Ivan Glasenberg places a dirty $36B bet: Chris Bryant

Higher U.S. bond yields have made the payouts offered by most stocks look pretty underwhelming lately. Not so Glencore Plc, whose implied yield is startlingly high even though it’s throwing off cash like it’s going out of fashion.

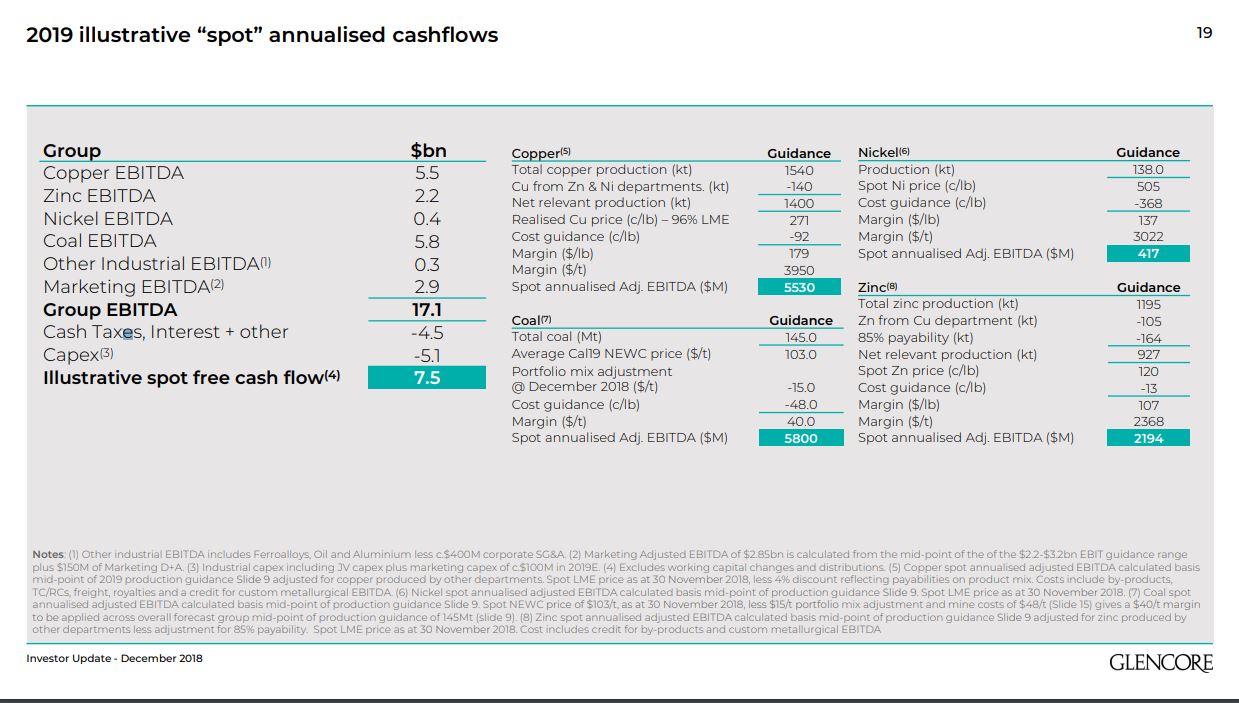

The miner-cum-trader thinks it can generate $7.5 billion of free cash flow next year at current commodity prices. Absent a downturn in the economy, it’s conceivable that the company will return all of that to shareholders via dividends and buybacks, it said on Monday. Here’s the relevant slide:

The market shrugged at its largess, even erasing some of the gains Glencore had enjoyed from the easing of U.S.-China trade tensions. The shares have dropped more than 21% this year and trade on less than 8 times estimated earnings.

Glencore’s cash flow projection indicates a whopping 14% yield – the amount investors get back as a percentage of the share price – should it indeed return all of the cash via dividends and buybacks. The company is poised to generate almost half its market value in cash in just three years, according to the Bloomberg consensus forecast. So why aren’t shareholders clamoring for a slice of the spoils?

Demand for Glencore’s commodities remains pretty robust and miners have been more reluctant to do the expansionary capital spending that got them into trouble in the past. Net debt has declined enough to let Glencore hand back heaps of cash to shareholders. Hence, chief executive Ivan Glasenberg thinks Glencore’s valuation handicap boils down to two issues. First, there’s the Democratic Republic of Congo, where Glencore has large copper and cobalt assets and has faced of string of government and legal problems. And then there’s coal.

There’s not much Glasenberg can do about a new Congolese mining code that penalizes foreign producers, other than keep appealing for a better settlement.

If Glasenberg is right, his shareholders will be swimming in cash, even as our oceans creep higher.

Nor does the company have any influence over a U.S. Justice Department probe into possible corruption and money-laundering in the DRC, Venezuela and Nigeria. But even if Glencore is whacked by a fine from Washington, it’s questionable whether it will be anywhere near the $5 billion wiped off the stock when the subpoena landed in July.

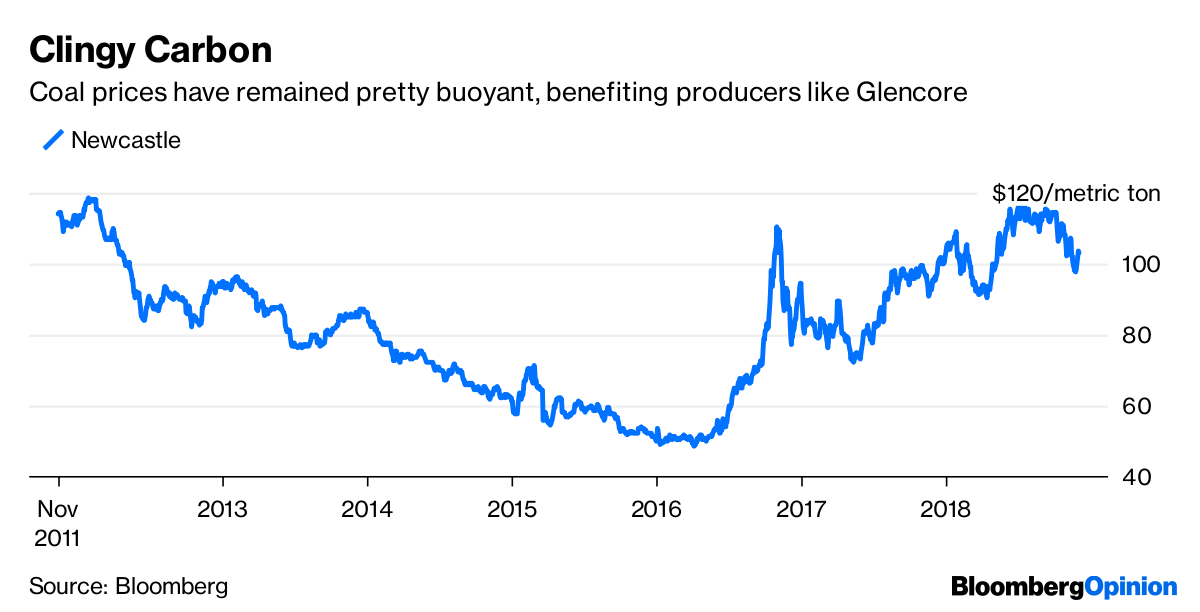

A bigger impediment, in valuation terms at least, is that investors aren’t willing to ascribe full value to Glencore’s thermal coal business. The company anticipates almost $6 billion of Ebitda from coal in 2019, more than it will generate from copper at current prices. Apply a typical deal multiple and the coal business is worth about $36 billion, thinks Glasenberg. That’s close to half the company’s enterprise value.

With international delegates meeting in Poland this week to debate the unfolding planetary climate emergency, it’s tempting to view the market’s thumbs down on coal as ethical. Glencore talks a lot about the copper and cobalt it will supply for electric vehicles, but it’s made a huge bet on carbon. Some sustainability-minded investors won’t touch Glencore’s shares for this reason, but that’s probably not why the coal business has been marked down. Rather, investors worry that high thermal coal prices aren’t sustainable. It’s possible they’re wrong about that. Glasenberg certainly thinks so.

Corporate boards and banks are increasingly unwilling to sanction or finance new coal mines, meaning there’s a dearth of new supply. That’s a huge advantage for miners that refuse to quit the coal game. In particular, Glencore profits from the premium that utilities pay for higher grade coals. With India and China constructing lots of new coal capacity, demand isn’t about to fall off a cliff either, whatever climate campaigners hope.

In the long run, high prices may end up dooming coal, as my colleague David Fickling has argued. But Glencore’s coal business should be a license to print money for several more years. If Glasenberg is right, his shareholders will be swimming in cash, even as our oceans creep higher.

(By Chris Bryant)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments