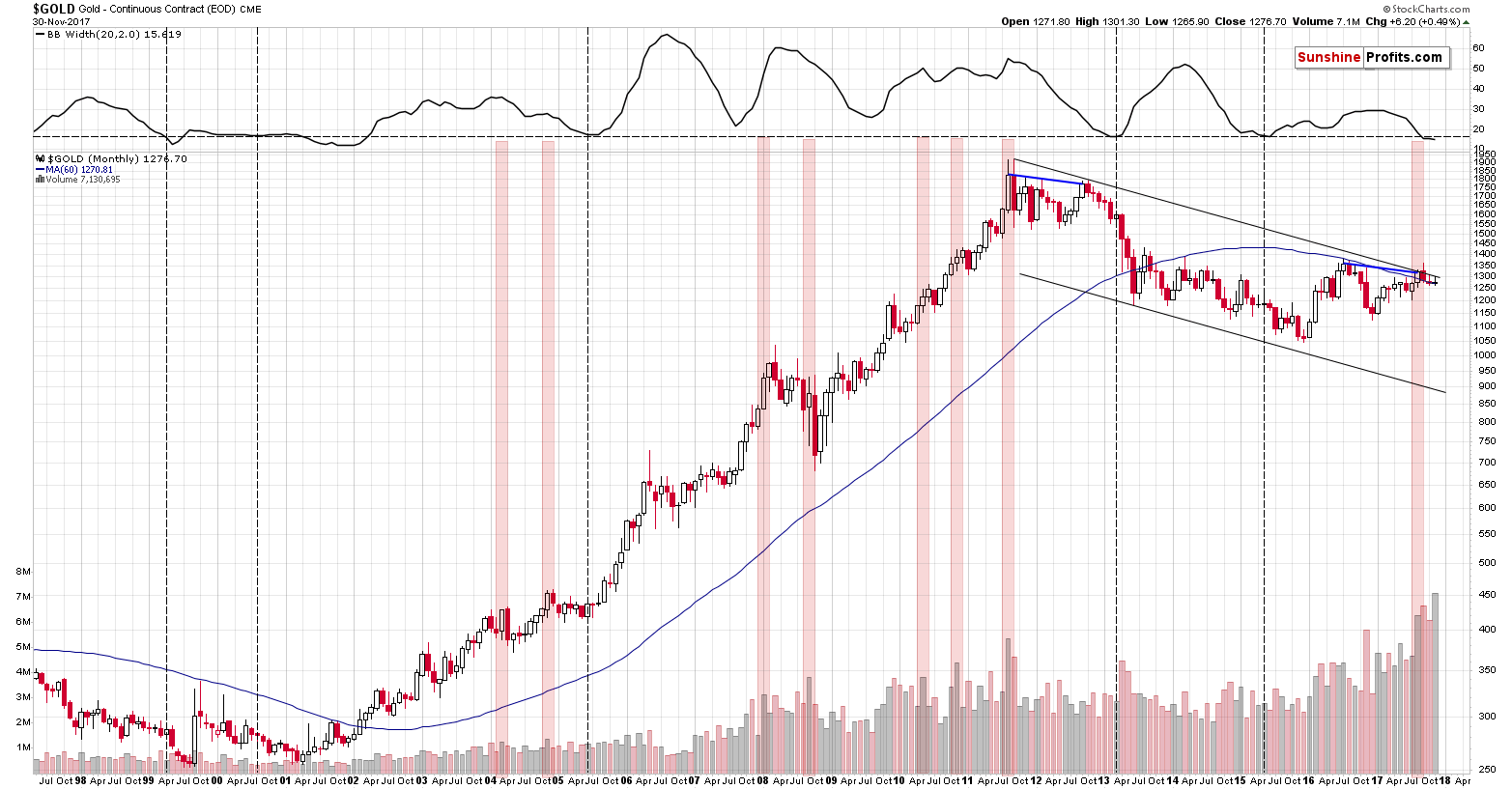

Gold’s record-breaking monthly volume

November turned out to be an up-month in gold and the analogy to what happened in late 2012 is no longer crystal clear. Moreover, gold’s monthly upswing was accompanied by extreme, record-breaking volume. What can we infer from the latter? Will we see a breakout shortly?

In our opinion, that’s highly unlikely. Let’s move right into gold’s long-term chart – it will be easier to discuss the above issues with the price moves in front of us.

Charts courtesy of StockCharts

Before we move to the details, let’s recall what we wrote about two weeks ago on gold’s big yearly volume:

We were asked to comment on the fact that the yearly volume in gold in 2016 was huge (even bigger than the one from 2011) and that the volume in gold so far this year is already bigger than in 2016. In particular, the question is if this is bullish, as both 2016 and 2017 were years when gold rallied. After all, an upswing on big volume is generally a bullish sign. (…)

In short, it doesn’t seem that it’s an important factor for the gold market’s outlook. It’s not even clear that it’s bullish at all.

The reason is provided by the context and there are multiple factors that make any bullish implications rather irrelevant:

1. The volume was high in 2016 and 2017 and so was the price, but if we consider the starting and ending price of 2016 (and the intra-year high) and we consider the same for this year (taking the current price instead of the yearly closing price), we’ll see that the yearly performance is not a clear rally (a big bright candlestick on a yearly candlestick chart) – it’s a… reversal, especially in the case of 2016. In 2016 gold rallied from $1,060 to $1,377 only to close the year at about $1,152, invalidating most of the rally. Huge volume confirms the bearish implications of reversals, so the implications here are bearish rather than bullish. By the way, the months with the highest volume in both 2016 and 2017 were the ones when gold declined.

2. Gold’s increase in yearly volume in terms of futures is not confirmed by yearly volume levels for the GLD ETF (this applies also to other precious metals ETFs, for instance PHYS and for the Central Fund of Canada). Yes, the volume for 2016 was higher than for 2015, but not as high as it was in 2010 or 2011. The 2017 performance is also far from spectacular – it appears that the 2017 volume for the GLD ETF will be lower than in 2016. Consequently, it could be the case that the increase in the gold futures’ volume is not suggesting anything very bullish for the gold market, but it simply shows an increase in the interest in the futures market. The following points seem to confirm it.

3. Gold is not the only market where the futures volume moved to record highs. The same is the case with crude oil and copper. Why are the commodity futures’ volume soaring, but not the one for the GLD ETF? Because the likely common denominator is not the performance of gold, but the interest in the futures market.

4. When gold futures’ volume previous increased substantially it meant that bigger declines were to be seen in the following months – this happened in 2008 and 2011. So, why would the move above the previous highs in the volume levels mean something else than a bigger decline this time? “This time is different” is often a costly phrase.

All in all, it doesn’t seem that the increase in the volume levels in the gold futures market is significant and it’s definitely not something to be viewed as bullish.

Just like the entire yearly “rally” and volume that we described above, gold’s price in November is a rally only theoretically (after all, gold ended the month $6 higher, so by definition it was a rally). In practice, gold rallied $31 and then declined $25, which is not really a rally, but a reversal. If it’s a reversal, then the huge volume that we saw is a major bearish confirmation, not a bullish one.

Having discussed the huge-volume “rally”, let’s discuss the analogy to the 2012-2013 decline. This analogy is something that we first described to our subscribers on September 1 and that we revealed publicly about 3 weeks ago. To make a long story short, based on the similarity in price patterns and similarly low values of the Bollinger Band width that shows lack of volatility, we think that the current price moves in gold resemble the 2012-2013 movement and that a big decline is just around the corner – similar to one that surprised gold bulls in 2013.

To be precise, the September 2012 is similar to August 2017 (highs in terms of monthly closing prices), October 2012 is similar to September 2017 (intraday highs followed by a

move lower before the end of the month), and November 2012 is similar to October 2017 (pause without meaningful changes in terms of monthly closing prices).

However, gold declined in December 2012 and it moved higher in November 2017 – the performance was different, so the question is if the entire analogy was just invalidated. In our view, it doesn’t because of two reasons.

Firstly, the December 2012 decline wasn’t huge and this November’s rally was tiny, so they are not very different and in light of the previous months’ similarity, it would take a big difference (or a few subsequent small differences) to invalidate the analogy.

Secondly, it appears that gold really “wanted to” decline in the last days of November, but it had “bad luck” in terms of a pause and a quick decline in the USD Index. It doesn’t seem that gold impacts the currency moves, but the that the relationship works in the opposite direction – currencies impact gold. Gold usually responds to the USD’s declines with rallies and in the final days of November, gold declined in spite of lower USD prices. That’s a big bearish sign and in light of what we wrote earlier, it strongly suggests that if the USD hadn’t interrupted gold in its plunge, the latter would have been much bigger. If gold’s decline was bigger by at least $6, it would have made November a down month for gold and if the addition to the decline was at least $15 or so (which seems a more realistic expectation in our view), then the analogy would be perfectly confirmed.

Should we view the analogy as invalidated because of a more or less random (in the sense that it’s an external factor from the gold market’s point of view) factor in the final part of the month? It doesn’t seem justified to do so. Gold’s decline continues this month and consequently, it seems that the now-2012 analogy is just as confirmed as if gold had declined last month.

Summing up, November’s reversal in gold and the huge volume that accompanied it seems to have bearish implications, not bullish ones, and the similarity to the pre-2013 slide remains in place. The above bearish implications are strengthened by the fact that gold stocks and silver stocks continue to underperform gold even though the main stock indices have recently soared. There are many other factors suggesting that the big decline in PMs is already underway. Even the following little-known, but important factors confirm it: analogy in the HUI Index, the analogy between the two most recent series of interest rate hikes, and the RSI signal from gold priced in the Japanese yen.

If you’d like to receive follow-ups to the above analysis, we invite you to sign up to our gold newsletter. You’ll receive our articles for free and if you don’t like them, you can unsubscribe in just a few seconds. Sign up today.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief, Gold & Silver Fund Manager

Sunshine Profits – Free Gold Analysis

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski’s, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments