Satellite images show Tesla’s Gigafactory ambitions

Newly released satellite images of the changing Nevada landscape just outside of Reno have revealed the scale of Tesla Motors’ super battery plant, the Gigafactory.

Tesla is well under way with phase one of construction that will see the launch of a lithium-ion battery plant with a 7GWh capacity by Q1 2016.

The first phase of the plant will already see the company host the world’s biggest lithium-ion battery plant, even at 20% the size of Tesla’s ultimate plans.

The Gigafactory will cost a total of $5bn and require huge volumes of critical minerals and metals, especially graphite, lithium and cobalt. The company has already spent $62m to date, primarily on land clearance and construction of the phase one shell.

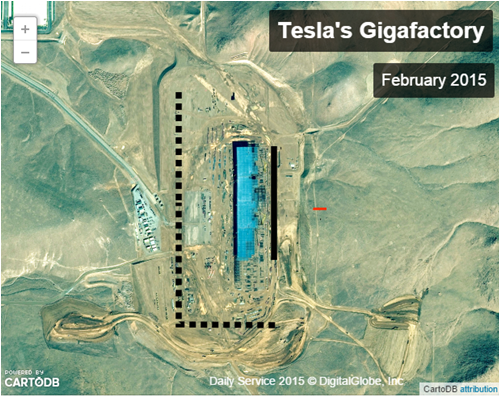

Gigafactory construction in February 2015. Source: CartoDB via Mashable

Gigafactory phase one construction v the full size plan. Source: CartoDB via Mashable

Benchmark Mineral Intelligence estimates for phase one, Tesla will need to purchase at least 7,000 tonnes of spherical graphite, 5,000 tonnes of lithium hydroxide, and 1,500 tonnes of cobalt in 2015 ready to begin production by January 2016.

The lithium industry is already seeing tighter supply owing to increased battery demand in Asia, especially for hydroxide. This is forcing prices upwards with some quoted prices 20% higher than in 2014.

The fact that lithium hydroxide cannot be stored for long periods of time leaves a race for fresh supply as and when it comes on the market. Battery producers will no doubt also be braced for the increased competition for raw materials that the Gigafactory will bring.

At present the only supply of battery grade graphite and 60% of cobalt refining capacity lies within China, which is also escalating its battery production capacities.

It is a perfect example of how the change in end markets, especially in the hi-tech space, is far outpacing supply side developments.

While the Gigafactory is an extreme disruptive example, under investment in critical mineral supply capacity over the last 20 years has left these niche industries inflexible and ill equipped to handle any reasonable change to the system.

It is likely key players will soon have to work with new suppliers of raw materials such as the junior exploration sector to satisfy its longer term demand requirements, certainly if they do not want to rely on China for the bulk of their raw materials – something Tesla ruled out last year.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments