London nickel market tightens as China lifts imports

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

London Metal Exchange (LME) nickel stocks have been falling relentlessly since April of this year.

Exchange inventory has slumped to 110,688 tonnes from 264,606 tonnes over the last six months with almost half of what is left canceled in preparation for physical load-out.

LME time-spreads have been tight since the middle of October. The cash premium hit $190 per tonne last month and was still a wide $141 at Friday’s close.

Some of what is leaving the LME’s warehousing system is heading for China.

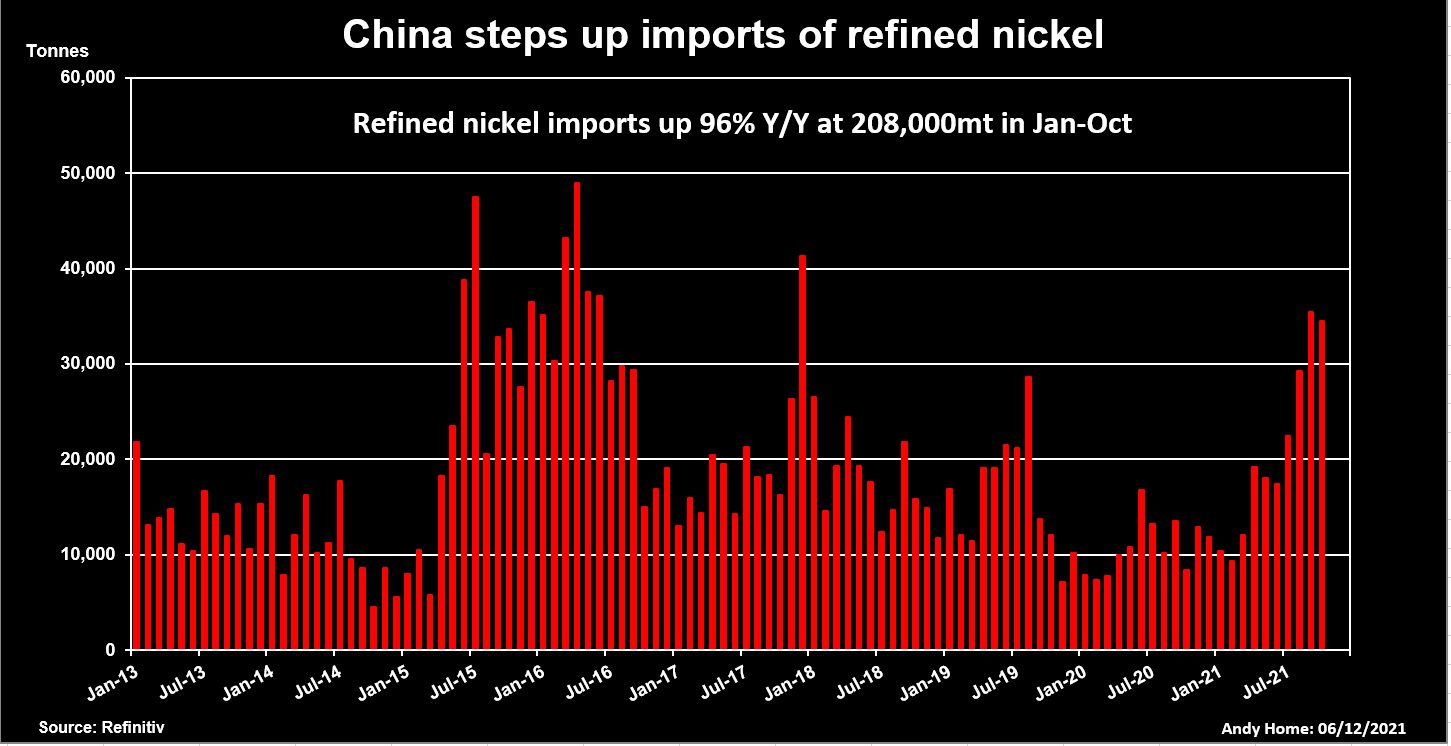

The country’s imports of refined nickel have accelerated appreciably since April with the cumulative January-October tally of 208,000 tonnes up 96% on the same period last year.

China’s recent import appetite is now stretching availability in a market already caught out by the strength of demand this year.

China’s import appetite grows

China’s imports of refined nickel were 35,500 and 34,500 tonnes in September and October respectively, the highest monthly tallies since December 2017.

Cumulative imports of 208,000 tonnes over the first 10 months of this year are almost double last year’s equivalent level and the strongest since 2016.

China had been importing less refined nickel in recent years as it stepped up purchases of raw materials, particularly Indonesian nickel pig iron destined for the stainless steel sector.

Inbound shipments of such raw materials remain robust. Those from Indonesia were up 21% year-on-year over January-October. Imports of intermediate nickel products were up by 29% and those of nickel ore and concentrates by 16%.

However, the domestic market for nickel in refined form has been tight, which has fed into a rolling squeeze on the Shanghai Futures Exchange (ShFE).

Shanghai exchange inventory has remained extremely low throughout 2021 and closed last week at just 5,563 tonnes, any sustained rebuild hindered by the limited number of non-Chinese brands deliverable against the contract.

Those from Russian producer Norilsk are deliverable and it’s noticeable that imports from Russia have surged to a combined 17,300 tonnes in September and October, more than total arrivals in the first eight months of the year.

Domestic availability of refined nickel has been constrained this year by a maintenance closure at dominant producer Jinchuan Group and by Jilin Jien’s switch from producing refined metal to nickel sulfate.

More recently, energy-saving measures across multiple Chinese provinces have hit power-hungry nickel pig iron producers, creating added displacement demand for nickel in refined form.

Demand boom

While Chinese supply has struggled, domestic demand has boomed this year, as it has everywhere else.

Most nickel still gets fed into stainless steel furnaces and global stainless production has been resurgent in 2021, registering year-on-year growth of 25% in the first half, according to the International Stainless Steel Forum.

Electric vehicle batteries are still a small part of the nickel usage picture but a fast-growing one.

Demand for battery-grade nickel in China, the world’s largest EV battery supplier, is showing up in super-charged imports of nickel sulfate. January-October arrivals totalled 35,900 tonnes, up from just 4,800 tonnes in the same 10-month period of 2020.

The combined strength of old and new nickel-consuming industries has defied expectations.

When the International Nickel Study Group (INSG) held its October 2020 meeting, it expected global demand to rise by 9% this year.

When it met in April 2021, it lifted that demand growth forecast to 12%. The most recent forecast from the Group’s meeting in October was higher still at 16%.

These are super-charged growth figures, even allowing for the economic snapback from covid-19 lockdowns last year.

They have also translated into a much wider-than-expected gap with supply, which has suffered multiple hits in China and the rest of the world.

Widening the gap

The INSG forecast a 2021 supply-demand surplus of 68,000 tonnes in October last year.

Fast forward to October this year and its most recent assessment is for a 134,000-tonne supply shortfall in 2021.

Even that drastic revision may need a few further tweaks. The Group’s latest monthly update for September suggests supply fell short of demand to the tune of 175,000 tonnes in the first 9 months of the year.

The INSG is forecasting a return to a modest, 76,000-tonne surplus next year as the stainless demand surge abates and nickel supply recovers, particularly in Indonesia, where producers are rapidly expanding capacity.

However, many of them are going down innovative technical paths in the collective attempt to pivot towards the type of product used for battery manufacture.

The risk of supply underperforming next year is one of the reasons analysts at JPMorgan are expecting deficit conditions to persist through at least the first half of 2022.

JPMorgan, indeed, has revised “materially higher” its nickel price forecasts to $23,000 per tonne in the first quarter of next year and $22,000 in the second. (“Base and Precious Metals 2022 Outlook,” Nov. 29, 2021)

The LME three-month nickel price is currently trading at $19,800 after peaking in October at $21,425 per tonne, its highest trading level since 2014.

As ever in the nickel market, everything will depend on what happens in Indonesia, where the next wave of supply is building.

Before it arrives, however, nickel looks set to remain a tight market with the flow of metal into China transferring the tightness from Shanghai to London.

(Editing by Emelia Sithole-Matarise)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments