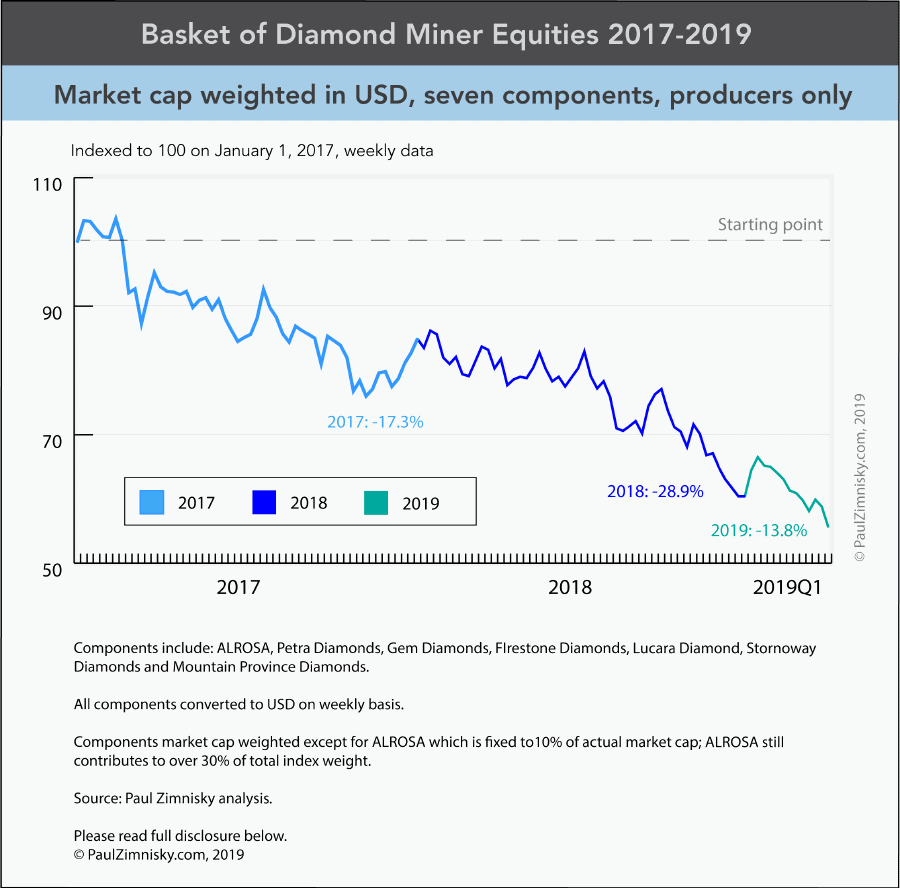

Investor sentiment in diamond mining stocks makes for a contrarian play

On Alrosa’s (MICEX: ALRS) Capital Markets Day on March 18th, the company said the most frequently asked questions it gets during 1-on-1 meetings with investors are those related to the impact that “synthetic” diamonds will have on the business.

Three days later, on a Mountain Province Diamonds (TSX: MPVD) analyst call following the company’s full year 2018 results, a portfolio manager posed more of a statement than a question in the Q&A portion of the call starkly reflecting a wider sentiment of institutional investors’ view of the diamond mining industry at the moment.

The PM bluntly addressed their opinion on the threat they believe lab-created diamonds pose to natural, saying “while I appreciate the attempts to kind of dance around the issue of lab-grown diamonds…I think we all have to just accept the fact that technological improvements will continue, technological progress moves forward and lab-grown diamonds will continue to be a much larger factor.” Further, he added an anecdote, “for those of us who have millennial children, they couldn’t care less whether it’s lab-grown or natural…if it sparkles, looks good and is a diamond, I think that’s what people are going to focus on.”

While frustration such as this is understandable for any investor that has had exposure to the space in recent years given the utter underperformance –diamond mining stocks have felt like a vortex that takes your money and does not give it back. However, it appears that sentiment has reached a level implying that the independent diamond mining industry will not survive, which is seemingly a stretch too far.

Yes, lab-created diamonds will inevitably take some market share from natural diamonds, especially at the lower price points, just as moissanite and cubic zirconia did, however the extent is yet to be determined and will most likely depend on the success of marketing by not just the lab-created industry, but also the natural industry, which has a very resilient history.

Historically, natural diamonds have been the envy of the luxury industry: the penetration of diamonds is unmatched, it is the one luxury item that most women (in American at least) will be gifted in their lifetime. However, maintaining such an overwhelming market position is almost as difficult as building it, especially in the post-De Beers monopoly era with the absence of “A Diamond is Forever” campaign.

While the challenge of maintaining market penetration in the industry’s most developed markets is offset by new growth in emerging markets, a couple of which (i.e. India and China) have the potential to eventually overtake the U.S. in size, the diamond industry undeniably faces aforementioned confrontation. Nonetheless, the natural diamond industry seems far from going away any time soon.

Natural diamond supply is estimated to come off this year and continue to incrementally decline through at least 2021, which should be supportive of diamond prices and thus miners. Weaker prices over the last five-plus years have led to a natural paring of supply which is approaching more normalized levels after reaching a post-global-financial-crisis high in 2017. Also worthy of note, a significant amount of a multi-year inventory-deleveraging in the Indian midstream sector has already taken place and inventories there are also approaching a more normal level.

In addition, despite various global macro-economic concerns, global demand for natural diamonds appears to be relatively stable at the moment. The largest jeweler in the world, Tiffany & Co. (NYSE: TIF), has guided sales increasing at a “low-single-digit percentage” in the 12 months ending January 31, 2020. Importantly, Tiffany does not offer lab-created diamonds. Further, the largest jeweler in Greater China, Chow Tai Fook (HK: 1929), opened a record number of new stores in the most recent fiscal year ended March 31, 2018, an undeniable bid of confidence in the growth potential of that market. Chow Tai Fook does not offer lab-created diamonds either.

While investor sentiment is what drives equity valuations, reflected by the “P” of the proverbial P/E ratio, or price-earnings multiple, the “E” is the portion of the equation ultimately driven by price fundamentals and operations which the industry poses control of. Seemingly stable global demand for natural diamonds and an apparent favorable supply picture should be supportive of diamond prices and the companies producing them, especially those with de-risked mining operations and a manageable debt load.

De Beers is currently 85%-owned by global diversified mining company Anglo American (LSE: AAL) and 15% by the Government of Botswana. Most of the company’s subsidiaries are joint ventures with government partners.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular analysis of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be reached at [email protected] and followed on Twitter @paulzimnisky.

Also, check out Paul Zimnisky’s new diamond podcast. The first episode featuring special guest Rob Bates from JCK Magazine can be streamed here. The podcast is also available for download on Apple iTunes and is accessible via the iPhone Podcasts app.

Disclosure: At the time of writing Paul Zimnisky held a long position in companies with exposure to the natural diamond industry including Lucara Diamond Corp, Stornoway Diamond Corp, Mountain Province Diamonds Inc, Diamcor Mining Inc, North Arrow Minerals Inc, Tsodilo Resources and Signet Jewelers.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments