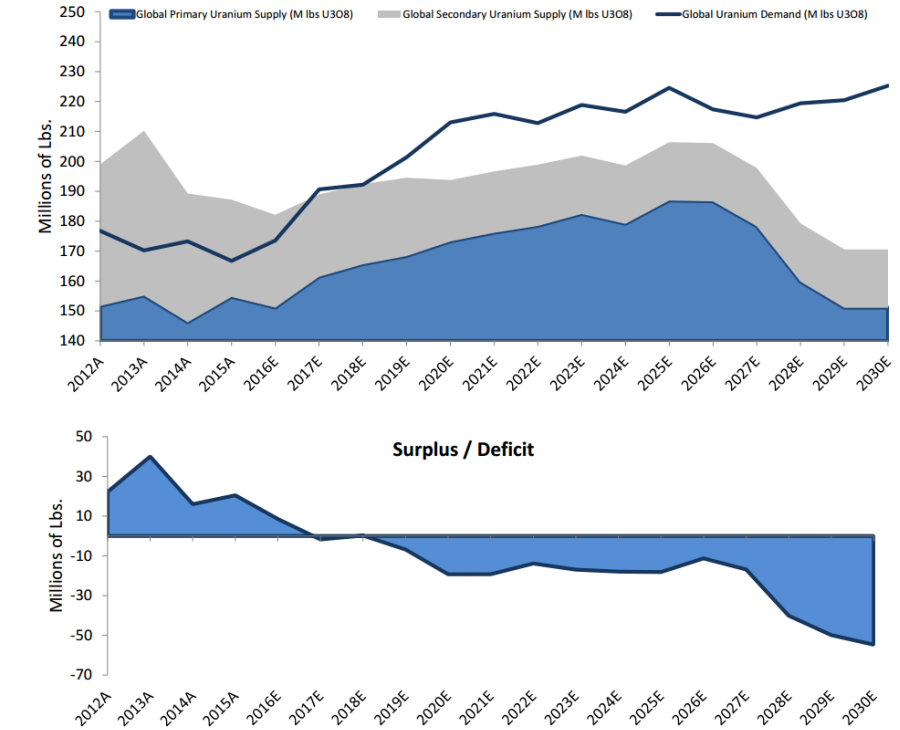

The second is an adjusted uranium production forecast assuming uranium prices remain at US$40/lb for the foreseeable future. In this model we forecast production shutdowns based on the estimated expiration of long term contracts.

We view the second scenario as the more realistic one since it is unreasonable to assume producers will continue producing at a loss indefinitely. Moreover with spot uranium prices currently closer to US$20/lb, there would be even fewer producers that can survive. In both scenarios, an unavoidable shortfall between supply and demand occurs.

Uranium Supply & Demand Forecast – US$40/lb long-term

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments