New NewCastle Gold CEO Gerald Panneton hits the ground running

Mining entrepreneur Gerald Panneton took a few years off after building one of Canada’s largest gold miners, Detour Gold.

Gerald Panneton (Newcastle Gold photo)

He raced performance cars in his downtime, and conducted due diligence on various mining assets to potentially back.

This summer, the geologist set his sights on NewCastle Gold(TSXV:NCA), owner of a past-producing gold mine in California with similarities to Detour Gold in its early days.

Panneton interviewed for the top spot at Newcastle on July 28. A few days later, he was badly injured in a car race in Toronto. Panneton was rear-ended by another racer and slammed into a wall at speeds over 100 km/hour, suffering a broken rib cage and perforated lung.

It was the first crash for the 58-year-old geologist turned racer, who was raised in Trois-Rivières, Quebec and now lives in Toronto. In an introductory call withCEO.CA last week, Panneton said he enjoys being under pressure and taking calculated risks.

Gerald Panneton with his Porsche GT3 RS on the track at Mosport. (FRED THORNHILL for The Globe and Mail)

Panneton is back in good health and about to begin his first marketing roadshow for Newcastle. He’s planning to spend the bulk of September communicating the Newcastle story to investors and analysts.

In NewCastle’s Castle Mountain gold project, Panneton sees a large-scale, brown field, largely permitted resource in a leading jurisdiction that’s amenable to simple heap-leach mining, and can be brought back into production in the near term.

Castle Mountain is located 90 km SW of Las Vegas and benefits from year-round access and good infrastructure. It was brought into production in 1992 at a cost of $50 million and reached an annual production high of 168,190 ounces in 1995. The mine was shuttered in 2001 due to low gold prices after producing some 1.2 million ounces of gold. It still has a valid Mining and Reclamation plan through 2025, meaning it is largely permitted.

Panneton sees major exploration upside at NewCastle’s already significant 4.2-million-ounce Measured and Indicated gold resource.

“I just went through the exercise of going through all the cross sections and long sections in both directions and this project has a very good geological model. It’s well understood now. We can predict where we will hit in new drilling. We know it’s open in most directions. I think the property has great potential to get bigger. At the same time, it can go into production with a relatively smaller effort than starting a new project from scratch.”

Newcastle is in the midst of a 22,000-meter drill program at Castle Mountain to expand and upgrade the resource, and additional assay results are pending. The company is also focused on geotechnical work that could improve the strip ratio. NewCastle plans further drilling, mining studies and permit applications in 2017.

“What’s going to excite the market is to put back the project in production in the near future once we have done more drilling to increase the resource base to make the project bigger,” Panneton says. “At the end of the day that’s what the shareholders want, adding value to the project and becoming a gold producer again.”

As founder and former CEO of Detour Gold, Panneton helped grow the Detour Lake project through the drill bit from a 1.7-million ounce resource to a reserve of over 16 million ounces of gold. He raised over $2.5 billion to build the mine. Now in production, Detour is expected to haul 540,000-570,000 ounces of gold in 2016 at competitive costs, making it one of Canada’s most significant producers.

“It was very sad when the board asked me to leave,” Panneton says of his 2013 departure from Detour Gold. At the time, gold had fallen from a high of $1,700 down to $1,150. The team and strategy Panneton put in place at Detour stayed and has since been validated by strong production results. Detour’s share price was $3.50 at IPO and its market cap was $140 million. Today, it’s a $31.50 stock with a market cap over $5 billion.

Panneton says NewCastle’s Castle Mountain project may not be as big as Detour, both in terms of resource size and annual production. However, it should be far cheaper to get back into production, though he was shy to put a ballpark estimate on CAPEX until further work is done. Panneton sees a potential 150,000-200,000 ounce per year producer with a multi-decade mine life. The mine could be a cornerstone asset for a mid-tier producer.

“The bonus of this project we can get it bigger within the permitted area, but what lies ahead for potential area or further expansion will require time, permitting and more drilling. The idea is to start where we have permits, make sure we don’t sterilize other areas of the property, and do more drilling for expansion eventually. If we show that we are good miners that care about the environment and work well with the county of San Bernadino, we should have no problems.”

NewCastle has a roughly $170-million market cap, based on a recent $1.08 share price and about 158 million shares outstanding. The company had $6.5 million in cash according to a July 2016 corporate presentation, meaning NewCastle will likely finance soon.

“Money always comes to the projects that are well-managed and well-presented”, Panneton says. “My job is to have a very good representation with shareholders and make sure they understand the story, the growth capacity, and the fact the valuation currently is very low.”

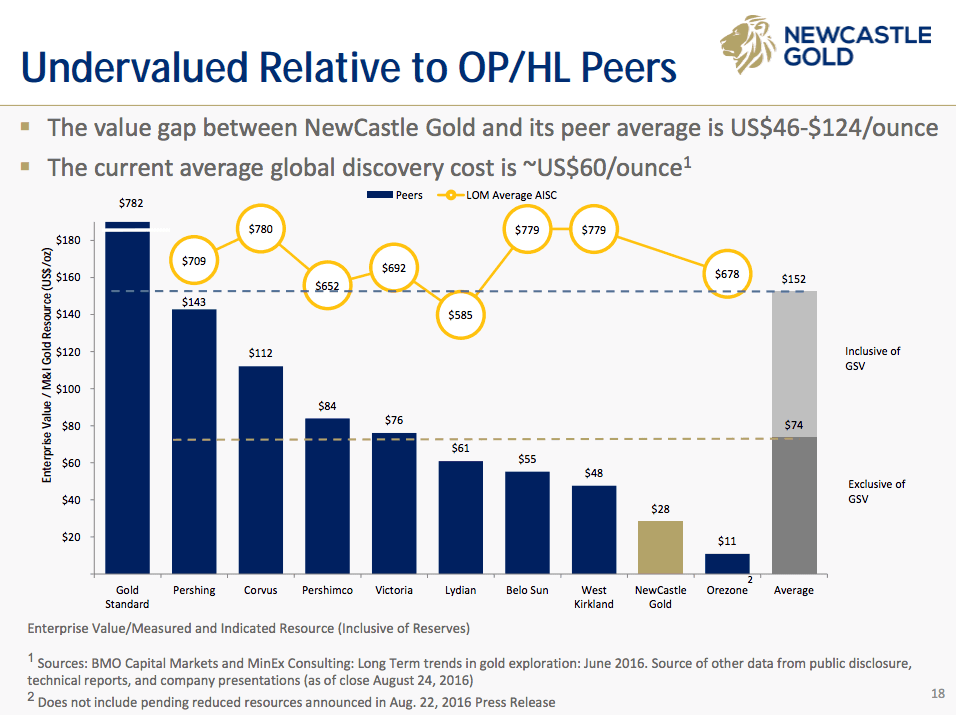

He’s referring to NewCastle’s value relative to its peer group on an enterprise value to M&I gold ounces basis:

Panneton plans to stick with NewCastle at least until it reaches production.

“You will not see me as President and CEO sitting on other boards. I have only one focus and it’s NewCastle Gold.”

He joins a company with an impressive board of directors, including Jim Gowans, Arizona Mining CEO and former co-President at Barrick Gold, and Frank Giustra, founder of Fiore Financial.

NewCastle Executive Chairman Richard Warke has an exceptional track record in mining. He founded Ventana Gold and Augusta Resource in 2006. Ventana was taken out in 2011 for $1.5 billion. Augusta was taken out in 2014 for $666 million. Mr. Warke has acquired more than 2 million Newcastle shares in the open market this summer.

Daniel Earle, mining analyst with TD Securities, has a SPEC BUY rating and C$2.00 price target on NewCastle, citing potential for rapid resource growth.

“People want to know why does Gerald Panneton take on NewCastle Gold? There’s a very good reason,” the new CEO of NewCastle said. “I believe I can make investors money again.”

Do your own due diligence on NewCastle Gold and discuss your suitability with a licensed investment advisor. It’s your money and your responsibility. Author is long NCA.V at the time of writing. This is not investment advice or an offer or suggestion to trade securities of any kind.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments