South Africa looks to mining industry to fuel covid-19 recovery

South Africa is banking on a rejuvenation of its flagging mining industry to help counter the economic devastation wrought by the coronavirus and a lockdown that was imposed to curb its spread.

The need to rebuild investor confidence in a sector that once formed the bedrock of Africa’s most-industrialized economy was identified as a key tenet of an economic recovery plan that was agreed by the government and business and labor representatives this week.

They undertook to jointly develop a strategy within three months to target 3% of global exploration expenditure and halve the time it currently takes to secure all mining, prospecting and environmental licenses. Fixing Eskom Holdings SOC Ltd., the debt-stricken state power company that has stifled output and investment because it can’t produce enough electricity to meet demand, and creating regulatory certainty were identified as other top priorities.

“Simplifying and modernizing mining regulation will unleash significant investment by business in exploration and production, generating substantial employment, both directly and indirectly, as well as contributions to the fiscus and foreign-exchange earnings,” according to the 13-page document seen by Bloomberg. President Cyril Ramaphosa is due to release the plan once the cabinet has signed off on it.

“The most important part of the growth plan with regards to mining will be electricity availability and policy certainty. The sector has been begging to generate its own power for a long time now, and even though there is progress, the proposed licensing arrangement and generation limits will still be constraining. With regards to policy — the goalposts keep changing. The sector will want to know that whatever the government decides will not change every five to 10 years as has been the case in the past.”

Boingotlo Gasealahwe, Africa economist, Bloomberg

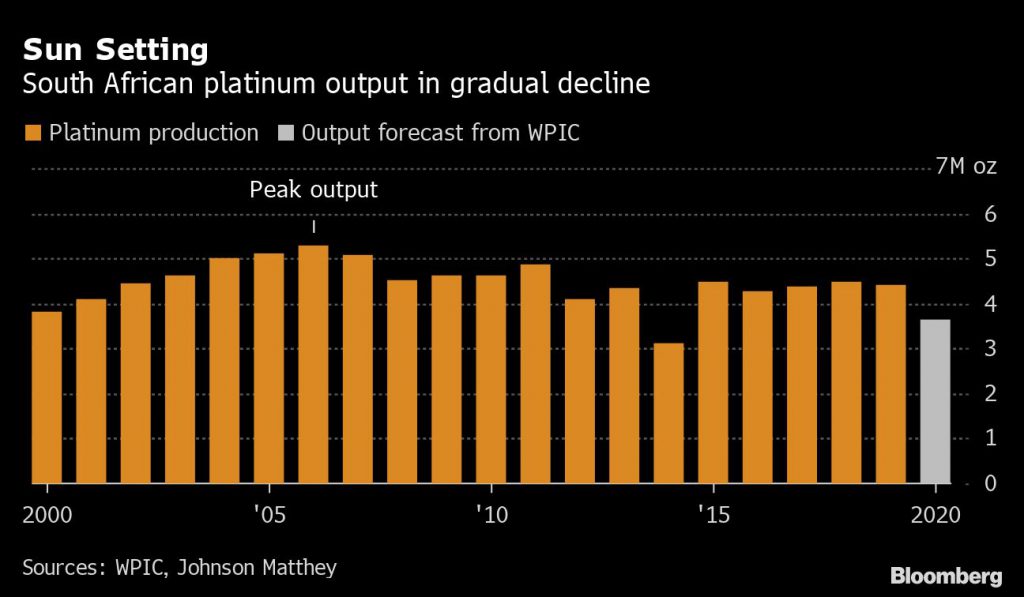

The mining industry contributed 8.1% of South Africa’s gross domestic product last year, from a peak of more than 20% in the 1980s. The drop coincided with robust demand for key metals including iron ore, platinum-group metals, gold and chrome. The industry directly employs about 450,000 people, down from 520,000 in 2012, according to the Minerals Council South Africa, a lobby group for larger producers.

The precipitous decline is most evident in the gold industry, which was once the world’s largest and now ranks eighth. Output has dwindled to less than a fifth of what it was at its peak, with deposits becoming harder to access and producers contending with power shortages and regulatory uncertainty.

Bullion producers AngloGold Ashanti Ltd. and Gold Fields Ltd. have pared back investment in South Africa to target more lucrative deposits elsewhere in Africa, Australia and Latin America. Platinum giants such as Sibanye Stillwater Ltd. and Impala Platinum Holdings Ltd. have also switched focus toward North America.

Roger Baxter, the Minerals Council’s chief executive officer, declined to comment on the plan until its official release.

The agreement reached on the plan marks a rare moment of compromise between labor unions, which are allied to the ruling party yet often bicker with it about economic policy, the government and business groups whose views have been largely discarded since the end of apartheid in 1994. Other key components include commitments to boost investment in infrastructure, reduce port bottlenecks, fight graft and cut red tape to make it easier to do business.

(By Mike Cohen, Felix Njini and Antony Sguazzin)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments