A turbulent year for alumina market could get still worse

LONDON, July 31 (Reuters) – Alumina is having a turbulent year.

The intermediate product sitting between bauxite and refined metal on the aluminium production chain doesn’t normally grab the headlines.

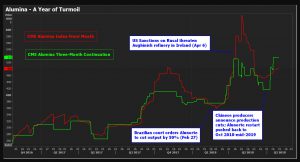

But it did in April, when the spot price doubled to over $700 per tonne as the market reacted to U.S. sanctions on Oleg Deripaska and his Rusal empire.

The sanctions threw into doubt the future of Rusal’s Aughinish alumina plant in Ireland, threatening a second blow to global production after the part closure of the Alunorte refinery in Brazil.

Aughinish won a reprieve as the U.S. Administration extended the sanctions deadline and the betting is that a political deal to lift the sanctions altogether will be achieved very shortly.

However, while the aluminium price is now trading back at pre-sanctions levels, that of alumina isn’t.

Alunorte remains part suspended and Chinese alumina refineries have started cutting production.

The latter may be a sign of things to come, promising further turbulence ahead.

Graphic on CME alumina price:

Sanctions spike

When the United States announced the imposition of sanctions on Rusal on April 6, it was the aluminium price that reacted first. London Metal Exchange (LME) three-month metal rocketed from $2,000 per tonne to a seven-year high of $2,718 in the space of a couple of weeks.

It took around a week for alumina to follow because that’s how long it took the market to unravel Rusal’s internal supply chains.

On paper the company looks vertically integrated with its own bauxite mines, alumina refineries and aluminium smelters.

The reality is a bit more complicated.

The market has something new to worry about in the form of falling Chinese alumina production.

Aughinish, it turns out, largely runs off bauxite supplied by Rio Tinto, which in turn takes a good part of the plant’s two million tonnes of annual production to feed aluminium smelters in Europe.

Rio Tinto declared force majeure on supplies of alumina to some customers on April 18, which is when the alumina price exploded higher.

It turned out to be only a notional force majeure since the extension of the sanctions deadline to Oct. 23 meant no interruption to actual deliveries, the company said in its Q2 operations report.

But even the threat was enough to trigger a panic in the physical alumina market, which was already trying to adjust to the loss of half the output at Hydro’s Alunorte refinery.

Alunorte, the world’s largest single alumina plant with annual capacity of 6.3 million tonnes, was ordered partially to curtail operations by a Brazilian court in February on environmental grounds.

The operational wind-down and any associated spot market buying by Hydro was still happening when the sanctions shock hit the market.

No return to business as usual

Alunorte is still operating at only 50 percent of capacity.

This explains why the CME’s front-month alumina contract , indexed against S&P Global Platts’ assessment of the spot market, is currently valued at $481 per tonne, compared with under $400 at the start of the year.

Indeed, Hydro has dampened expectations of any quick fix with the Brazilian authorities.

“The process to resolve the situation in Brazil is challenging and has taken longer than expected,” said Chief Executive Officer Svein Richard Brandtzaeg. “The timing for resuming full production remains uncertain.”

The company’s best guess is that a restart will take place sometime between October this year and the middle of next year.

The uncertainty hanging over such a big component of global alumina supply is evident in the CME alumina contract’s forward curve.

The price of alumina for three months forward is currently sitting at $515, higher than it was at the peak of the Rusal sanctions scare.

That’s also because the market has something new to worry about in the form of falling Chinese alumina production.

State-owned Chalco warned early July that around 770,000 tonnes of its annual alumina capacity would be subject to “flexible” output arrangements. Or output curtailments, as everyone else would call them.

A day later another producer, Luoyang Heungkong Wanji Aluminium, said it too would be cutting output to the tune of an annualised 680,000 tonnes.

Others have followed.

Five major Chinese refineries have now significantly cut output, according to specialist research house AZ China.

That raises the prospect of China, which has historically tended to be a net importer of alumina, having to tap the international market for more material precisely at a time when there is little or no supply slack.

Blue skies, red alert

The problem for the alumina market is that these Chinese cuts are down to an environmental crackdown that is only going to get more punitive in the weeks and months ahead.

Beijing’s “blue skies” war on smog has embraced the entire aluminium production process chain in China but it’s only recently that environmental investigators have turned their attention to the bauxite mines that feed the chain.

Bauxite operators in Henan province have already been hit and the crackdown is in full swing in Shanxi province, causing a shortage of raw material that in turn is forcing the shuttering of alumina capacity.

“This is just the beginning of the process,” according to researchers at Wood MacKenzie. The outlook is for further closures to “exacerbate bauxite shortages, which in turn could lead to further refining cuts.” (“Why is the Chinese aluminium industry feeling blue?”, 26/07/2018)

Alumina refineries are themselves also likely to be directly impacted by the coming winter heating season restrictions, particularly since the government’s latest three-year plan to reduce air pollution vastly expands the targeted area and extends it beyond last year’s November-March time frame.

This year the curtailments will kick in from September and last year’s “26+2” target zone around Beijing and Tianjin will be expanded to include the Yangtze River Delta and the Fenwei Plain, comprising parts of Shaanxi, Henan and Shanxi provinces.

Since around 70 percent of China’s alumina capacity is located in this year’s targeted areas, the impact is going to be much greater than last year.

Throw in the intensifying scrutiny of the bauxite sector and the pressure on alumina refineries to switch from coal to gas power over the winter months and, to quote WoodMac, “there could be more chaos to come”.

They mean chaos in China’s giant aluminium sector.

But more chaos in China will easily translate into more price chaos in the international alumina market.

(By David Evans)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

{kind=link}

Comments