The real cash cow in mining isn’t metals. It’s bad old coal

For all the bullish talk about metals of the future, miners are making some of their biggest profits from heavy-industry stalwart coal.

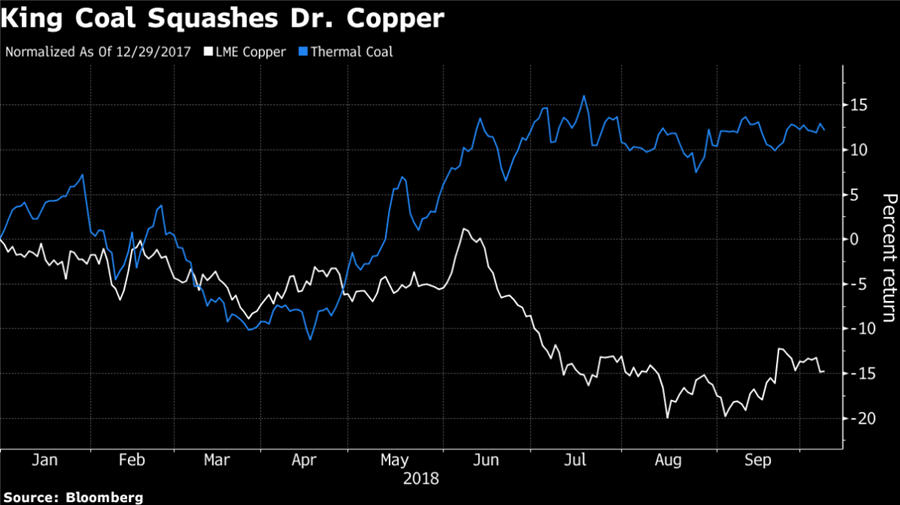

Base metals from copper to zinc have tumbled this year, caught up as a proxy for trade fears and emerging market jitters. Meanwhile, coal has ground steadily upwards, supported by strong demand from top commodities user China, and is trading near the highest in more than six years.

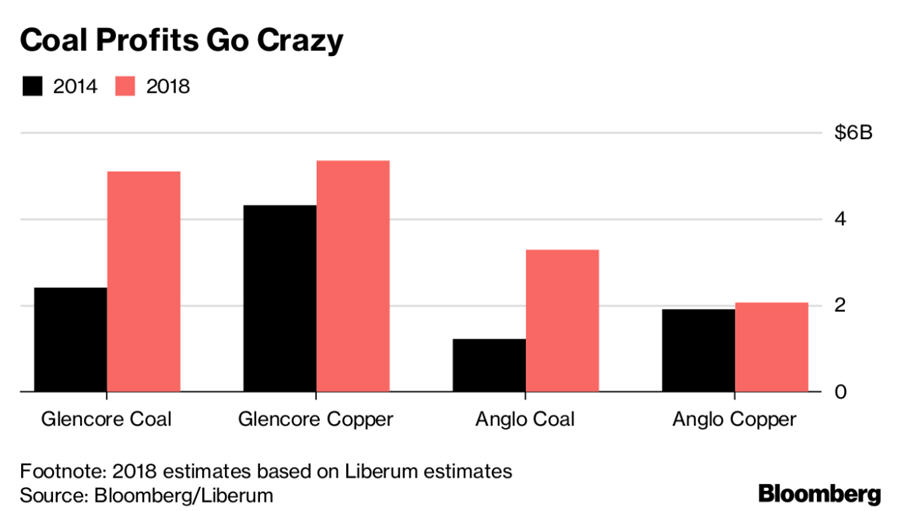

That’s translating into big paydays for producers. Anglo American Plc’s coal earnings almost trebled in the last four years, despite lower production. The fuel is forecast to contribute a whopping 43 percent of Anglo’s profits this year despite it operating some of the best platinum, diamond and copper mines in the world.

Glencore Plc is in touching distance of seeing its coal mining profits eclipse copper earnings this year for the first time since it sold shares in London in 2011.

“This is the sweet spot for the coal miners,” said Ben Davis, an analyst at Liberum Capital Markets. “Chinese coal demand is through the roof and that’s because domestically they’re not producing enough. China is importing more coal than it ever has done before.”

It wasn’t supposed to be this way. Almost everyone in metals is universally bullish on copper, from the CEOs of the biggest mining companies to investors and analysts, all expecting increased demand from the electrification of cities and cars and constrained supply. Coal, on the other hand, has been widely shunned by both investors and many producers.

One explanation is that coal is susceptible to strong price swings. Unlike most other commodities, the vast majority of the fuel is produced in the country it’s burned, near power stations. The global seaborne market of about 1 billion tons is less than a fifth of total production, meaning small swings in demand can have a disproportionate impact on price.

Seaborne coal demand increased more than 9 percent in the first half, while supply rose by less than 8 percent, according to Glencore. Chinese coal power generation increased by 7.8 percent, the world’s biggest coal producer said.

While a disconnect between bulk materials and base metals isn’t uncommon, commodities like coal and iron ore tend to be more closely aligned to supply and demand fundamentals than investor sentiment, the pattern is holding for longer than usual.

“We have seen such disconnects before, however they have tended to last only a few weeks,” BMO Capital Markets said. “The current example has lasted several months, and every time it looks as though the macro headwinds have blown themselves out, they return once more.”

(By Thomas Biesheuvel)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments