The hawkish dovish Fed

US markets are a bit of a mess right now. On Friday the S&P lost 53 points or 2.4%. Monday they regained half that ground but Tuesday saw another slide. The Dow made similar moves.

What gives?

The Hawkish Dovish Federal Reserve.

On Friday Boston Fed President Eric Rosengren, a member of the Fed Open Market Committee that decides on interest rate moves, said he was worried the long delay in raising rates was creating asset bubbles. Chalk one for the Hawks. In response, bond traders got worried and started selling, pushing prices down and yields up, and stocks fell in the now-classic response to the threat of the ‘end of easy money’.

Then on Monday another FOMC member, Lael Brainard, took the mic. She reinforced her reputation as a dove, saying the central bank would be wise to keep monetary policy loose. Chalk one for the Doves. In response, bond yields dropped as prices regained some ground and stocks got a lift.

Of course, these comments followed Janet Yellen’s late August Jackson Hole speech, which neither confirmed nor denied a pending hike. The talk was biased towards raising, based on strong jobs numbers in July and apparently strengthening inflation and GDP growth, though she did speak before the August jobs numbers came out.

The market obsessed over every word and didn’t know what to make of it. And so, with the September meeting looming, traders analyzed every word the Rosengren and Brainard said, searching for confirmation one way or another.

There are now no FOMC speeches to worry about for the next eight days, as we have entered the pre-meeting blackout period. The meeting will take place September 22 and Yellen insists it is ‘live’, meaning a hike is truly on the table.

As so for the next week markets will be cautious, preparing themselves for the possibility. Gold moving – falling – with equities is part of that.

The obsession over rates continues. It is both justified and ridiculous.

Justified

This seemingly endless period of rock bottom interest rates has created a mess.

Big picture: low rates means (1) debt has piled up, for governments and corporations, (2) companies have used debt to buy back stock, boosting prices by changing the denominator rather than adding value to the numerator, and (3) bonds yielding almost nothing (or less than nothing in many cases) have pushed investors towards ever-rising stocks in search of price gains, to replace their missing yields.

Does all of this change if Yellen increases rates by 25 basis points? Yes and no.

The debt will remain, because government and corporate debt loads are massive; the only difference will be a slight increase in service costs. Share buybacks are already running out of steam, leaving share prices to reflect corporate realities rather than financial engineering.

So those two are what they are.

It’s bonds where we have a problem.

Rock-bottom interest rates have wrought havoc on bond markets. Prices are unsustainably high, because the lack of yield has had traders pulling for price.

Any suggestion that story might shift via an interest rate hike creates major worry because no one wants to be last out when bond prices start to fall. And that could happen all of a sudden.

Bond king Bill Gross hit the nail on the head when he said, “Low yield bonds are especially vulnerable because a small increase can bring a large decline in price.”

We got a taste of that on Friday, when prices fell and yields jumped. But there’s a heck of a lot more where that came from. And it’s inevitable.

Rates will go up again at some point. However, inevitable is not the same as imminent. I don’t see a rate hike next week. (More on this in the Ridiculous section below.)

In addition, rate increases, even enough to cause a bond debacle, would cause chaos but gold would remain a Go To investment.

A bond debacle could be very significant. Companies and governments have to continually roll over their huge debt burdens, which requires constant bond buying. If prices plummet, much more money will get wiped out than a year or two of better yields can generate. That will limit the availability of bond investment dollars.

Then there’s the fear factor. A bond crisis would create enough uncertainty to hurt stocks in a big way, similar to how a banking liquidity crisis hurt markets in the global financial crisis.

Investors would flood towards safe havens. And there just aren’t many. Long-term government bonds might count, but rates would have to rise significantly before those would provide much yield.

The US dollar still counts right now, for security if not for upside potential; it’s difficult to know how that might change in a bond debacle. Real estate is another, in the right areas, though the US housing bubble created major fear around risk in real estate.

That’s the essence of the precious metals argument: that it is almost alone as a safe haven option. Of course, the need for safe havens is not because of low rates; low interest rates and high bond pricing are the result of a global economy that remains sluggish at best.

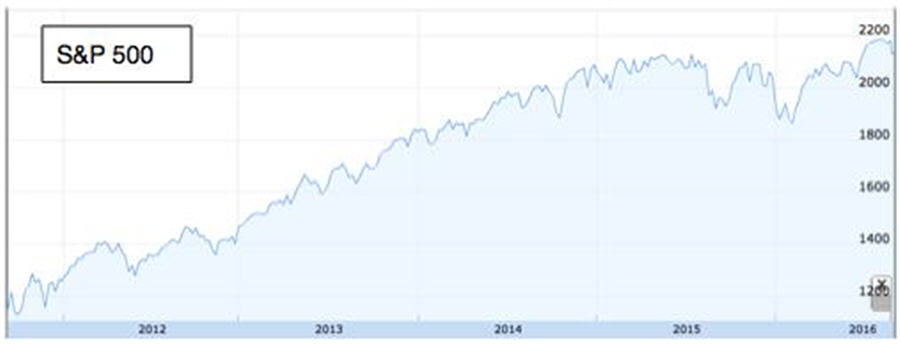

Once again this year, US GDP expectations have been downgraded. This has now been the pattern for six years running: optimistic projections at the start of the year are downgraded dramatically by the time we near the end. At this point, it looks like GDP growth in 2016 will come in at just 1%. That’s terrible.

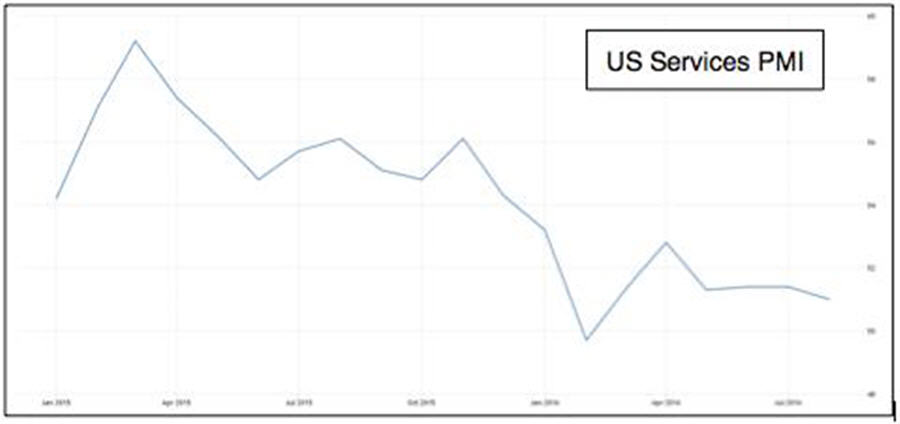

One of the yuckiest charts out there now is the Purchasing Managers’ Index (PMI) for the US services sector. Services make up 70% of the US economy so this number matters – and if that isn’t a decided downtrend I don’t know what is.

Arguments about the state of the US economy abound. Depending what data you choose, the situation can range from desperate to decent. But for such a mediocre economy to support a sky-high stock market is questionable.

The reason we are in this situation, of course, is that, as in the bond market, investors have been chasing stocks for price, cause of the lack of yield elsewhere. And enough of them are doing it that they turned the market into a gift that keeps on giving.

It will not last forever. Cracks might be starting to appear, though it is too soon to tell. Whether now or later, at some point the US markets will turn down. When that happens a rush of investors will move into gold, the classic safe haven investment in times of turmoil.

And until the markets turn, gold will perform as one of few options that make sense in a negative rate world. At the end of the day, rates are the most important force in the gold market right now. Just look at this chart comparing gold with the bond/dollar ratio (price of Treasury bills divided by the dollar index).

Thanks to The Speculative Investor blog (link here; a great free service you should sign up for if not already) for pointing out this chart, as the correlation is just so strong. It makes sense: the bond/dollar ratio incorporates interest rates, exchange rates, and inflation expectations, also known as the drivers of financial balance. Bond prices fall when interest rates rise; the dollar rises with rates but falls with inflation, while also reflecting relative valuations against other currencies.

The result: gold gained this year whenever the market decided rates were staying put, which pushed bond prices up and the dollar down.

What I see for the rest of the year is more of the same.

And as the low/negative rate world fuels gold, the yellow metal creates its own momentum. I’ve said it before and I will say it again: a rising gold price becomes a self-fulfilling prophecy. Investors know that gold moves in cycles. Once the yellow metal has proven an upward path, generalists turn towards.

Political and economic uncertainties amplify the move, but gold only starts to gain when such uncertainties abound so it’s no surprise they play a role during the rise.

The setup makes sense. Gold is still inexpensive, relative to historic levels, so it offers upside. For decades gold has held its value when artificial instruments – currencies, bonds, and stocks – have failed, so it offers security. It has a very well established pattern of rising in the face of economic and political uncertainties, which abound.

So yes: rates are the most important factor at play for gold, but the catch is that continued low rates (as I expect for the next few months) support the metal but so will a rate increase, because of the stock and bond volatility it will create.

Ridiculous

That brings us to the ridiculous part of the current obsession with rates. For gold investors, the ridiculous is that exact timing hardly matters.

The question of When matters if you are a trader. A rate hike will create significant short-term stock and bond moves, so analyzing the evidence to predict when that will happen matters to those trading stocks on a day-to-day basis.

But most of us are not day traders. Metals and mining investors are putting their money into a trend, an historically supported, data driven idea that certain mined commodities – gold, silver, zinc, and uranium to start – are in the early stages of a new up cycle.

As I just described, things are well set for that whatever happens with rates. So provided one can ignore the stress of short-term fluctuations, long positions in gold equities work.

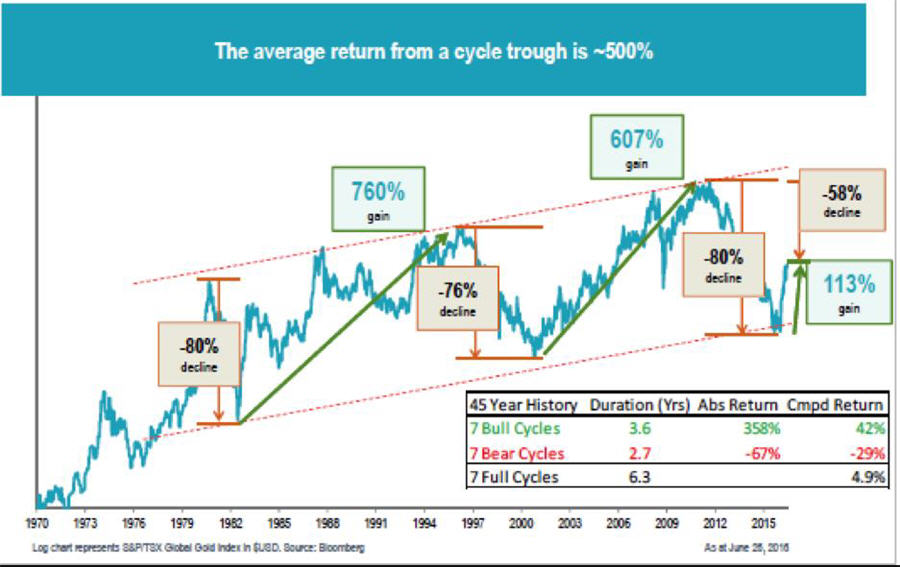

While we’re talking context, I want to include this chart. I openly acknowledge that it was published in Sprott’s Thoughts (a great read that comes out a few times a week – sign up HERE if you’re not yet on the list. I write it occasionally). It charts the S&P / TSX Global Gold Index since 1970 and shows clearly the cycles we’ve gone through.

The chart shows seven bull-bear cycles, though only the biggest three (three downs and two-and-a-bit ups) are highlighted.

Considering all seven cycles, the average decline was 67%. That means the 80% decline we endured in the last bear market was worse than usual.

More importantly: bull market gains have averaged 358% among those seven cycles. Recovering from the two cycles with the biggest losses (as highlighted on the chart) required gains of 760% and 607%.

To date in this market, the S&P / TSX Global Gold Index gained 114% to its early August peak. The August correction has cut the gain back to 84% today.

That means the gold index has to more than double from here to achieve the average gain of the seven bull markets and it would have to quadruple from here to achieve a gain comparable to the last two big cycles.

That’s a lot of long term upside.

As for the short term, I think the odds of a rate hike next week are less than 30%.

Every time the threat of a rate hike appears, the market throws a tantrum. And like the kid who keeps throwing tantrums because he gets what he wants, the market’s self-induced slides have worked to delay rate hikes because the Fed hates to throw out a disruptor when things are disrupted.

Right now the same story is playing out again, but with two added factors: a Presidential election around the corner and some poor economic data of late (remember that August jobs number?). I think this combination of factors will delay the Fed, no matter how much Yellen wants to raise rates. After all, they’ve been waiting for the right moment for years – why rush into it now?

I could be wrong (hence the 30% leeway). If Yellen hikes next week, be prepared for a week or two of volatility to the downside. If there are stocks you want to own more of, be ready to buy.

If she doesn’t hike, gold will rise (breaking its current association with US equities) and the strong fall gold season will be off to the races.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments