The making of an Athabasca rockstar

James Sykes disregarded management directive and kept the drill going. He had already waited a year to finally drill ‘Area C’, and had just cleared the overburden before the call came down to pack up and head back south. The drill was to be deployed closer to a neighbouring discovery, where results have been dubious to date, but made for a better story. A critical element for any exploration mining play, especially true for uranium juniors who were still mired in one of the worst bear markets in decades.

While James was only 33 at the time, he already had a decade of uranium exploration in the Basin under his belt and knew ‘Area C’ held something special. And his insubordination was vindicated on February 19, 2014, when NexGen Energy (TSXV:NXE) announced the discovery of a new zone of uranium mineralisation in the Rook 1 project in SW Athabasca Basin.

NexGen’s stock price skyrocketed in one day and the company is now arguably one of the best uranium development stories on the market, boasting a market cap of C$800 million.

If you know James Sykes like we do, then you know that uranium flows through his veins. Probably even literally being the son of a uranium miner and having spent his entire professional career looking for it. Nothing satiates his mind more than uranium exploration, and he is the only geologist we know that has looked over 600 core samples just for fun. James’ end goal is to be the most successful Athabasca uranium explorer and to discover 1 billion pounds of U3O8, which, in all honesty, would probably push him to find more.

To get to these lofty goals, James is all-in with his newest venture, but before we delve into the company, we need to explore how James became an expert of the Athabasca Basin in the first place, and why we are betting a lot of money he can replicate his past successes.

Born Into Uranium

James Sykes was born in Elliot Lake, Ontario, a city that owes its very existence to uranium mining. The uranium frenzy was ignited when a deposit was discovered in 1953 and the Ontario Provincial Government created an initiative to develop the area into a full-fledged mining town. The result thereafter was fourteen uranium mines and for the next forty years the district produced the lion’s share of the world’s uranium.

After graduating from Elliot Lake High School, James packed his bags for Waterloo, where for the next three years he earned a Bachelor of Science Degree in General Studies. It wasn’t until the tail end of his  education he was steered towards his natural calling in geology. James thanks a passionate professor for fanning the flames. And for the next two years James honed his knowledge through self-study, and finally formalized it by obtaining an actual degree in Geology from Dalhousie University.

education he was steered towards his natural calling in geology. James thanks a passionate professor for fanning the flames. And for the next two years James honed his knowledge through self-study, and finally formalized it by obtaining an actual degree in Geology from Dalhousie University.

Naturally, James’ focus was in uranium, and when an opportunity arose with Denison Mines (TSX:DML), James packed his bags again and headed for northern Saskatchewan, or the Athabasca Basin, home to 22% of the world’s uranium output, and where James would lay his roots and begin his legacy.

James’ first assignment was that of a junior in the Wheeler River project, but in just three months the Project Manager, who ironically hired James, quit and the duty was thrust upon the recent grad – talk about trial by fire. And as James stated himself, he suffered deliriously from recent graduate syndrome; he knew everything and was determined to prove this by taking the reins.

Fortunately for James, he was quickly put into place and rather than leading, began working with the older group of mining veterans and in putting together the puzzle that was Wheeler River. Concurrently, James personally managed the joint venture with perennial uranium powerhouse, Cameco Corp (TSX:CCO), and JCU, a Japanese conglomerate owned by ITOCHU, Mitsubishi, and OURD, securing personal ties and relationships with the largest players in the sector.

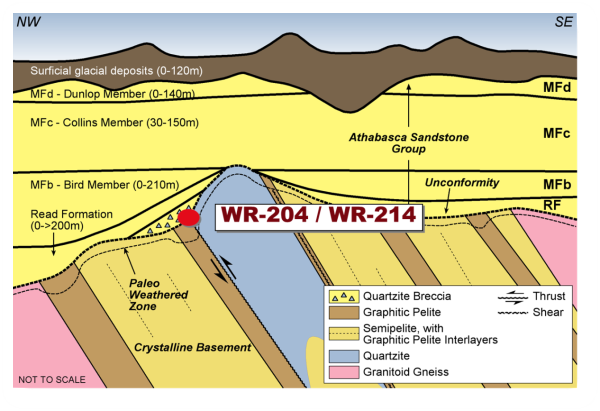

In addition to being mentored, James began spending all of his free time in the core shacks, logging the new while studying the old. His fascination and obsession was apparent: no one hangs out in a core shack for hours after work willingly. Cameco had been drilling in Wheeler River since the 1980s, and all the smoke was there for multiple high-grade uranium deposits. As fate had it, the first drill hole James ever logged was WR-214, the best intersection to date yielding 3.8 meters of 0.85% eU3O8; the Wheeler River team were close to something big.

When James started in May 2006, Denison’s geologists were comparing Wheeler River to the prolific McArthur River project; however, at the time were exploring on the wrong side of the quartzite:

Source: Denison Mines

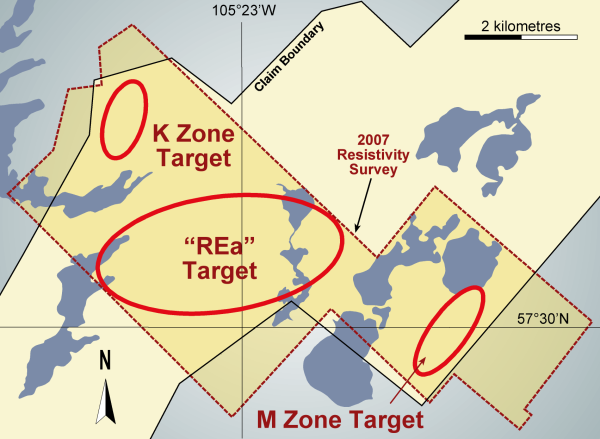

It was not until late 2007 that the team decided to go to the footwall, but unfortunately for James, he was on his way out; however, not before working with the other geos in picking out three exploration targets:

Before his departure and during the summer of 2007, James was out at the core racks as usual when he stumbled across the historical ZK holes (ZK-04 and -06), and made the connection between that area and Cameco’s Millennium deposit. James was on-site at Millennium in 2006 and one of the features that caught his eye was the clay alteration, which was identical to that of the K Zone Target. This information was used in conjunction with existing identified uranium mineralization and the workings of Gary Cohoon and Roger Wallis, who were pounding the table to drill the REa Target.

REa eventually became Phoenix, and the K Zone became Gryphon. Today the Wheeler project hosts 114.3 million pounds of U3O8, and is the highest grade undeveloped uranium deposit in the world.

So what prompted James to leave when he was obviously on the heels of a major discovery?

First, an opportunity arose at Forum Uranium (TSXV:FDC) to work with two of the most reputable Athabasca uranium geologists in Ken Wheatley, AREVA’s Senior and District Geologist, and Boen Tan, the key figure in the discovery of the Key Lake uranium deposit in 1975. Second, a more seasoned Project Manager was finally brought on to replace James and he quit in spite. These points will be a reoccurring theme throughout James’ career: the insatiable thirst to learn, and hot-headed stubbornness, which in case James’ case is actually a virtue.

Alas, James’ stint at Forum was valuable, but also short. The 2008-2009 financial crisis hit uranium explorers especially hard, with uranium prices crashing from its peak of more than $140 per pound to almost $40. James and the rest of the crew was let go, but he quickly landed on his feet.

The Next Chapter – Hathor Exploration, Rio Tinto, And NexGen Energy

James’ next gig was at Hathor Exploration, the hottest uranium explorer at the time. Hathor had just discovered the Roughrider Deposit’s West Zone, and had C$20 million in the treasury to aggressively follow-up with the hole and advance its eleven other projects.

Like at Denison, James made his home in the core shacks and racks which, to his chagrin, was an absolute mess. As James puts it, there was no continuity, no sections, and no system. There was nothing that was ‘holding anything together’, so James cranked up the heavy metal (self-professed metalhead) and began work on a model to help with interpretation and to firm-up the mineralization.

James’ bosses were ecstatic with what he built, and he was commissioned to continue work by picture relogging. In just two months’ time Hathor finally had its first legitimate 3D model. Prior to the James model, Hathor had assumed the strike was running north-east, however, it was in fact trending east to west. Utilizing the James model, Hathor soon discovered the East Zone, which was followed up with the Far East Zone.

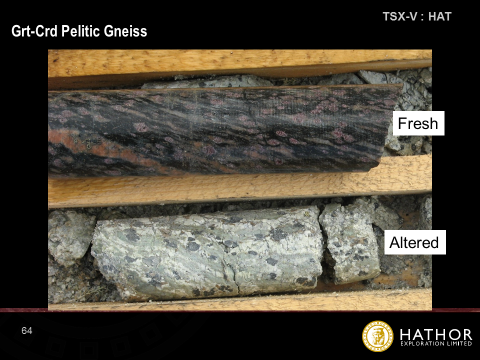

Roughrider core, clay alteration which is identical to Cameco’s Millennium and Denison’s Gryphon

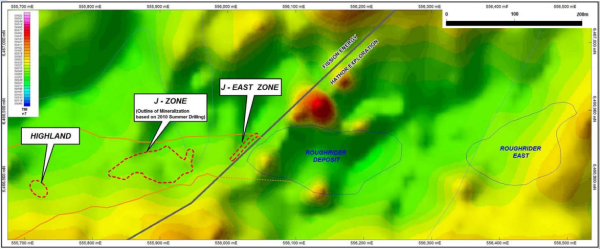

Fission Energy, the predecessor of Fission Uranium (TSXV:FCU), was the direct beneficiary of James’ work. All they had to do was line up their rig with Hathor’s and drill:

Source: Fission Uranium corporate presentation

In January 2010, Fission Energy announced the discovery of the J-Zone, which included an intersection of 5.55% U3O8 over 15.5 meters (drill hole WAT10-0103). We mention this tidbit because at James’ next gig he was forced to apply the same strategy, but more on that later.

Due to James’ success, he was offered the role of the Manager of Roughrider, but James loved grassroots exploration so much he declined the role and asked to become the Project Manager of Russell Lake, a project Hathor considered a tier-one exploration project. At that point in time, Russell Lake had garnered the interest of the boys and multiple JV attempts were shot down.

James’ tenure at Russell Lake began in the summer of 2010, and started right back in the core shack, relogging the project and identifying some key areas of interest. For the next year James managed three drilling campaigns which cumulated during the fall of 2011. The last campaign would be a five-hole drill program at the M-Zone Extension (MZE) of the property, or where Denison’s M-Zone supposedly extended into Russell Lake.

Through his work, James was able to identify three new zones in previously untargeted and untested areas. While the basement-hosted uranium mineralization was sub-economic, it was another Eureka-moment for James, verifying his theories and concepts learned to date. Three out of five holes hit mineralization at MZE, something that was never released due to a press black-out. It was during this time Cameco and Rio Tinto were in a heated bidding war for Hathor. To this day James loses sleep over Russell Lake. The question still looms over his head – is Russell Lake host to an economic deposit?!

James stayed on with Hathor until it was acquired by Rio Tinto in what was one of the more exciting bidding wars in the junior mining game. In August 2011, Cameco announced the hostile bid for Hathor in an all cash consideration of C$3.75, or what amounted to C$520 million. The bid was immediately rejected by Hathor, claiming the offer was “predatory” and “opportunistic”. Cue the white knight, Rio Tinto offering C$4.15 cash per share, or C$578 million, precariously close to the October 31, 2011 deadline set by Cameco. Nonetheless, a bids a bid and Hathor’s board unanimously recommended to accept this offer and even baked in a C$20 million break fee.

Right away the mining community knew Cameco would respond, and respond in a big way. Because of the break fee, and investors began peculating Cameco’s response would be at least C$4.40, and they were right. On November 14, 2011, the bid was increased to C$4.50 cash per share, or C$625 million. Cameco decided that Hathor’s Roughrider project was integral to their plan for growth beyond their goal of doubling production by 2018. The proximity of the acreage to their existing projects and facilities were too synergistic to give up without a fight.

Rio Tinto’s last bid came just three days after, raising their offer to C$4.70, or C$654 million. While the market urged Cameco to respond, Cameco conceded a week later, not allowing their corporate ego to get in the way. The bidding war was finally over, and James Sykes, yet again, had a new employer.

By now our readers probably know James would not do too well in a large corporate and a bureaucratic setting. The red tape and almost daily meetings got to James immediately, and he approached Michael Downes of Mega Uranium (TSX:MGA). Michael and company had just acquired a portfolio of Canadian exploration assets from Titan Uranium; projects with significant merit James had his eyes on, especially Rook I.

Source: Mega Uranium press release

Unfortunately, Mega Uranium was cash-poor, and James was forced to stay on with Rio, working on research projects for Athabasca uranium mineralization and the Roughrider deposit and system.

James big break came in August 2012, when Mega Uranium flipped the Canadian projects to NexGen Energy (TSXV:NXE). The day following the announcement, he gave Leigh Curyer a call and after some jockeying back and forth, was hired in May 2013:

“James Sykes has joined NexGen as a senior geologist. Mr. Sykes joins NexGen from Rio Tinto. He originally commenced with Hathor in 2007 prior to the discovery of Roughrider and transferred to Rio from Hathor in February, 2012, as part of its acquisition of Hathor. Mr. Sykes was a key member of the team that constructed the original 3-D geological model of the Roughrider system, which ultimately led to the discovery of the Roughrider East and Far East deposits. Prior to Hathor, Mr. Sykes was a project geologist with Denison Mines Corp.”

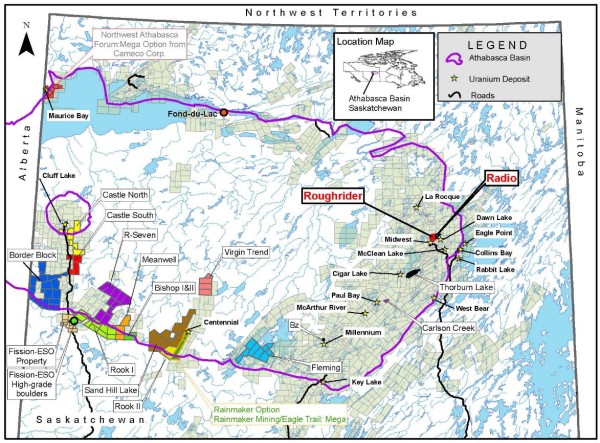

Radio was to be NexGen’s first property to drill, located immediately east to the Roughrider deposit and obviously James’ speciality. Second on the priority list was Rook I, located immediately adjacent to the northeast of the Patterson Lake South (PLS) uranium discoveries. The surprising part here is that James was more excited about Rook I than Radio, and was the only geologist who reached out to NexGen on it.

James’ appointment was announced concurrently with the plan to drill 4,400 meters at Radio, and in just one month NexGen was off to the races. At the same time, the company also initiated a DC resistivity survey in the southern section of Rook 1 to assist in the drill hole targeting of an upcoming 1,500 meter campaign.

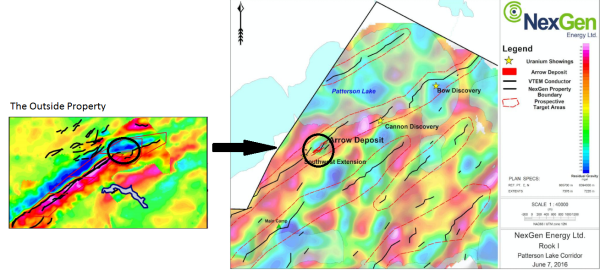

Although uranium was still mired in the post-Fukushima slump, the Athabasca Basin began generating significant buzz, led by the massive discovery of Patterson Lake South (PLS) by Dev Randhawa’ Fission Uranium. PLS was pulling out impressive grades and quickly became the market darling, Leigh pivoted focus to Rook I, and doubled the drill program to 3,000 meters. NexGen huddled and it was decided ‘Area A’ would be the first target, despite James’ declaring ‘Area C’ should be first. ‘Area A’ was closer to the PLS border, and in accordance to a weighting scheme devised by management, there was more factors that swayed the vote to begin drilling there first.

Full circle. James was finally able to drill ‘Area C’ in the winter of 2014, and broke a couple of rules to get NexGen on the radar. Using what he learned from Russell Lake, James drilled 200 meters into the basement and kept going. By the end of it, the first hole at Arrow, RK-14-21, went down almost 700 meters and yielded four zones of mineralization; NexGen was forced to halt their stock before releasing the news and when they finally resumed trading the stock almost doubled.

During the same drilling campaign, the plan was drill 15-20 meter step outs, but in typical James-fashion, he chose to drill 215 meters away. James knew he had overshot the target with his first hole, and during the night moved a drill and proceeded to drill RK-14-30, once again disobeying orders. On March 30, 2014, NexGen announced the results and it was the best hole to date, encountering the widest and strongest radiometrically anomalous zones. On the tails of the discovery, NexGen raised an astonishing C$11.5 million to continue drilling Rook I in what was looking like a massive deposit(s).

James’ last campaign with NexGen targeting drill holes was summer 2014. He had collared AR-14-15, the company’s first scissor hole, and was told explicitly to not drill past 500 meters. Drilling was just about complete and the brass emailed James to shut down the rig that night. Nonetheless, James looked at the data and knew the target had not been reached, and continued drilling like a cowboy. By the end of it, James drilled to a total depth of 750 meters with the intersection made at 527 meters; it was NexGen’s first continuous intersection of high grade uranium and most intense mineralization to date. It was the discovery of the A2 sub-zone.

With most of the heavy exploration work done, during a very snowy winter of 2015, James was assigned to geological management. The exact cause of reassignment was not known, but we have a feeling the decision was an especially hard one. With the thrill of exploration always on his mind, and feeling spited again, James and NexGen eventually departed in what was a precarious but thrilling relationship.

James Finally At The Helm – Appia Energy (CNX:API)

Feeling somewhat jaded, James took a breather from the uranium game.

However the pull of exploration and uranium was just too strong and less than a year later James began looking for his next opportunity.

At this point we have established James Sykes is some sort of uranium exploration savant, but maybe a little difficult to manage. The ideal situation for James was to run his own ship, and he found that break in Tom Drivas and Appia Energy.

Full circle again, and back to Elliot Lake. While James was going through potential uranium companies to transact with, he came across Appia Energy, a relatively new company in the public space, listing on the Canadian Securities Exchange in June 2014. What stood out the most was Appia’s large resource in Elliot Lake, 55.7 million pounds in 43-101 compliant resource, and another 199.2 million pounds in historical. While the resource is impressive, the grades are low, and James approached Tom with an alternative strategy to get Appia in the spotlight.

James gave Tom his full story, sparing no detail, and highlighted two projects he would like to stake. To Tom, hiring James was a no brainer, on April 14, 2016, James Sykes was appointed Director of Saskatchewan Operations, and the Otherside and Loranger properties were staked soon after. James finally had his vehicle, and two properties staked specifically to register his name in a big way.

The Otherside

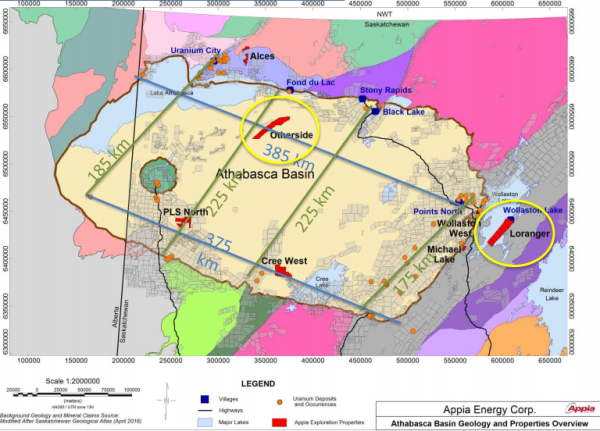

James staked the Otherside because of the similar characteristics it had with ‘Area C’, or better known as Arrow. The 21,868 hectare property features a 44 kilometers conductive trend that measures 2 kilometres across. Within that conductive trend are discrete electromagnetic (EM) conductors that are interpreted to be responding to graphitic faults within the basement rocks. The discrete conductors are long and continuous themselves, with some of them bifurcating into two and/or merging into one. One conductor in particular is perfectly coincident with the gradients of both airborne magnetic and gravity survey results.

The Otherside has already had some exploration work, and all of the airborne geophysical surveys flown over the property to date (magnetics, gravity, EM) reveal a ‘bend’ that shifts the geophysical features from northeast linear orientations to east-northeast linear orientations. At this ‘bend’ James observes subtle geophysical anomalies within each of the surveys, such as a slight change in magnetic signature, an offset of the coincident conductor, and changes within the gravity signature from a high to a low. It is these latter two features, the offset conductor and gravity low anomaly that were instrumental in James prioritizing ‘Area C’ as a tier 1 target for Rook I.

The conductors on Outside and Rook I are offset in the same fashion

Loranger Property

The Loranger property is 24,755 hectares that includes a 31 kilometres conductive trend that hosts at least 5 EM conductors, all observed to either bifurcate from/merge with one another. Numerous ‘bumps’ and ‘jogs’ are observed within each of the conductors, as are areas of signal degradation, which are interpreted to be possibly related to hydrothermal clay alteration associated with a mineralization event or a change in the geological nature of the rocks themselves. Most importantly, the main conductor trend terminates in a fold nose, very similar to other known high-grade uranium deposits, such as Key Lake and even Roughrider.

One feature of Loranger that James is especially interested is the conductors are all steeply dipping, while all the conductors outside of Loranger are observed as shallow dipping. This inflection of graphitic conductors was another prominent feature at Arrow, observable both geophysically and within the core. A change in orientation from shallow dipping structure to steeply dipping structure has also been interpreted to control the mineralization site at McArthur River, the largest high-grade deposit in the world.

Betting On James Sykes – Moving Forward

James has outlined an exploration budget to get to drilling for both Otherside and Loranger and Appia is currently raising C$2 million in two $1 million financings, a hard financing and flow-through, and recently closed C$263,000 in the first tranche of financing.

At Otherside, James has budgeted $300,000 for ground TAMT and another $105,000 for ground gravity. This will get James drilling, which he is planning for January 2017, a two hole campaign for 2,000 meters which is estimated to cost $750,000. Otherside is in a fairly remote area, and further in the basin, thus will be more expensive to explore and ultimately drill.

Loranger is closer to existing infrastructure, but is still considered ‘underdog’ and overlooked because past explorers have been afraid of where it is located on a regional scale, located well past the eastern boundary of the basin. James has budgeted $172,400 for an airborne EM, and another $135,000 for ground gravity. Drilling is also planned for January 2017, but this campaign will include ten holes planned over 2,000 meters for $750,000.

Here is the current financial snapshot of the company, post-financing:

Current Price: C$0.20

Shares Outstanding: 51.6 million

Market Capitalization: C$10.3 million

52-Week Range: C$0.01 – C$0.30

Cash: ~C$2.6 million

Total Liabilities: C$0.6 million

As we mentioned earlier, Appia Energy in itself is a great optionality play on uranium, currently trading at 18 cents per pound in the ground uranium, or 4 cents per pound if you include Appia’s historical resources. The resource gives Appia a great back stop and downside protection, however, in our opinion, like any other exploration play, the real value and investment comes from betting on the right people, and in this case is James Sykes and industry veteran Tom Drivas.

This is an exciting play and we have participated in the first tranche of the financing. The upside potential of Appia’s exploration assets is enormous, and the optionality of the existing uranium at Elliot Lake is just the free call option. Let’s go James!

Don’t bet against the fro

Palisade Global Investments Limited holds shares of Appia Energy. We receive either monetary or securities compensation for our services. We stand to benefit from any volume this write-up may generate. The information contained in such write-ups is not intended as individual investment advice and is not designed to meet your personal financial situation. Information contained in this report is obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The opinions expressed in this report are those of Palisade Global Investments and are subject to change without notice. The information in this report may become outdated and there is no obligation to update any such information.Do your own due diligence.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments