Sanctions fever grips nickel as market rethinks Russia risk — Andy Home

By Andy Home, columnist for Reuters

Sanctions fever has spread to nickel.

With Russian aluminium producer Rusal imploding in the wake of U.S. sanctions against its oligarch owner Oleg Deripaska, attention is now turning to the status of another Russian industrial powerhouse, Norilsk Nickel.

Deripaska is a 27.8 percent shareholder in Norilsk, while the oligarch behind the world’s number two nickel producer, Vladimir Potanin, is himself on a U.S. Treasury Department list of Russians deemed to be close to the Kremlin.

Fears that Norilsk might follow Rusal down the U.S. sanctions path have sent London nickel prices on an extraordinary rollercoaster ride.

But this was a market primed for an explosive breakout, with all sorts of technical drivers kicking in once it started rallying.

Right now there is no imminent danger of Norilsk being pulled into the Rusal sanctions and the speculative froth is already blowing off an overheated market.

But nickel’s shake, rattle and roll is a sign of changing times.

Industrial metal markets have spent the past decade tracking the shifting policies of just one country, China.

The eruption of U.S. policy risk and global geopolitical risk injects something completely new and different into market calculations.

As nickel shows, pricing this changed landscape is still very much a chaotic work in progress.

COLLATERAL DAMAGE

There is no compelling evidence that the U.S. sanctions on Deripaska and his aluminium empire are going to affect Norilsk.

Deripaska’s stake is below the 50 percent threshold over which sanctions can leap from targeted entity to secondary entity.

It is also worth remembering that Deripaska’s relations with Potanin are distinctly frosty. The two oligarchs have been locked in an acrimonious stand-off ever since Deripaska scooped up his holding in Norilsk during the global financial crisis.

And while Potanin does appear on the Treasury’s “Putin List”, released in January this year, so do 209 other Russians.

Only seven were designated in the April 6 sanctions and the U.S. government has signalled it is not planning any imminent new sanctions.

Norilsk is also a different beast from Rusal. As well as looming large in global nickel production terms, it is also big supplier of copper and cobalt.

Most importantly, however, it is the world’s No.1 supplier of palladium to automotive manufacturers who use the metal in catalytic converters.

That includes U.S. auto companies. North American and Latin American customers accounted for $807 million, or 34 percent, of Norilsk’s palladium sales in 2016.

Hitting Norilsk with the sort of draconian sanctions unleashed on Rusal risks massive collateral damage. The United States has only one major palladium mine, Stillwater in Montana, which would be unable to full any sanctions-induced supply gap.

The Rusal sanctions, by contrast, dovetail with the U.S. administration’s aluminium tariffs, aimed at encouraging the restart of idled production capacity.

A PRIMED MARKET

Such details have been lost in the speculative heat of the past couple of days.

Fanning the flames further were rumours that the London Metal Exchange (LME) was delisting Norilsk brands.

However, unlike the emergency suspension of Rusal brands, this is old news, originally announced in August 2016.

The brands are being removed because Norilsk has decommissioned the plant that produced them. Most of the Russian metal in LME warehouses has long since set sail for China.

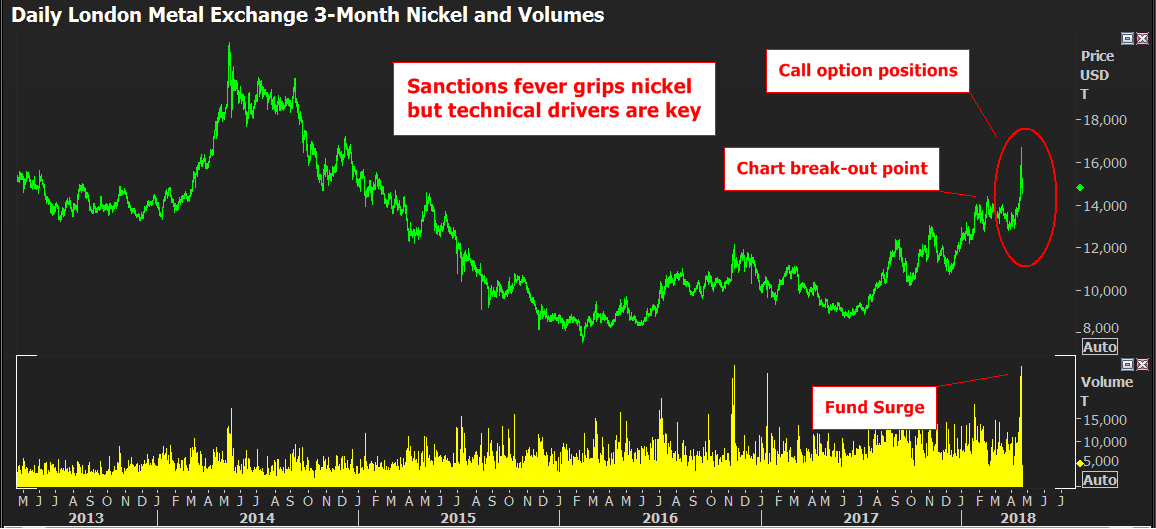

None of which seemed to matter as the LME nickel price exploded to a three-year high of $16,690 a tonne on Thursday, registering its widest intraday range since 2011 in the process.

This, though, was a market primed for a bull breakout. Sanctions fever just gave it the impetus to do so.

On the back of production cuts from Brazil’s Vale , the world’s largest producer, exchange stocks have been sliding and LME nickel this week started to nudge up against the February high of $14,420, a red-flag target for technical players.

Unsurprisingly, when that level was breached on Wednesday, speculative buyers surged into the market, evidenced by massive volumes.

So too did Chinese speculators. Volumes on the Shanghai Future Exchange’s (ShFE) nickel contract hit a record 2.693 million contracts on Thursday.

ShFE moved quickly to douse the fires with an increase to the intraday margin, a tried and tested way of dispersing the speculative crowds, Chinese style.

Meanwhile, exacerbating the ferocity of the move on the London market was hedging against shorts in the options market.

The wild rally sent the nickel price crashing through layers of call option positions. These confer the right to buy, which is nice for the buyer in such a fast-moving rally but a major hedging headache for the seller.

Some 50,000 tonnes of call option positions, spread across the front three months and concentrated on the $15,000 strike, were put into play in the space of 24 hours. Those short of the options were forced to buy the underlying nickel contract, adding to the frenzy.

And they were forced to sell it all back when the market went into sharp reverse yesterday afternoon.

Nickel has this morning touched a low of $14,530, close to where it started the week.

The speculative bubble has burst as the market realises that Norilsk is in the clear for now.

EXPANDED RISK HORIZONS

The emphasis, howevber, is on those last two words.

While Norilsk’s Potanin isn’t facing imminent sanctions, it is no longer inconceivable that he won’t at some stage if U.S.-Russian relations deteriorate further.

This is the true psychological shock of the sanctions against Rusal.

No one saw them coming because no one could conceive of such a large international supplier of aluminium being locked out of the U.S. dollar system.

And now we all can, as each day bring fresh news of Rusal’s own collapsing supply chain.

For at least a decade industrial metal markets have only bothered tracking one country’s policy.

China has so dominated the landscape that the markets have increasingly focused almost exclusively on policymaking in Beijing with the prism set to pick up shifts in economic, industrial and, increasingly, environmental thinking.

U.S. sanctions on Russia require an expansion of risk horizons and, quite possibly, a repricing of Russian risk on certain specific commodities. Such as nickel.

This week’s wild gyrations suggest the process has only just started.

(Editing by David Goodman |The opinions expressed here are those of the author.)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments