How gold got its groove back

Who says gold lost its appeal as a safe haven asset?

After five straight positive trading sessions, the yellow metal climbed above $1,100 on a weaker U.S. dollar, its highest level in nine weeks. The rally proves that gold still retains its status as a safe haven among investors, who were motivated this week by a rocky Chinese stock market, North Korea’s announcement that it detonated a hydrogen bomb on Wednesday and rising tensions between Saudi Arabia and Iran.

Here in the U.S., gold finished 2015 down 10.42 percent, its third straight negative year. Until the new year, sentiment appeared poor, and many gold bulls were finding it hard to stay optimistic.

But after the price jump this week, large exchange-traded gold funds saw massive inflows, confirming a shift in investors’ attitude toward the precious metal.

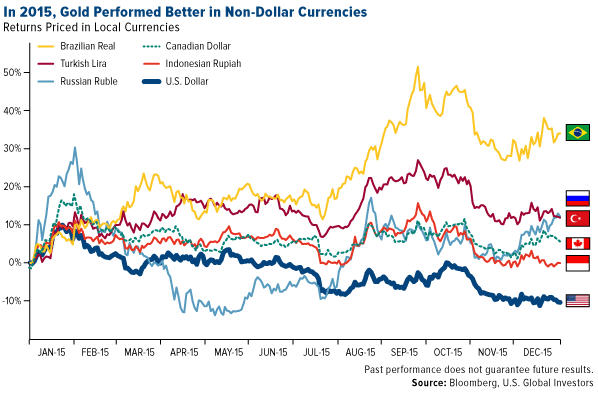

It’s worth remembering that about 90 percent of physical demand comes from outside the U.S., mostly in emerging markets such as China and India. In many non-dollar economies, buyers are actually seeing either a steady or even rising gold price. The metal is up in Russia, Peru, South Africa, Canada, Mexico, Brazil and many more.

Note the differences in returns between gold priced in U.S. dollars and gold priced in the Brazilian real, Turkish lira, Canadian dollar, Russian ruble and Indonesian rupiah.

Gold demand in China was very robust last year. A record 2,596.4 tonnes of the yellow metal, or a whopping 80 percent of total global output for 2015, were withdrawn from the Shanghai Gold Exchange. As for the Chinese central bank, it reported adding 19 more tonnes in December, bringing the total to over 1,762 tonnes. Precious metals commentator Lawrie Williams points out, though, that China’s total reserve figure is widely believed to be “hugely understated,” meaning the central bank might very well have much more than we’re being told.

Forget Interest Rates—Real Rates Are the Key Drivers of Gold

Despite all the talk of rising interest rates in connection to gold, they’re not a dominant driver of prices. Sure, rising nominal rates have tended to make the metal less attractive, since it doesn’t pay an income, but the larger driver by far are real interest rates. When real rates drop into negative territory, gold has historically done well.

As a reminder, real rates, important for the Fear Trade, are what you get when you subtract the consumer price index (CPI), or inflation, from the 10-year Treasury yield. As of January 6, the 10-year yield was 2.18 percent, while the 12-month CPI for November—December data will be released later this month—came in at a barely-there 0.50 percent. Real rates, therefore, are running at a positive 1.68 percent, which is a headwind for gold.

That’s why we need inflation to pick up, because then gold would be more likely to rally.

Regardless, the World Gold Council (WGC) writes in its 2016 outlook that gold’s role as a diversifier remains “particularly relevant”:

Research shows that, over the long run, holding 2 percent to 10 percent of an investor’s portfolio in gold can improve portfolio performance.

The reason for this is that gold has tended to have a low correlation to many other asset classes, making it a valuable diversifier. During economic contractions, for example, gold’s correlation to stocks actually decreased, according to data between 1987 and 2015.

For the last three years, gold has disappointed many because other investments, specifically equities, have seen such huge gains. But with global markets hitting turbulence, the yellow metal is looking more attractive as insurance against the currency wars.

I always recommend 10 percent in gold: 5 percent in gold stocks or an actively-managed gold fund, 5 percent in bullion and/or jewelry. It’s also important to rebalance every year.

This should be the case in both good times and bad, whether gold is rising or falling. As highly influential investment expert Ray Dalio said last year: “If you don’t own gold, you know neither history nor economics.”

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments