Nickel: The secret driver of the battery revolution

Nickel: The Secret Driver of the Battery Revolution

Commodity markets are being turned upside down by the EV revolution.

But while lithium and cobalt deservedly get a lot of the press, there is another metal that will also be changed forever by increasing penetration rates of EVs in the automobile market: nickel.

Today’s infographic comes to us from North American Nickel and it dives into nickel’s rapidly increasing role in lithium-ion battery chemistries, as well as interesting developments on the supply end of the spectrum.

NICKEL’S VITAL ROLE

Nickel’s role in lithium-ion batteries may still be underappreciated for now, but certainly one person familiar with the situation has been vocal about the metal’s importance.

Our cells should be called Nickel-Graphite, because primarily the cathode is nickel and the anode side is graphite with silicon oxide.

– Elon Musk, Tesla CEO and co-founder

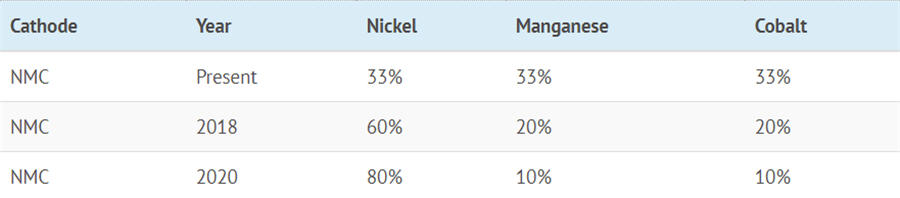

Indeed, nickel is the most important metal by mass in the lithium-ion battery cathodes used by EV manufacturers – it makes up about 80% of an NCA cathode, and about one-third of NMC or LMO-NMC cathodes. More importantly, as battery formulations evolve, it’s expected that we’ll use more nickel, not less.

According to UBS, in their recent report on tearing down a Chevy Bolt, here is how NMC cathodes are expected to evolve:

The end result? In time, nickel will make up 80% of the mass in both NCA and NMC cathodes, used by companies like Tesla and Chevrolet.

IMPACT ON THE NICKEL MARKET

Nickel, which is primarily used for the production of stainless steel, is already one of the world’s most important metal markets at over $20 billion in size. For this reason, how much the nickel market is affected by battery demand depends largely on EV penetration.

EVs currently constitute about 1% of auto demand – this translates to 70,000 tonnes of nickel demand, about 3% of the total market. However, as EV penetration goes up, nickel demand increases rapidly as well.

A shift of just 10% of the global car fleet to EVs would create demand for 400,000 tonnes of nickel, in a 2 million tonne market. Glencore sees nickel shortage as EV demand burgeons.

– Ivan Glasenberg, Glencore CEO

THE SUPPLY KICKER

Even though much more nickel will be needed for lithium-ion batteries, there is an interesting wrinkle in that equation: most nickel in the global supply chain is not actually suited for battery production.

Today’s nickel supply comes from two very different types of deposits:

- Nickel Laterites: Low grade, bulk-tonnage deposits that make up 62.4% of current production.

- Nickel Sulfides: Higher grade, but rarer deposits that make up 37.5% of current production.

Many laterite deposits are used to produce nickel pig iron and ferronickel, which are cheap inputs to make Chinese stainless steel. Meanwhile, nickel sulfide deposits are used to make nickel metal as well as nickel sulfate. The latter salt, nickel sulfate, is what’s used primarily for electroplating and lithium-ion cathode material, and less than 10% of nickel supply is in sulfate form.

Not surprisingly, major mining companies see this as an opportunity. In August 2017, mining giant BHP Billiton announced it would invest $43.2 million to build the world’s biggest nickel sulfate plant in Australia.

But even investments like this may not be enough to capture rising demand for nickel sulfate.

Although the capacity to produce nickel sulfate is expanding rapidly, we cannot yet identify enough nickel sulfate capacity to feed the projected battery forecasts.

– Wood Mackenzie

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments