Lead, the bull market no-one wants to buy into

Historically low stocks, a yawning supply deficit and a depleted pipeline of future mine growth. Lead has all the hallmarks of a classic bull commodity story. Yet the unglamorous metal has been the worst performer this year among the core base metals traded on the London Metal Exchange (LME).

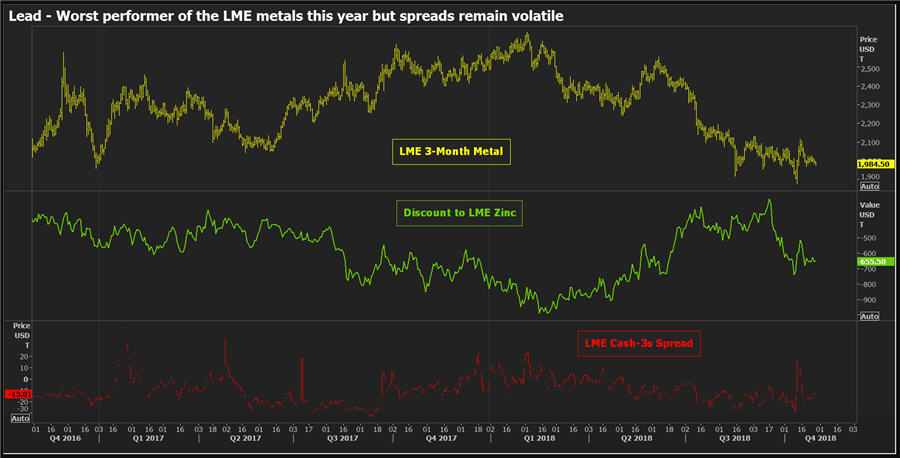

LME three-month lead is currently trading around the $2,000 per tonne level, down almost 23 percent since the start of 2018 and struggling to recover from the two-year low of $1,876 recorded earlier this month.

Fund managers don’t like lead’s toxic past and they don’t much like its future prospects either.

Lead’s demand fortunes are inextricably tied to the batteries used to power conventional internal combustion vehicles, which means the metal is likely to be one of the main casualties of the electric vehicle revolution.

This lack of investment “sex appeal” leaves the lead price beholden to the gyrations of zinc, the second-weakest LME performer this year. Indeed, the ever-popular relative value trade between the two “sister metals” is at times a price driver in its own right.

Yet, lead’s supply problems are more structurally severe than those of zinc and the divergence in supply performance is only going to grow.

Wide deficit, low stocks

The International Lead and Zinc Group (ILZSG) has just drastically revised its estimate of supply-demand balance in the lead market. At its October meeting the group lifted its assessment of the supply deficit this year to 123,000 tonnes from its April forecast of 17,000 tonnes. While projected demand growth has been slashed to just 0.2 percent from 2.7 percent, the supply side of the equation has come in for even more radical revision.

Mine supply, which was expected to grow by a robust 4.2 percent in April, is now expected to fall by 0.2 percent this year. That in turn will drag refined metal production growth down to just 0.4 percent from a previous forecast of 3.8 percent. The ILZSG’s estimates are broadly in line with those of Wood Mackenzie, although the research group has a slightly different deficit timeline.

But, according to Farid Ahmed, Woodmac’s lead analyst, “what is certainly true is that our 2018 mine supply figures have continued to fall throughout the year” to the tune of around 450,000 tonnes, split fairly evenly between China and the rest of the world. Current deficit in the lead market mirrors that in the zinc market and reflects the closure over the last few years of major mines which produced both “sister” metals. Environmental crackdown in China, meanwhile, has hollowed out the country’s traditional role as swing producer of both metals during periods of tightness.

As with zinc, mine supply constraints have fed through to the refined metal part of the lead supply chain. LME stocks of lead currently stand at 111,500 tonnes, their lowest level since 2009. In China the amount of lead registered with the Shanghai Futures Exchange has slumped by 35,869 tonnes since the start of January to just 6,139 tonnes. None of which has impressed investors. Speculators hold a larger short position on LME lead than any other metal at 22 percent of open interest, according to LME broker Marex Spectron. Look no further to understand why lead is so bombed-out even by the standards of a sector that has been aggressively sold as a proxy for global trade woes. Only sporadic bursts of time-spread tightness, the most recent earlier this month, betray lead’s struggling supply profile.

Sanctions and scrap

The ILZSG expects lead mine supply to bounce back next year to the tune of 4.1 percent growth with a corresponding shift in refined metal market balance to modest 50,000-tonne surplus. As ever, this reflects the dynamics of the zinc market. A host of new zinc mines will generate a mini-surge of by-product lead.

However, there are two important caveats.

Firstly, lead is facing far more supply-chain disruption from U.S. trade policy than its sister metal. China lost one key supplier of mine concentrates in the form of North Korea, sanctioned by the U.S. administration last year. All imports from what had been the country’s four-largest supplier of raw material ground to a halt in October 2017. Its second-largest supplier last year was the United States, with imports totalling 212,000 tonnes. However, that flow of raw material is likely going to be hit hard by the 10 percent tariffs imposed by China in the latest round of tit-for-tat trade measures. It’s noticeable that while Chinese smelters are now receiving better terms for treating zinc concentrates, there has been little discernible improvement in lead treatment charges.

Secondly, the long list of pending zinc mine projects is surprisingly light on lead. Analysts at ICBC Standard Bank, for example, note that while zinc mine capacity will grow by 2.2 million tonnes per year, or 17 percent of 2017 production, in the years to 2021, lead mine capacity will grow by just 486,000 tonnes per year, or 11 percent of 2017 output. (“Base metals outlook”, October 2018) True, such primary supply constraints will be mitigated by secondary supply in the form of lead being recycled back into the supply chain.

However, the scrap component of lead supply has itself faced significant disruption as Chinese authorities clamp down on lead recyclers and secondary production rates are driven not by market mechanics but by the availability of obsolete lead-acid batteries.

Mine supply, in other words, will continue to be the key determinant of overall lead market balance.

Sunset industry?

Right now lead is arguably considerably more bullish a market than zinc.

Investors, however, are loathe to commit to the lead market, transfixed as they are by the bear narrative of a sunset industry that has already seen e-bike usage peak and now faces the prospect of lead-acid battery technology succumbing to the electric vehicle revolution. It will be many years, however, before lead drops out of the automotive battery picture. And until it does, this metal is going to continue to face supply challenges, ones which for once will not be alleviated by sister metal zinc. Does that mean funds will reassess how they think about lead relative to zinc? Probably not, unless there is a true supply-side lead shock.

But it does suggest that the time-spread tightness that has characterised the LME lead contract over the last two years is going to remain a feature of the market.

(By Andy Home; Editing by David Evans)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

{kind=link}

Comments