Graphic: Hefty shortages to help buoy aluminum prices this year

Supply disruptions in China due to problems with hydropower mean hefty shortages of aluminum this year, which are likely to offset slow demand growth and help bolster prices.

Smelter shutdowns in Europe due to high energy prices over the past couple of years and consumers there shunning Russian metal after Moscow invaded Ukraine last year make the problem particularly acute in the region.

Despite expectations of tight supplies, aluminum prices on the London Metal Exchange (LME) have come under pressure due to interest rate hikes in the United States and sluggish demand in top consumer China.

At $2,400 a tonne, they have dropped 10% since mid-January.

However, in recent weeks deficits have emerged, as seen in sliding inventories of aluminum used in the transport, construction and packaging industries.

In warehouses monitored by the Shanghai Futures Exchanges, aluminum stocks at 274,347 tonnes have dropped 12% over the last month. In LME approved warehouses, stocks have fallen 5% since mid-February.

Chinese production should rise, but at a slower pace than previously forecast due to power rationing and disruptions in provinces such as Yunnan where aluminum is mostly smelted using hydroelectricity.

“China’s smelters remain under pressure because of hydropower shortages. At the same time, demand should pick up, so exports will likely remain capped,” said Bank of America analyst Michael Widmer. “We expect rising deficits going forward.”

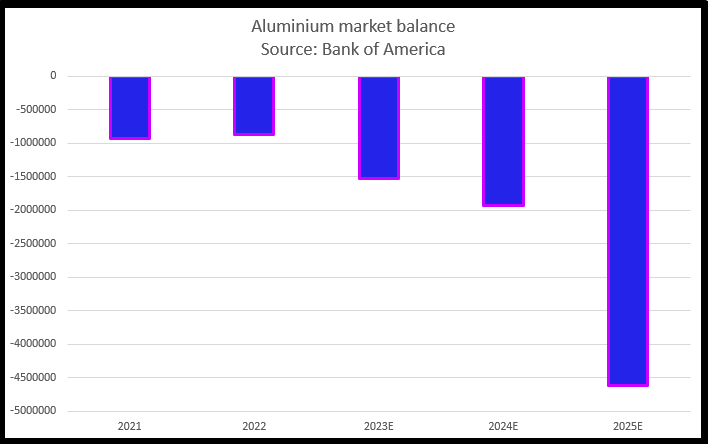

Widmer expects an aluminum market deficit of 1.53 million tonnes this year and a shortage of 1.93 million tonnes next.

Meanwhile, in Europe, lower power prices have helped to reduce production costs, but smelter restarts are limited.

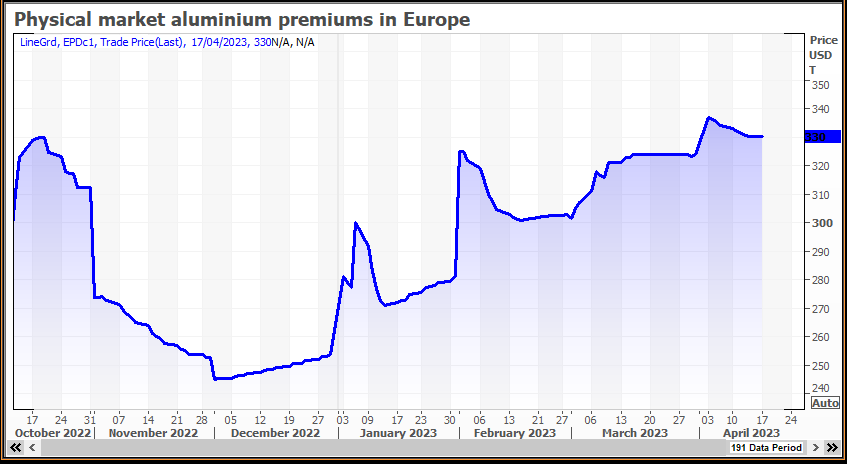

A scramble for supplies has since mid-January fuelled a 20% jump in the duty-paid aluminum premiums buyers in Europe pay in the physical market – above the LME price – to $330 a tonne.

“Physical premiums managed to hold up in Europe where supply constraints remain following the large smelter cuts last year and Russian metal being diverted to Asia,” Macquarie analysts said in a note.

“Given more Russian metal is expected to flow to China, there should be fundamental support for physical premiums.”

Macquarie forecasts an aluminum market deficit of 670,000 tonnes this year and global consumption at 70.8 million tonnes.

(By Pratima Desai; Editing by Mark Potter)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments