Oreninc Index – Monday, June 19, 2017

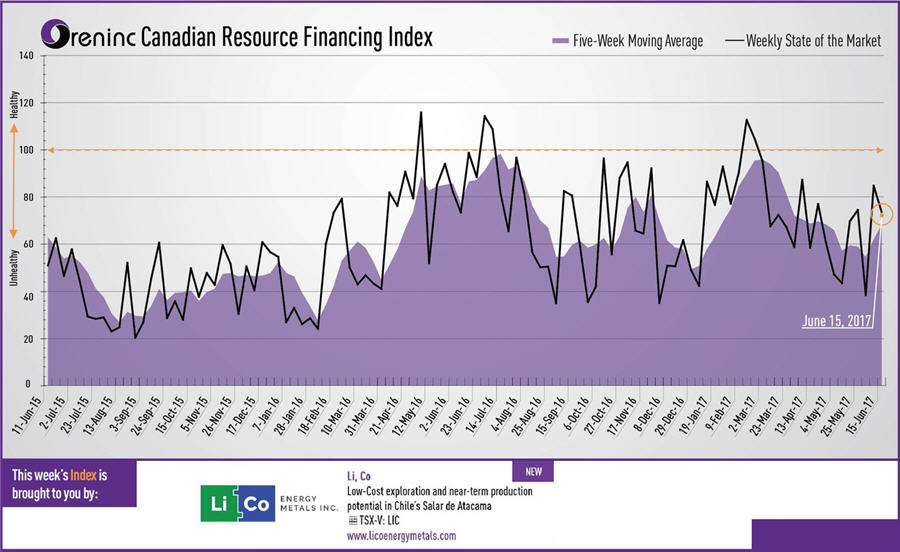

Last week index score: 84.81 (Updated)

This week: 73.66

Castle Silver Resources (TSXV: CSR) reported that chip sampling returned 1.8% cobalt, 8.6% nickel and 25.2g/t silver at its Castle mine in Ontario, Canada.

The Oreninc Index fell in the week ending June 16th, 2017 to 73.66 from an updated 84.81 the previous week.

Total raises announced fell to C$139.5 million, a two-week low, which included six brokered financings for a total of C$91.5 million, a 13-week high, within which there were two bought-deal financings for C$60.0 million, a 13-week high. The average offer size fell slightly to C$4.0 million, a two-week low, whilst the total number of financings announced decreased to 35, a two-week low.

It was a week of turbulence for many gold stocks with the VanEck Vectors Junior Gold Miners ETF (GDXJ) rebalance finally happening on Friday June 16th. The rebalance was necessary as the success of the ETF meant that it was approaching 20% significant shareholder status in many companies. To continue to grow, therefore, it will now buy gold miners in the C$75-million to C$2.9-billion market cap, up from C$75-million to C$1.6-billion. As a result, smaller names in the index have been sold off, creating market turbulence.

Gold began the week strongly, hitting a peak of US$1,275 per ounce on Wednesday before falling off to close the week at US$1,256 per ounce, down from the previous week’s US$1,271 per ounce close, as the US Federal Reserve raised interest rates again from 1% to 1.25% and indicated that rate increases could continue. This was the third consecutive quarterly increase in interest rates and came as US jobs growth continued, pushing the unemployment rate down to its lowest level in 16 years. The Fed also said it plans to reduce bond holdings to unwind the huge economic stimulus plan brought in after the great recession.

With the rebalance taking place the van Eck managed GDXJ improved slightly to now be up 4.6% so far in 2017. The inventory of the SPDR GLD ETF pulled back to close at 854 tonnes, from 867 tonnes the previous week.

In other commodities, silver followed gold’s trajectory but with a harder fall to close down on the week at US$16.67. Copper also had a tough week to close at US$2.58 per pound from US$2.64 per pound the previous week. Oil continued to weaken with WTI crude falling to US$44.70 per barrel from US$45.83 per barrel last week.

The Dow Jones Industrial Average continues to climb to close up at 21,383 whilst Canada’s S&P/TSX Composite Index fell to 15,160. The S&P/TSX Venture Composite Index continued to fall to close at 775.91.

Summary:

• Number of financings decreased to 35, a two-week low.

• Six brokered financings were announced for $91.5m, a 13-week high.

• Two bought-deal financing were announced for $60.0m, a 13-week high.

• Total dollars dropped to $139.5m, a two-week low.

• Average offer size slipped to $4.0m, a two-week low.

Financial news highlights

Nemaska Lithium (TSX:NMX) announced C$50 million bought deal financing to fund ongoing development of its Whabouchi lithium mine and spodumene concentrator and the Shawinigan hydrometallurgical plant.

• Nemaska aims to become a lithium hydroxide and lithium carbonate supplier to the emerging lithium battery market

• Spodumene concentrate that will produced at the Whabouchi mine will be shipped to its lithium compounds processing plant to be completed in Shawinigan, Québec from H218.

Cordoba Minerals (TSX-V: CDB) announced a C$10 million bought deal financing to provide funds to continue exploration of its San Matias copper-gold project in Colombia.

• The financing comes as the company converted its joint venture agreement with Robert Friedland’s High Power Exploration company into direct ownership in Cordoba Minerals.

Fiore Exploration (TSXV: F) announced a C$17 million private placement financing as part of a business combination with GRP Minerals.

• The net proceeds will be used for expansion of the leach pads at the Pan mine on the Battle Mountain-Eureka trend in Nevada, drilling at both Pan and Gold Rock in Nevada.

• Fiore was founded by Frank Giustra and Lithium X founder Brian Paes-Braga

• It also has a strategic land position surrounding Yamana’s El Peñon mine complex in Chile

Major Financing Openings:

• Nemaska Lithium (TSX-V:NMX) opened a C$50 million offering underwritten by a syndicate led by National Bank Financial on a bought deal basis. The deal is expected to close on or about June 29th.

• Fiore Exploration (TSX-V:F) opened a C$17 million offering underwritten by a syndicate led by GMP Securities on a best efforts basis.

• Orca Gold (TSX-V:ORG) opened a C$15 million offering on a best efforts basis. Each unit includes half a warrant that expires in 12 months.

• BonTerra Resources (TSX-V:BTR) opened a C$12.91 million offering underwritten by a syndicate led by Sprott Capital Partners on a best efforts basis. The deal is expected to close on or about June 29th.

Major Financing Closings:

• Candelaria Mining (TSX-V:CXX) closed a C$9.77 million offering on a strategic deal basis.

• White Gold (TSX-V:WGO) closed a C$8.76 million offering on a strategic deal basis.

• Jaguar Mining (TSX:JAG) closed a C$7.75 million offering on a best efforts basis.

• Skeena Resources (TSX-V:SKE) closed a C$5.68 million offering underwritten by a syndicate led by RBC Capital Markets on a best efforts basis.

Company news

Castle Silver Resources (TSXV: CSR) reported that chip sampling returned 1.8% cobalt, 8.6% nickel and 25.2g/t silver at its Castle mine in Ontario, Canada.

• Previous mine operators only assayed for silver

• Underground sampling covering multiple target areas continues

Conclusion

Sampling is the first step to determining the cobalt, nickel and silver potential at high-grade Castle silver mine, and developing targets for a future drilling program as the company aims to become a player in the cobalt space.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments