Iron ore’s recent reversal likely the start of longer slide: Russell

Iron ore prices are in retreat as the market starts to factor in realities that it has previously been happy to ignore in the euphoria of a strong rally.

As always when prices start to decline after a surge that appeared unrelated to supply-demand fundamentals, the question is will the reverse become a rout and where exactly does fair value lie?

It’s worth noting that the current slump was led by iron ore futures traded on China’s Dalian Commodity Exchange (DCE), a market dominated by local investors, as opposed to the more professional and industry-favoured spot and Singapore Exchange (SGX) contracts.

The benchmark DCE contract has declined 17.6 percent since its recent closing peak of 601.5 yuan ($91.40) a tonne on Aug. 22, ending on Wednesday at 495.5 yuan.

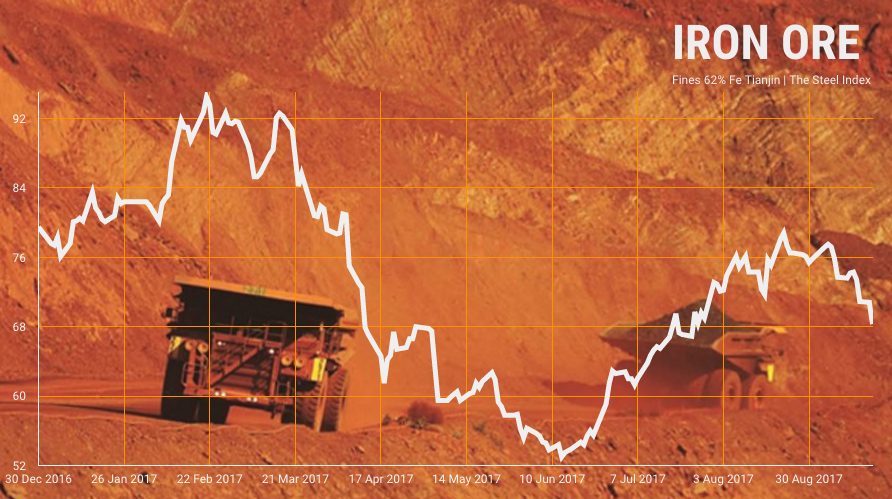

In contrast, SGX futures, which are priced against the Steel Index spot assessment, have slipped 7.8 percent from their recent high of $77.80 a tonne on Sept. 5 to end at $71.72 on Wednesday.

SGX futures are now below the $79.75 a tonne they fetched at the end of 2016, but have had a volatile year so far, reaching more than $90 a tonne in March before falling to $53.66 by mid-June, and then staging a strong rally before the current reversal.

However, the DCE contract is still above the 2016 year-end price of 438 yuan a tonne, which suggests there is still further room for it to fall before its performance more closely matches that of the SGX futures.

How much further and how quickly iron ore prices drop will likely depend on how the market views the current dynamics around Chinese steel output and demand.

Certainly, rising steel prices and production in recent months have dragged iron ore along for the ride.

STEEL REVERSAL

Chinese steel output hit a record of 74.59 million tonnes in August, up 8.7 percent on the year-earlier month and beating the previous record set just one month earlier in July of 74.02 million tonnes.

Prices of benchmark steel rebar in Shanghai reached a 4-1/2-year earlier this month, although the contract has fallen 8.6 percent since the closing-high of 4,098 yuan a tonne on Sept. 4.

The slide in prices comes amid signs that August’s record-high may be close to the highwater mark for Chinese steel output, at least for now, as environmental inspections are ramped up, and authorities at several levels of government weigh enforcing closures in coming months in order to reduce pollution levels in winter.

The municipal government of the capital Beijing said it would suspend construction of major public projects during winter to improve the capital’s air quality, official media reported on Sept. 17.

It’s also possible that the ruling Communist Party may tilt economic policy in favour of reform and away from stimulus at next month’s Chinese People’s Congress, a major policy-setting meeting.

There is also no shortage of both iron ore and steel inventories in China.

Iron ore port stocks are down slightly from the recent record-high of 141.4 million tonnes in June, but at 131.8 million for the week to Sept. 15 they are still well above the 80 million that prevailed at this time last year.

Steel rebar inventories display a more seasonal pattern, building in winter and drawing in summer, in line with the peaks and troughs of the construction cycle.

They were 4.34 million tonnes in the week to Sept. 15, up from 4.24 million for the same week a year earlier.

With the risks to steel output and demand becoming more apparent, it was only a matter of time before investors grew wary of the rally in iron ore and decided to take profits, or scale back exposure.

There is also the likelihood of increased supply in coming months and in 2018, with the Australian government forecaster expecting Brazil’s Vale, the world’s biggest iron ore miner, to increase its output to 400 million tonnes by next year, up from 360-380 million this year.

Australia is expected to increase iron ore exports to 885 million tonnes in the fiscal year ending June 2018, up from 851 million in the year ended June 2017, the Department of Industry said in its latest quarterly resources outlook.

Given the volatility of iron ore this year, making a price forecast is a fraught process, but a good indicator is the Australian government’s expectation that prices will average $55 a tonne in the second half of this year, and $48 in 2018.

(By Clyde Russell | Editing by Joseph Radford)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments