Macquarie’s Brian Bagnell: Forget peak oil; worry about peak demand

Brian Bagnell of Macquarie Capital Markets has two caveats for investors in junior oil and gas companies: Expect extreme volatility, and don’t expect oil prices above $70/barrel anytime soon. He tells the The Energy Report that the winners in this sector will demonstrate maximal efficiency and minimal costs, and that even in this time of crisis there are bargains to be had.

The Energy Report: Oil prices have made a minor recovery, with West Texas Intermediate (WTI) at about $50/barrel ($50/bbl) and Brent at about $60/bbl. Where are oil prices going in the short term?

Brian Bagnell: That’s a hard question to answer. What we know for certain is that prices will remain volatile throughout H1/15. The numbers bear this out, with the global supply/demand overbalance predicted to come in around 1.5 million barrels per day (1.5 MMbbl/d) in Q1/15 and 1.9 MMbbl/d in Q2/15.

TER: The U.S. oil rig count reached a five-year low earlier this month. How long before U.S. oil production shows a significant decline?

BB: Our commodities team thinks the loss of another 150 rigs in the U.S. will bring the growing disparity between supply and demand back into balance. The rig count is being reduced by about 80 rigs per week, so the reduction will take a couple of weeks. Losing any additional rigs could mean we start seeing declines in late 2015.

TER: When U.S. production declines, will we see a price spike?

BB: No. I don’t think we’ll be back to $70/bbl anytime soon. The forward curve for WTI—what we call the strip—suggests we will hit $60–61/bbl by the end of this year. That seems reasonable to me.

TER: Do you believe in peak oil?

BB: No, I don’t. Higher prices tend to spur innovation. We once thought that peak oil existed, but that was before we discovered horizontal drilling and multistage fracturing, etc., and those technologies still have not been applied to shale reservoirs worldwide. Potentially, a lot of untapped resource in the world still can be accessed through newer technology and improved efficiency. It is possible we could see peak demand before peak supply.

TER: Many oil majors and the banks that lend them money have taken tremendous hits with the collapse in the oil price. Does this suggest that loans will not be available for expansion of shale oil drilling in the near future?

BB: Most bank lines are tied to reserve growth. What we’ve seen this year, so far, are year-over-year reserve increases. And the banks have tended to use price decks in the $65/bbl or higher range, which is obviously much higher than the current strip. This suggests they are still willing to increase credit lines, even in this environment.

TER: What conditions would lead to oil prices once again topping $100/bbl?

BB: In the next couple of years, I can imagine only two. The first would be a geopolitical event, such as a Nigerian civil war or even greater turmoil in Libya and Syria. The second would be a decision by member nations of the Organization of the Petroleum Exporting Countries (OPEC) to break ranks and act unilaterally to decrease production.

TER: Would open Russian military involvement in Ukraine count as one of those geopolitical events?

BB: Probably not. Ukraine is more of a gas-producing country than an oil-producing country. Armed retaliation against Russia from outside could cause prices to spike, but I highly doubt oil prices would reach $100/bbl.

TER: Since September, the price of natural gas has fallen from above $4.20 per million British thermal units ($4.20/MMBtu) to below $2.80/MMBtu. How badly has this drop hurt producers and explorers?

BB: It’s had a tremendous impact. In this gas price environment, the key to survival is to have the lowest possible cost structure. We have seen some Canadian producers with low cost structures demonstrate pretty resilient share prices, even though gas prices are near five-year lows. There is a lot of gas out there, and only the most productive wells and efficient companies will continue to make a profit.

TER: In the current cycle, how important is cash flow for oil and gas juniors?

BB: Cash flow is always king—the foremost consideration for all oil and gas companies in any commodity price cycle. It’s more important now than ever. Cash flow is the top metric we examine, so long as the company looks solvent. And it is of even greater importance to the juniors, as they don’t tend to have as much access to capital as larger companies.

TER: What’s your favorite Western Canadian junior gas producer?

BB: Advantage Oil and Gas Ltd. (AAV:TSX; AAV:NYSE). This company was a very different entity a year ago, when it was consolidated uneasily with a company called Longview Oil Corp. Advantage has since sold Longview to Surge Energy Inc. (SGY:TSX), and has become a pure-play Montney producer with a large, contiguous land base in the Glacier region of western Alberta.

This company is trading at a discounted multiple compared to the rest of its peer group. It has a very solid balance sheet, and a decent amount of production growth coming in 2015, most of which has already been paid for and drilled. On a combined basis, cash costs have averaged between $6–7/barrel of oil equivalent ($6–7/boe) over the last couple of quarters, which puts Advantage in the conversation about lowest cash costs in western Canada. In a poor natural gas environment, all this looks very attractive.

TER: Advantage shares are up significantly recently.

BB: The whole market has been up. Several Canadian small- and mid-cap companies are up similar amounts in the last few weeks. DeeThree Exploration Ltd. (DTX:TSX.V) comes to mind. But from my discussions with institutional investors, there is not a lot of attention being paid to Advantage as compared to some of its higher profile peers, such as Peyto Exploration and Development Corp. (PEY:TSX; PEYUF:OTC) and Tourmaline Oil Corp. (TOU:TSX).

TER: Advantage has announced its intention to spend $735 million ($735M) in capital expenditures (capex) over the next three years. What do you make of that?

BB: That has been the company’s plan for quite a while. And Advantage has been executing according to that plan, framed within the prevailing commodity prices environment of the last couple of years. The company recently reduced its three-year capex forecast to $545M; it was able to do so because of higher productivity and lower than expected declines from its 2013 Montney wells. Not a single one of its 33 wells drilled in 2014 has yet been tied in, which means the company can cut back on its spending and still hit its three-year growth targets. We like that Advantage has a measured, achievable pace of growth that it can finance internally; in my opinion, the market isn’t paying for big growth numbers anyway, like it was in mid-2014. Companies are being rewarded more now for having sustainable balance sheets.

TER: How big a producer could Advantage become?

BB: Quite large, if it were to continue to fulfill the $735M plan. Certainly, the company could close to double its current production. Producing up to 50 thousand barrels of oil equivalent per day (50 Mboe/d) is not out of the question.

TER: Which new Alberta oil junior do you like?

BB: We recently initiated coverage on Toro Oil & Gas Ltd. (TOO:TSX.V), the newest western Canadian junior to be publicly listed. It is focused in the Alberta Viking play in the Provost-Halkirk region. It acquired its main asset from Zargon Oil & Gas Ltd. (ZAR:TSX) in November.

There are a few interesting things about this company. The management has had past success. President and CEO Barry Olson was formerly CEO of Orleans Energy Ltd., which discovered the Ante Creek Montney pool and then merged with RMP Energy Inc. (RMP:TSX) in 2011. RMP has gone on to be very successful, with one of the most attractive assets in western Canada. Toro is focused on high netback Viking oil. Of course, netbacks for all oil plays in the current environment are challenged, to say the least, but the Viking is one of the plays we think will recover the soonest.

TER: How does Toro stand for cash?

BB: It has $12M cash on its balance sheet, which is a boast very few Canadian junior oil and gas companies can make today. Most have some form of bank debt, and that is hurting them in this environment. Toro, with its access to a $25M credit line, is in a position of strength.

TER: How does Toro’s resource base compare to those of its peers?

BB: We have compared it to Beaumont Energy Inc., a private oil and gas Viking producer in Saskatchewan. Beaumont acquired a similar-size pool in late 2012, began horizontal drilling on it right away, and was able to grow production from 1,000 barrels per day (1 Mbbl/d) to between 5–6 Mbbl/d in about two years. Toro’s oil pool is very similar to Beaumont’s, and it has seen very little horizontal development to date. With proper application and drilling techniques Toro should be able to enjoy a success similar to Beaumont’s. That is certainly not being priced into the stock today.

TER: You initiated coverage of Toro on Jan. 30 with a 12-month target price of $1.50/share. Shares are currently trading at about $0.68. That would be a 124% increase.

BB: Yes. But that puts the stock at only a median multiple. The target price is based on a multiple derived from the average of all the Canadian small- and mid-cap companies we have under coverage today.

TER: Can you discuss a natural gas junior you recently assumed coverage on?

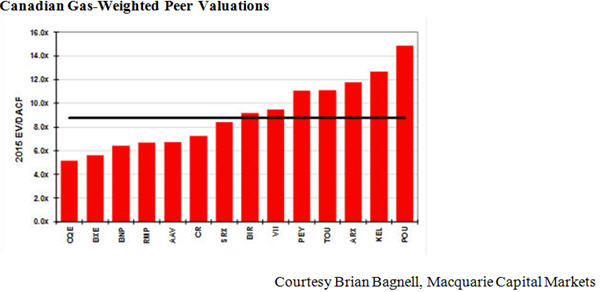

BB: Storm Resources Ltd. (SRX:TSX.V) is another company doing great things in the Montney. Its main asset is in the Umbach region of British Columbia. It has increased its type curve every year, all while showing pretty significant production growth from its Montney wells. The company is reasonably valued and has a very conservative management team, which I like a lot. I like a team that doesn’t grow just for the sake of growth.

TER: How does Storm’s balance sheet look?

BB: We quote based on current forward pricing, which we update every week because we don’t think the market is paying us for our commodity price forecasts. We think investors want to know where a company is trading on market-implied pricing. On that pricing, we see Storm staying below 1.8x debt:cash-flow through 2015, which is in the top tier of peers. We have Storm trading at around 9x 2015 enterprise value:debt-adjusted cash flow, which is about the median multiple of the gas-weighted group in Canada. It ranks among the highest of the gas-weighted group on current forward pricing in terms of production/share growth and cash flow/share growth.

TER: What are the company’s prospects for growth?

BB: We like that Storm doesn’t give itself credit for much outside its core Umbach region, even though it appears the company has a lot of resource potential there and also, potentially, in the lower layers of the Montney. Storm’s share price has been on a roll in the last month, and we think it’s trading at a very reasonable valuation today.

TER: Can you name another Alberta junior that’s not growing solely for the sake of growth?

BB: Manitok Energy Inc. (MEI:TSX) has decided to suspend drilling at its Entice and Stolberg properties and apply 80% of its cash flow to debt reduction in H1/15. This is a prudent move. This is survival of the fittest, and maintaining a flexible balance sheet so that you can come out on the other side when commodity prices improve is crucial.

This company has had some good wells out of Entice, and some not-so-good wells. We think Manitok has a lot of potential in some of the formations on that property, but today, most of those wells are likely not economic. It makes more sense to wait the downturn out.

TER: Manitok has hedged 70% of 2015 oil production at $93.67/bbl WTI, and its 2015 natural gas is hedged at $3.47/MMBtu. Is this prescient or commonplace?

BB: It’s quite uncommon, actually. It is at the very high end of the entire Canadian small- and mid-cap space for hedging—probably the entire oil and gas universe. A lot of what Manitok has for hedges are in the form of puts. That’s a way to protect the downside without locking in your upside. Hindsight is always 20/20, but right now, what Manitok has done with hedging looks absolutely fantastic.

“There is a lot of gas out there, and only the most productive wells and efficient companies will continue to make a profit.”

I am personally a fan of hedging, and I think any company with a big growth component in its platform should hedge a considerable part of its production. This mitigates commodity price environments like today’s, when unhedged companies are forced to shelve rigs and abandon growth. Manitok is in good shape because of its prudence, and yet it is trading very cheaply versus its peers.

TER: Let’s talk an oil and gas junior outside North America you follow.

BB: Serinus Energy (SEN:TSX) has operations in eastern Ukraine, Tunisia and Romania. Obviously, with all the strife in eastern Ukraine right now, it’s having a tough time. While the troubles haven’t affected its drilling operations, the government in Kiev has imposed policies that make it difficult for this company. For instance, capital controls have been instituted, and now it is essentially illegal for cash to be sent out of the country. Serinus gets most of its cash flow from its Ukrainian operations.

TER: Serinus’ Ukrainian operations are in the Donbass, the region that has demonstrated support for Russia, correct?

BB: Yes, but its operations are north of the areas that have seen the most fighting.

TER: What’s your opinion of Serinus’ operations in Romania and Tunisia?

BB: Its Moftinu project in Romania is very early stage. Both its wells discovered multiple hydrocarbon-bearing zones, and the company is moving forward with completion and testing in mid-March. It’s really too early to call, but it looks to be a very interesting prospect.

Serinus’ Sabria concession in Tunisia is more advanced. Its first horizontal well there started producing at a rate of 635 boe/d and grew to 1 Mboe/d after cleanup, an excellent result that warrants further exploration and development drilling.

TER: To close, can you describe a good 2015 strategy for oil and gas investors?

BB: Again, this space will be characterized by extreme volatility, so it will not be for the faint of heart in the short term. Many Canadian companies are implying WTI prices of $70/bbl or higher, which means that they’ve already priced in a large chunk of the pending recovery.

TER: Is this perhaps a good environment for bargain hunters?

BB: There are some bargains to be found within the Canadian energy space. Some examples would be Advantage Oil and Gas, DeeThree Exploration and RMP Energy. All three are still trading at discounted valuations and could have potential for a catch-up trade.

TER: Brian, thank you for your time and insights.

Brian Bagnell, CFA, is a research analyst in Canadian oil and gas company analysis for Macquarie Capital Markets in Calgary. He was formerly an investment associate at the NB Investment Management Corp. He holds a bachelor’s degree in business administration (finance and accounting) from the University of New Brunswick.

Brian Bagnell, CFA, is a research analyst in Canadian oil and gas company analysis for Macquarie Capital Markets in Calgary. He was formerly an investment associate at the NB Investment Management Corp. He holds a bachelor’s degree in business administration (finance and accounting) from the University of New Brunswick.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Source: Kevin Michael Grace of The Energy Report

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Manitok Energy Inc. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Brian Bagnell: I own, or my family owns, shares of the following companies mentioned in this interview: None. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Manitok Energy Inc., Toro Oil & Gas Ltd., DeeThree Exploration Ltd., RMP Energy. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent. Oil and stock prices were current as of the date of publication.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

Streetwise – The Energy Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Energy Report. These logos are trademarks and are the property of the individual companies.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments