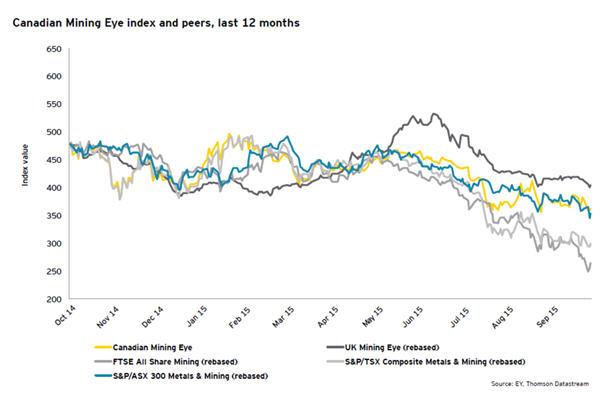

Market uncertainty pulls Canadian Mining Eye index down in Q3

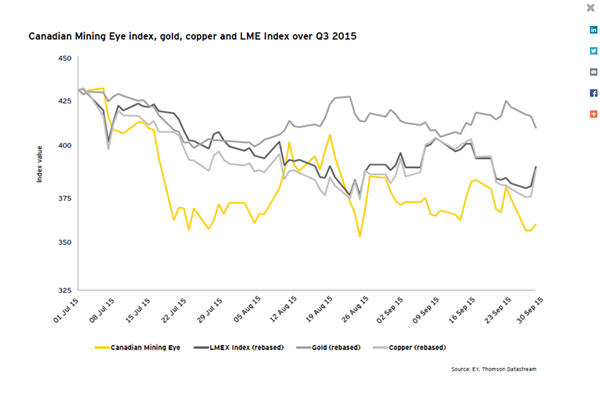

The slide in base metals continued in Q3 2015 as a result of an economic slowdown and a decline in the manufacturing activities in China. In response to China’s slowing demand and concerns over metal financing inventories, copper tumbled 10% during the quarter on the London Metal Exchange (LME), the largest drop since 1Q 2014. Nickel and Lead were down 13% and 5% respectively on the LME over Q3 2015, while Zinc slipped 16%. In the face of lower prices, some companies suspended operations and focused on cost cutting. Glencore, the world’s largest miner and trader of zinc, suspended its zinc mine production in Australia and Peru, while also reducing production across its various operations.

Mergers and acquisitions

Momentum in M&A increased significantly in Q3 2015 as a result of several high-value M&A and financing deals. A number of companies accessed financing through asset disposals, equity or stream financing arrangements, as evident in such cases as Barrick, North American Palladium and New Gold. In contrast to earlier quarters, there were many high value deals announced.

Barrick Gold announced that it entered into an agreement to sell its 50% stake in its Chile-based Zaldivar copper mine to Antofagasta on July 30, 2015, for a total consideration of US$1,005 million in cash, which consists of US$980 million upon closing, and five annual payments of US$5 million per year starting in 2016. Under the transaction, Antofagasta will take over as operator of the mine and a JV will be formed with equal representation of Barrick and Antofagasta on its board. Zaldivar produced 222 million lbs at cash cost of US$1.79/lb and EBITDA of US$260 million in 2014. The mine carries a P&P reserve of 5.56bn lbs copper at an estimated life of approximately 14 years with additional upside potential through exploration, so it appears Antofagasta is taking a longer term view. Production guidance of 230-250 lbs in 2015 at a current spot price of US$2.42/lb implies an EV/EBITDA multiple of 13.3x for the deal. The transaction is expected to close in late 2015. This transaction took Barrick to c.60% (~US$1.85 billion) of its net debt reduction target of US$3.0 billion for 2015, including disposals of Cowal (US$550 million) and Porgera (US$298 million) earlier in the year. Also, it added a partner with wide experience in Chile. After this deal announcement, Barrick entered in a US$610 million gold and silver streaming agreement with Royal Gold on August 05, 2015, for production linked to Barrick’s 60% interest in the Pueblo Vjejo mine. Following its efforts to reduce debt, Barrick announced on October 14, 2015 that it would purchase its US$850 million outstanding loan notes. 1, 2, 3, 4

OceanaGold announced acquisition of Romarco Minerals for a total consideration of CDN$856 million on July 30, 2015. OceanaGold offered 0.241 shares for each Romarco Minerals share with a consideration of CDN$0.68 per share, representing a premium of 72.7% on the closing price as of July 29, 2015. The offer price represented a premium of 71.8% to the 30-day volume-weighted average price (VWAP) of each company’s respective shares. After the completion of the transaction, existing OceanaGold and Romarco shareholders will own approximately 51% and 49% respectively of the combined entity. This combined entity will be a low-cost intermediate gold producer, diversified across New Zealand, Philippines and USA, and producing over 540kozpa starting in 2017, with a top quartile AISC of <US$600/oz. Romarco’s principal asset, Haile, is a US$331 million open cut mine, which is expected to commence production in Q4 2016 at AISC of just US$414/oz in its first year of operation. Analysts expect the Romarco acquisition to be dilutive at present, but will become EPS accretive in 2017-18, once Haile commences production. The transaction closed on October 1, 2015.5, 6

New Gold sold its 30% interest in Chile-based El Morro to Gold Corp for US$90 million in cash and a 4% royalty stream on gold production from El Morro on August 27, 2015. As part of the deal, New Gold’s US$93 million project loan will be cancelled. Under the streaming agreement, New Gold will have an option to buy El Morro’s 4% gold production at US$400/oz up to 217koz with 1% per year increase after the first 217koz. In July 2015, New Gold entered into a US$175 million streaming arrangement with Royal Gold to develop the Rainy River project. Analysts expect that these two deals and the existing cash balance of US$327 million should negate any additional financing requirements for New Gold in the near future. Following the acquisition, Gold Corp became the 100% owner of the project and announced a 50:50 JV with Teck Resources, combining El Morro and Relincho projects in Chile. El Morro has P&P reserves of 8.9moz, with low grades, high capex requirement and substantial permitting issues. As such, it is not beneficial to New Gold or Gold Corp’s model independently, but significant synergies can be realized by combining with Teck’s Relincho project. The transaction is expected to close in the fourth quarter of 2015.7, 8

Endeavour Mining announced a strategic partnership with La Mancha on September 21, 2015. Under the agreement, La Mancha offered its (i) 55% interest in Société des Mines (SMI), (ii) US$63 million cash (including US$25 million cash held in SMI) and (iii) commitment to invest up to US$75 million in additional funds. In return, La Mancha will be issued 177.1 million shares, representing 30% interest in Endeavour Mining, which involves a two-year equity lock-up. This deal will increase Endeavour’s gold production rate to 580kozpa, grow its P&P reserves by 23% to 8.5moz gold and reduce net debt by c.US$80 million to US$159 million. Deal proceeds will be used to fully fund the next phase of development of the Hounde project based in Burkina Faso.9

Fund-raising

Pretium Resources closed a construction financing package of US$540 million with the Orion Mine Finance and Blackstone Tactical Opportunities on September 21, 2015. The financing package comprises of (i) a senior secured credit facility and offtake of US$350 million at 7.5% interest rate, maturing December 2018, (ii) an 8% callable streaming agreement of US$150 million on 7.1moz gold and 26.3moz silver production, and (iii) a private placement of US$40 million of 3.85 million common shares at US$5.1975 per share. The company will use proceeds of the financing package to fund approximately 70% of estimated US$747 million capex requirement to develop a mine at its Brucejack project, where construction is expected to commence immediately with production targeted for 2017. Analysts expect Pretium to generate sufficient free cash flows in 2018-19 to pay the credit facility in 2019, though they remain skeptical of its ability to buy back 100% of the streaming agreement.10, 11

Alacer Gold signed its previously announced a US$250 million senior secured project finance facility with BNP Paribas, ING Bank and Société Génerale on September 21, 2015. The facility has a seven-year maturity at LIBOR plus 2.50%-2.95% interest rate, without any mandatory gold hedging requirements or early repayment penalties. The proceeds will be used to de-risk and advance growth of Copler Sulfide project.12

Western Potash closed its previously announced private placement of 240.4 million common shares at CDN$0.34 per share on September 16, 2015, raising gross proceeds of CDN$80.7 million. Under the transaction, Beijing Tairui Innovation Capital and CBC subscribed 238.2 million and 2.1 million shares and subsequently gained 51.0% and 10.1% ownership in Western Potash respectively. The proceeds will be used to develop company’s Pilot plant on the Milestone project.13

North American Palladium closed its previously announced rights offering of 8.4 million common shares, raising gross proceeds of approximately CDN$50 million on September 15, 2015. Pursuant to subscription privilege, approximately 7.7 million shares were subscribed by Brookfield and 0.4 million by Polar. The proceeds of the rights offering will be used to repay the amounts owed under the bridge loan facility with Brookfield and ongoing operations at its flagship LDI Mine. Earlier in the year, North American Palladium underwent a restructuring including workforce reduction and management changes.14

Imperial Metals closed its previously announced financing package of CDN$80 million on August 24, 2015, which included (i) rights offering of 5.5 million common shares at CDN$8.0/share, raising gross proceeds of CDN$44 million, (ii) private placement of 0.7 million common shares at CDN$8.4/share, raising gross proceeds of CDN$6 million and (iii) private placement of convertible debentures, bearing 6.0% p.a. interest rate, maturing August 2021, raising gross proceeds of CDN$30 million. The proceeds will be used to repay CDN$30 million line of credit from Edco Capital to fund the production ramp-up of the Red Chris mine, and to restart operations at the Mount Polley mine.15

Kennady Diamonds closed the final tranche of its previously announced private placement of 15.4 million common shares and 1.7 million flow-through common shares, raising gross proceeds of CDN$48.1 million, on October 08, 2015. The proceeds will be used to fund all aspects of Kennady North Project until the end of 2017, significantly de-risking to the company’s balance sheet.16

Looking ahead to upcoming quarters

In September 2015, Glencore updated its plans to reduce its net debt (US$29.6 billion) by up to US$10.2 billion, which will involve raising approximately US$2.0 billion from precious metal streaming transaction and asset sales. Proposed asset sales include a minority stake disposal in certain agriculture and infrastructure assets in Australia and Canada, in which Japanese, Chinese and Middle Eastern sovereign wealth funds showed immediate interest. Continuing with the asset sales efforts, the company also announced that it would seek a buyer for its Cobar copper mine in Australia (production of 50ktpa copper) and Lomas Bayas copper mine in Chile (production of 75ktpa copper cathode) in October.17, 18, 19

Following its plans to reduce debt by US$3.0 billion by the end of 2015, Barrick Gold has already sold three assets (100% stake in Cowal, 50% stake in Porgera and 50% stake in Zaldivar) for an aggregate of US$1.85 billion this year and launched a process to sell another six assets in October 2015 including: Bald Mountain (P&P reserves of 1.36moz gold), 50% stake in Round Mountain (P&P reserves of 690koz gold), Golden Sunlight (P&P reserves of 127koz gold), Ruby Hill (P&P reserves of 24koz gold), Spring Valley and Hilltop.20

In September 2015, Moody’s downgraded First Quantum Minerals’ (FQM) rating to ‘B2-negative outlook’, due to high capex committed to developing the Cobre Panama mine and high net debt levels of US$5.2 billion. Following the rating downgrade, FQM targeted to reduce net debt by US$1.0 billion by end of Q1 2016, through asset sales and strategic initiatives. On October 5, 2015, FQM entered into a streaming arrangement with Franco-Nevada, linked to production at Cobre Panama for initial funding of US$330-340 million.21

Karnalyte Resources received a proposal from Braich Group on September 21, 2015. As per the proposal, Braich showed interest in making a significant investment in Karnalyte, in return for which Braich would acquire control of the company. The Karnalyte board is considering the proposal along with other strategic options which include debt-financing by its largest shareholder, Gujarat State Fertilizers and Chemicals.22

Although most of the players are making efforts to control costs, declining metal prices will put further pressure on profitability. Gold prices can be expected to remain volatile due to uncertainty over the interest rate hike by the US Federal Reserve. Some investors are using this recent upturn to book profits and move their investments in other asset classes. In addition, metal prices are expected to be affected by a macro-economic slowdown in China.

Mining companies are vulnerable to global economic uncertainty and changing investor sentiment. Some Canadian mining companies are likely to sell their assets to manage debt but will face limited interest from the various investors for these assets. While the current pricing suggests bargains may be available, the volatility and demand concerns make pricing very difficult and it takes a brave management team to make a decision to invest much needed capital in an acquisition. Despite the level of interest from private capital acquirers growing, the market remains tight and asset sales difficult to exec.

1. “Acquisition of 50% interest in Zaldivar copper mine”, Antofagasta press release, 30 July 2015.

2. “Barrick announces streaming agreement with Royal Gold”, Barrick press release, 05 August 2015.

3. “Barrick Announces Early Tender Date Results of Debt Tender Offer and Amendment to Maximum Tender Amount”,Barrick press release, 14 October 2015.

4. “Zaldivar $1bn sale accretive . . . but balance sheet running to stand still”, Deutsche Bank, 30 July 2015.

5. “OceanaGold to acquire Romarco creating the lowest cost gold producer globally”, OceanaGold press release, 31 July 2015.

6. “Securing a cornerstone asset”, Macquarie Research, 31 July 2015.

7. “Goldcorp acquires New Gold’s 30% interest in the El Morro project in Chile; creates 50/50 joint venture with Teck’s Relincho project”, GoldCorp press release, 27 August 2015.

8. “Bolstering the Balance Sheet with Sale of El Morro Stake”, TD Securities, 28 August 2015.

9. “Endeavour Mining announces strategic long term African gold partnership with Naguib Sawiris and La Mancha”,Endeavour Mining press release, September 21, 2015.

10. “US$540 million construction financing; production decision for Brucejack”, Pretium Resources press release, 15 September 2015.

11. “Financing package advances Brucejack to construction phase”, Scotiabank Research report, 16 September 2015.

12. “Alacer gold signs $250 million project finance facility”, Alacer Gold press release, 21 September 2015.

13. “Investment from Beijing Tairui Innovation Capital Management Ltd.”, Western Potash press release, 16 September 2015.

14. “North American Palladium completes rights offering”, North American Palladium press release, 15 September 2015.

15. “Imperial files final rights offering circular and provides pricing on financings”, Imperial press release, 20 July 2015.

16. “Kennady diamonds closes final tranche of $48 million non-brokered private placement”, Kennady Diamonds press release, 08 October 2015.

17. “Proposed Sale of Cobar and/or Lomas Bayas Copper Mines”, Glencore press release, 12 October 2015.

18. “Glencore conference call”, 07 September 2015.

19. “Update on Glencore’s plans to reduce net debt and adapt the business to the current commodity landscape”,Glencore press release, 7 September 2015.

20. “Barrick Gold Q2 2015 conference call”, 06 August 2015.

21. “First Quantum Minerals Updates on Key Developments and Actions”, First Quantum press release, 5 October 2015.

22. “Karnalyte resources inc. provides clarification to Braich press release issued on September 30, 2015”, Karnalyte press release, 05 October 2015.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments