The new coal miner pitch: Don’t mention coal

Gray? Try “steel-colored.” Angular? You must mean “steel-inspired.” I’m referring, of course, to the new logo of the rechristened Arch Resources Inc.

The old logo, with its stylized fragment of St Louis’ Gateway Arch, was fine — apart from the fact that it had the word “coal” in it. Arch Coal, the company’s old name, was a mite too connected with a certain fuel that is not only in terminal decline in the U.S. but also rather unpopular with the ESG crowd.

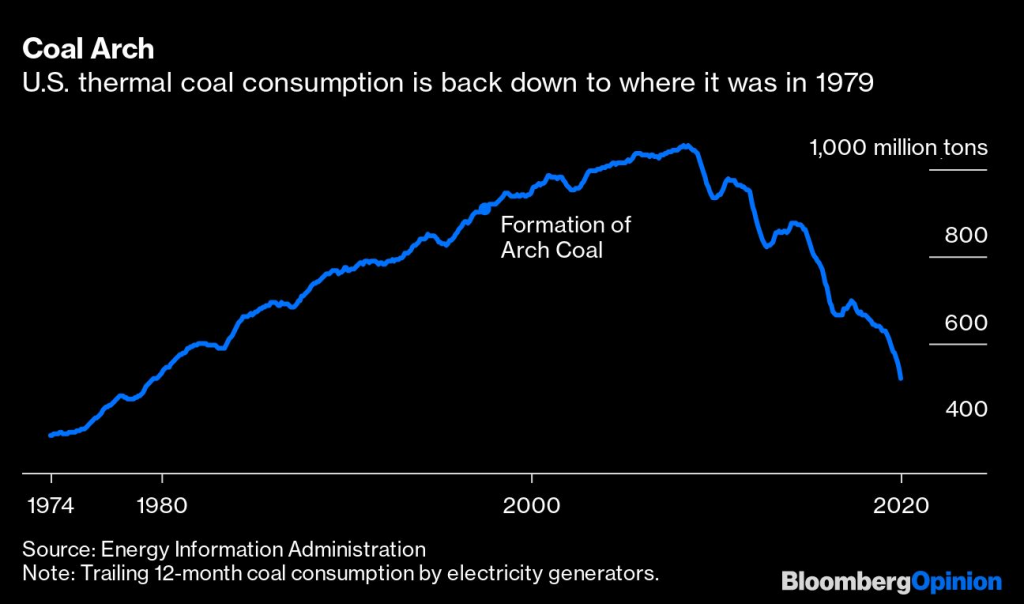

When Arch Coal was formed in 1997, America’s power stations were burning 900 million tons a year, generating more than half the country’s electricity, and climbing. Today, thermal coal accounts for less than a fifth of the mix:

Remarkably, in announcing its name change this week, Arch pulled a Voldemort with the word “coal”: It doesn’t appear anywhere in the main body of the press release. This is doubly impressive when you consider Arch Resources will in fact continue to mine prodigious quantities of … well, you know. Thingy.

Only Arch is now focused on a different class of thingy. Metallurgical coal is thermal coal’s more prosperous sibling, a vital ingredient for making steel; hence Arch’s steely new logo. Except Arch refers to these black rocks dug out from the ground not as metallurgical coal but as metallurgical products.

Corporate rebranding tends to offer a rich seam of material, but Arch’s new name is actually a logical progression in a logical strategy.

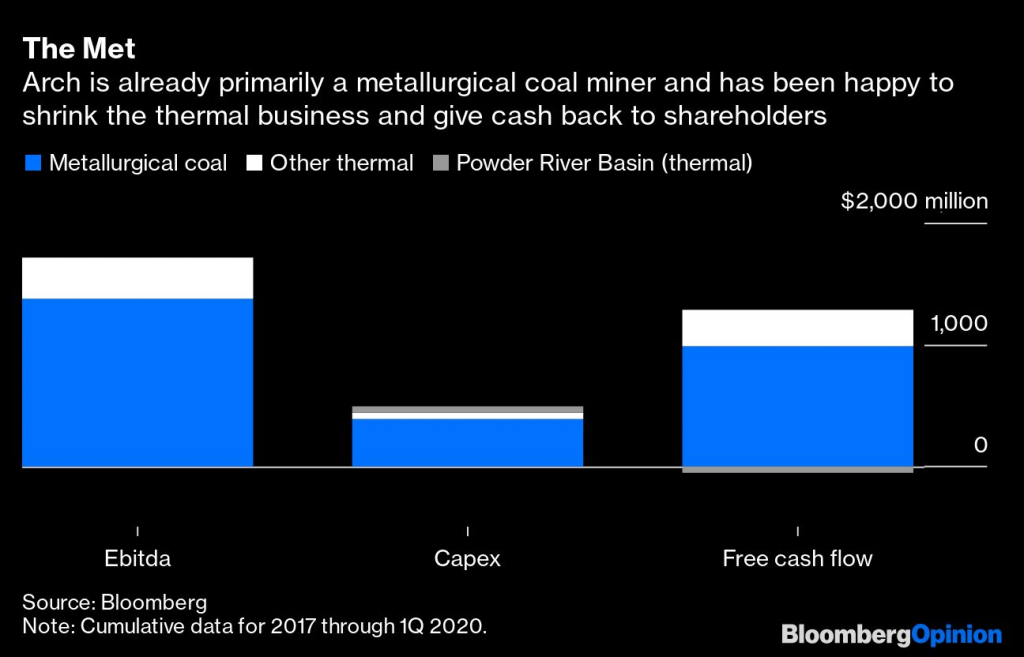

Ever since the miner emerged from chapter 11 in 2016, its approach has been one long tacit acknowledgement that the US thermal coal industry is in a downward spiral. That business has essentially been run for cash, with capex running at just 70% of depreciation, and the company’s Powder River Basin assets are about to be subsumed into a joint venture with Peabody Energy Corp. The more profitable metallurgical business, meanwhile, is expanding, with a major new project in West Virginia underway. Most importantly, though, for every dollar Arch has invested back into the business, it’s spent about $1.60 on stock buybacks, taking in 40% of the shares. This is how you head into the sunset.

So the new name and Terminator-esque logo aren’t just some branding consultant’s WFH project. It’s the latest step in Arch’s quest to carve out a new life after death. For example, see this from the announcement:

We expect steel to play an essential role in the revitalization of the global economy as it recovers from the disruption of the covid-19 pandemic, and in the construction of a new economy supported by mass transit systems, wind turbines and electric vehicles.

See? No mention of coal, but a cameo by wind turbines, no less (ah, the irony). Mad Men’s Don Draper once pitched Bethlehem Steel on advertising itself as producing the building blocks of America’s great cities. In real life, Arch would like you to know it mines the building blocks that go into making those building blocks.

On one level, that’s par for the course. Any commodity producer would like you to associate their otherwise standard product with something more exceptional and valuable; similar thinking underlay Arconic Corp.’s split from aluminum smelter Alcoa Corp. Metallurgical coal may be higher-margin, but it remains a commodity, with all the volatility that entails; the stock has halved so far this year. Far better to focus minds on something more stable, like a T-bar.

In this case, though, there’s a bigger drama playing out, and the wind turbine is the key character. While Arch’s announcement lacked “coal,” it provided my annual quota of “environmental, social and governance” mentions in the space of a few minutes. Arch is still running its thermal coal mines and likely will for as long as they spit out cash. But competition from cheap shale gas and renewable energy has made thermal coal a tough sell to investors already. Now climate change is making it altogether taboo — regardless of how efficient the miner — as ESG considerations gain traction.

The ongoing rebranding of Big Oil as Big Energy reflects similar dynamics. As the function of energy markets shifts from simply producing ever more tons or barrels or whatnot to optimizing supply, demand and emissions, so the expectations of the capital markets shift, too.

The multiple that makes a stock price is ultimately just some narrative about the future expressed as a number (for an extreme example, see Tesla Inc.). It isn’t just that Arch’s old story no longer convinces; it’s increasingly unacceptable and thereby a burden on, rather than a boost to, value. Becoming truly steel-inspired requires being a touch coal-amnesic.

(By Liam Denning)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments