Gold’s bottom could be investors’ lost treasure

Get ready, gold bulls: The precious metal could be close to finding a bottom.

The price of gold fell back below $1,200 an ounce again this week as the U.S. dollar advanced following another federal funds rate hike. It’s now set to log its sixth straight month of declines, its longest losing streak since 1989.

That gold’s not trading below $1,150 is, I believe, remarkable. There’s a lot motivating the bears right now. Besides a stronger dollar and higher interest rate, stocks are still going strong, buoyed by record buybacks and massive inflows into passive investment products. In the week ended September 20, investors poured as much as $34.3 billion into ETFs, taking year-to-date inflows to nearly $215 billion, according to FactSet data.

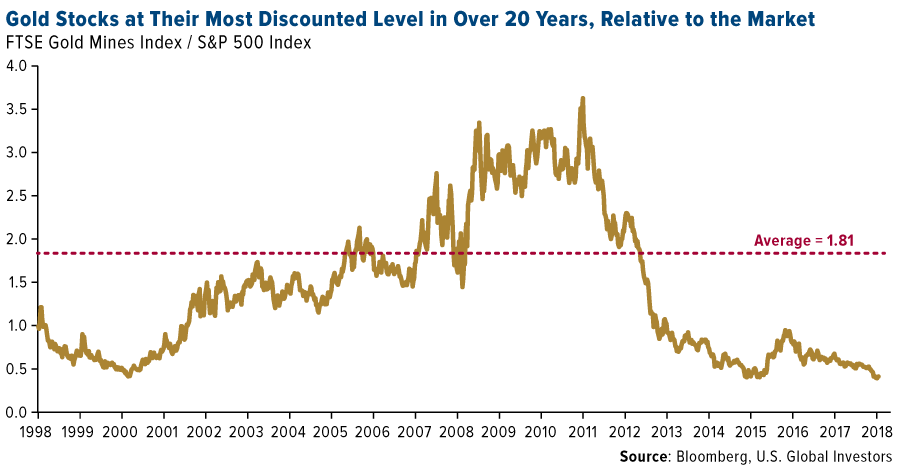

This makes gold mining stocks look especially attractive by comparison. Relative to U.S. blue chips, the FTSE Gold Mines Index is now at its most discounted level in over 20 years.

Gold Industry Ready for Consolidation?

There are other signs that a bottom is near.

For one, Vanguard just restructured its precious metals mutual fund, slashing its exposure to the industry from 80 percent to only 25 percent. This means the world’s largest fund company will no longer offer its investors a way to participate in a potential rally in metals and mining stocks.

The last time Vanguard made a change like this, it coincided with a huge run-up in metal prices. In 2001, gold was just as unloved as it is now, prompting Vanguard to drop the word “Gold” from what was then the Gold and Precious Metals Fund.

Bad move—the precious metal went from under $300 an ounce to as high as $1,900 in September 2011.

This week, mining giants Barrick Gold and Randgold Resources announced an $18 billion merger that, once complete, will create the world’s largest gold producer. An “industry champion for long-term value creation,” according to BMO Capital Markets, the resultant company will “operate five of the 10 ‘tier one’ gold mines on a total cash cost basis and possess numerous projects with potential to” deliver sustainable profitability.

Historically, a telltale sign that an industry has found a bottom is consolidation—just look at the wave of mergers and takeovers in the then-struggling airline industry following the financial crisis.

Other financial firms and analysts also find the Barrick-Randgold news positive—for the two senior producers as well as metals and mining as a whole. Scotiabank believes the merger “improves [Barrick’s] overall asset quality, balance sheet, free cash flow profile, technical expertise and management team, with no takeout premium paid.” The deal, says the Royal Bank of Canada (RBC), “could spur a pick-up in M&As, which in our view could result in a turnaround in mining equity performance.”

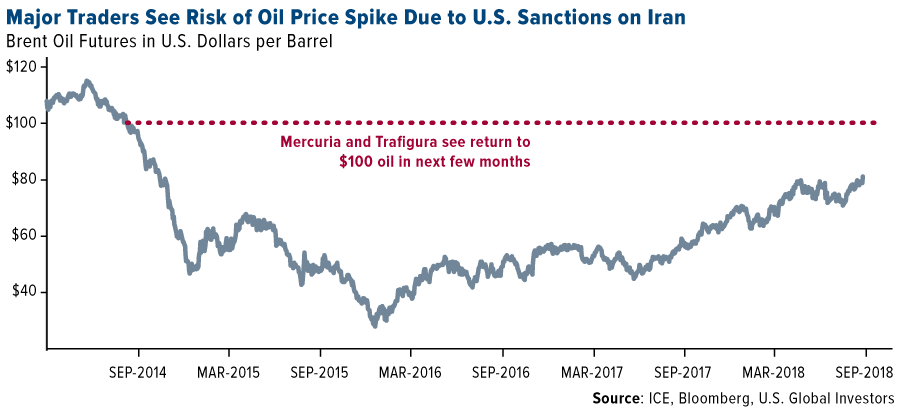

Good news indeed as inflation continues to ramp up. The price of Brent oil, the international benchmark, closed above $80 a barrel this week for the first time since November 2014. That’s an incredible threefold increase from its recent low of $27 a barrel, set in January 2016.

The Incredible Shrinking Stock Market Is Shrinking Even Faster

As you already know, one of the key reasons why gold has been so highly valued for centuries—as a commodity and currency—is its scarcity. It makes up roughly 0.003 parts per million of the earth’s crust. According to the World Gold Council (WGC), an estimated 190,040 metric tons of the stuff have been mined since the beginning of time, leaving only 54,000 metric tons in the ground for producers to dig up, at greater expense.

“Peak gold,” as some experts call it, is a real concern, one that could rocket the price of the yellow metal into the stratosphere on a supply-demand imbalance.

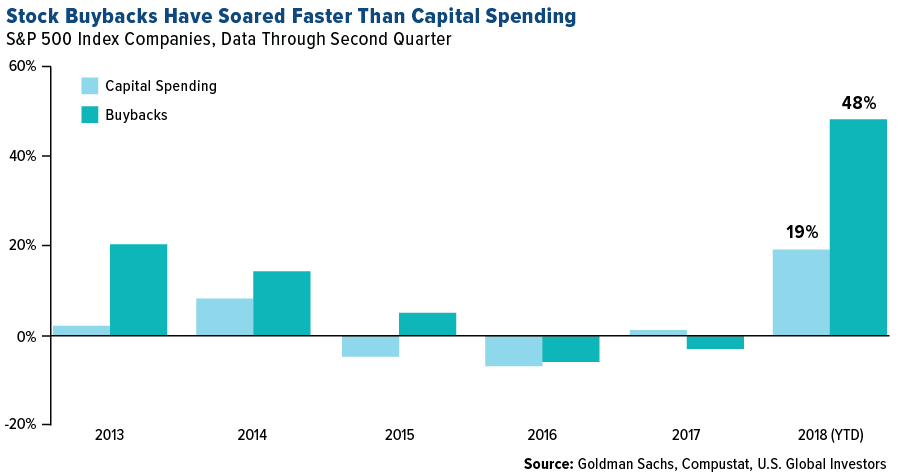

Scarcity, after all, is what’s helping to drive the equity bull market even higher right now. Over the past 20 years, the number of listed companies has steadily been shrinking, mostly as a result of tougher securities regulations. And now, those companies—flush with cash thanks to last year’s corporate tax reform—are buying back their own stock at record and near-record levels.

Just how much? I shared with you recently that in the June quarter alone, S&P 500 companies spent a record $190.6 billion on stock repurchases, an increase of almost 60 percent from the same quarter a year ago. Apple led the pack, taking $21.9 billion worth of stock out of circulation. That’s down slightly from the record $22.8 billion in the first quarter.

In general, Wall Street likes buybacks. Because they lower the number of shares outstanding, earnings per share (EPS) and dividends available per share increase even when there isn’t any profit growth.

But there are a couple of issues. First, buybacks require capital that could have otherwise been spent on investing, upgrading equipment, giving workers raises and the like. For the first time in 10 years, according to Goldman Sachs, buybacks have outstripped capital spending so far in 2018. The S&P 500 is already trading at overinflated prices, meaning companies like Apple are buying high.

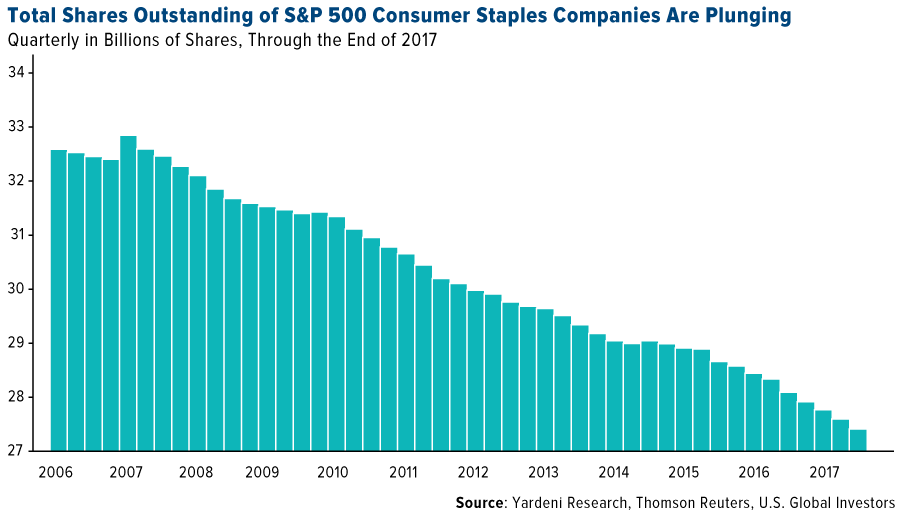

Second, buybacks take shares off the market. Over the past decade, companies have bought back $4.4 trillion as historically low interest rates created, for some, a more favorable environment to float debt instead of equity. Below, I chose to highlight the consumer staples sector because the decline in shares since 2006 has been so dramatic, falling from around 32.5 billion shares to 27.5 billion shares—a decrease of more than 15 percent.

Today, “not enough shares are being issued to offset those being withdrawn from circulation,” according to Reuters. Net equity supply turned negative for the first time ever in 2016, and it could end in negative territory again by the end of this year.

Coupled with the ticking passive index bomb I wrote about earlier in the month, fundamental investing is changing. It’s hard to say where this will end—when there’s only one share of Apple left? Prices would explode, and investing would become even more out-of-reach for many than it already is today.

Click here to get my thoughts on why I think the market could correct between 10 percent and 20 percent early next year, and what investors can do now to prepare!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 1.07 percent. The S&P 500 Stock Index fell 0.54 percent, while the Nasdaq Composite climbed 0.74 percent. The Russell 2000 small capitalization index lost 0.92 percent this week.

- The Hang Seng Composite lost 1.23 percent this week; while Taiwan was up 0.31 percent and the KOSPI rose 0.17 percent.

- The 10-year Treasury bond yield fell 0.2 basis points to 3.062 percent.

Domestic Equity Market

Strengths

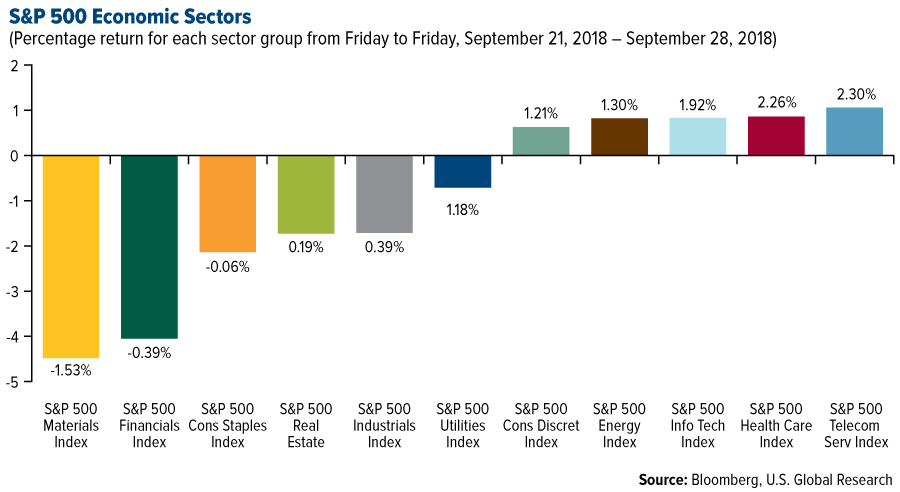

- Communication services was the best performing sector of the week, increasing by 1.06 percent versus an overall decrease of 0.61 percent for the S&P 500.

- Abiomed was the best performing stock for the week, increasing 16.85 percent.

- SurveyMonkey soared in its trading debut. The survey provider priced its initial public offering at $12 a share, and ended its first day of trading at $17.24, up 43.7 percent.

Weaknesses

- Materials was the worst performing sector for the week, decreasing by 4.48 percent versus an overall decrease of 0.61 percent for the S&P 500.

- Smith (A.0.) Corp was the worst performing stock for the week, falling 10.63 percent.

- Global mergers and acquisitions dropped to $783 billion in the third quarter, down 35 percent from the prior quarter. The escalating trade dispute between the United States and China has cast a shadow on the financial and regulatory prospects of many deals.

Opportunities

- Chinese startup Bytedance is said to be raising new funding at a mega valuation of $75 billion. The deal, thought to be led by backers including SoftBank, would make the firm the most valuable startup in the world.

- Britain’s biotechnology industry has raised a whopping $2.05 billion in the first eight months of this year, surpassing the entire amount raised in the whole of 2017, despite anxiety in the sector about the fallout from Brexit. The increase has been fueled by recent changes to venture capital tax incentives, according to UK BioIndustry Association CEO Steve Bates, as well as global investor enthusiasm for drug discoveries emanating from biotech labs.

- Masayoshi Son, CEO of SoftBank, said the company plans to raise another $100 billion to invest in startups every few years. Son told Bloomberg he plans to spend around $50 billion a year making bets on startups.

Threats

- The Securities and Exchange Commission is suing Tesla CEO Elon Musk on charges that he made “false and misleading statements” and wants to bar him from helming a public company. The SEC says the charges stem from Musk’s tweets about taking his electric car company private at $420 a share, a claim he tweeted to his 22 million followers on August 7. Tesla shares fell more than 11 percent on the news.

- Ryanair is bracing for another strike by staff as walkouts in six European countries force flight cancellations that will disrupt the plans of more than 40,000 travelers. Europe’s largest low-cost carrier has faced a string of strikes since it recognized trade unions for the first time in December, damaging bookings and forcing it to consider cutting short-term growth plans if labor unrest continues.

- Macquarie Bank CEO Nicholas Moore has been implicated in a financial investigation by German authorities. The inquiry concerns a complex dividend trading scheme that is currently the subject of civil litigation. In a statement to the ASX, Macquarie said the Cologne Prosecutor’s Office is expected to speak with at least 30 senior staff members involved in the deal.

The Economy and Bond Market

Strengths

- The U.S. economy expanded at a strong pace in the second quarter, with growth expected to pull back slightly this coming quarter but still continue its solid run. GDP rose at a 4.2 percent seasonally and inflation-adjusted annual rate in the second quarter, the Commerce Department said Thursday, which matched its August estimate. Gains in consumer spending, net exports and business investment led to the strong growth.

- The Federal Reserve hiked its benchmark interest rate this week and upped its estimate for economic growth this year and next. In addition, it provided a road map of what lies ahead through 2021. As widely anticipated, the rate was increased 25 basis points which takes the rate to a range of 2 percent to 2.25 percent, where it last was in April 2008. This is the eighth increase since the Fed began normalizing policy in December 2015.

- Consumer sentiment was just under expectations in the final reading of September although remaining near all-time high levels. The University of Michigan’s monthly survey of consumers hit 100.1 in the final reading of September, below the 100.8 expected from economists polled by Reuters. Sentiment among consumers rose from August’s final reading, when sentiment hit 96.2. “Consumer sentiment remained at very favorable levels in September, with the Index topping 100.0 for only the third time since January 2004,” Richard Curtin, chief economist for The University of Michigan’s survey, said in a statement.

Weaknesses

- The MNI Chicago Business Barometer, also known as Chicago PMI, fell to a five-month low of 60.4 in September, down 3.2 points from August’s 63.6. Moderations in both output and new orders, alongside weaker hiring sentiment, were accountable for the Barometer’s decline, MNI said.

- U.S. consumer spending withdrew slightly in August from the strong pace of growth in the spring. Household spending rose 0.3 percent in August from July, the Commerce Department said Friday. August’s gain was the smallest since February, marking a modest pullback from a 0.4 percent increase in both June and July, and 0.5 percent rises in April and May.

- The number of Americans filing for unemployment benefits increased more than expected last week, likely as Hurricane Florence temporarily displaced some workers. Initial claims for state unemployment benefits rose 12,000 to a seasonally-adjusted level of 214,000 for the week ended September 22, the Labor Department reported. Economists polled by Reuters had forecast claims rising to 210,000 in the latest week.

Opportunities

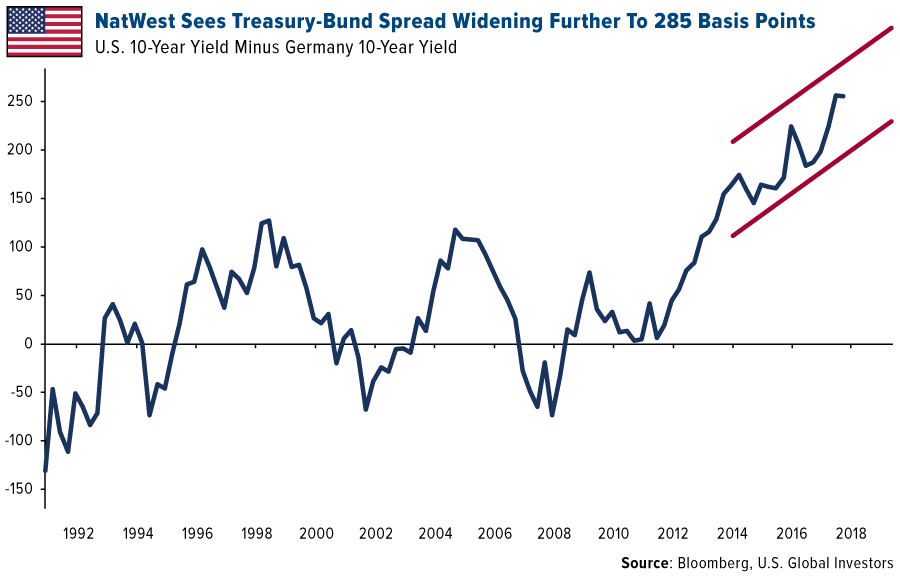

- The yield premium on 10-year Treasuries over German bunds hit a record high last week, spurred by the prospect that the Federal Reserve will further lift interest rates. That has prompted Andrew Roberts, head strategist at NatWest Markets, to raise his target for the spread to 285 basis points from 265 previously. The widening has been driven by an increase in Treasury yields.

- Next Friday, average hourly earnings are projected to have risen by 3.0 percent year-on-year in September, which would mark the fastest rate in nine years.

- Also on Friday, the jobless rate is expected to inch lower by 0.1 percentage points to 3.8 percent, signaling further tightening in the labor market.

Threats

- Next Friday, the U.S. economy is forecast to have added 188,000 jobs in September, somewhat less than the 201,000 gains seen in the prior month. If the jobs report fails to excite the markets, it could lead to turmoil.

- After a surprise surge in August, the ISM manufacturing PMI is expected to ease marginally in September when released on Monday. The ISM’s non-manufacturing PMI will follow on Wednesday and is also forecast for a slight drop in September.

- Trade-related headlines will keep investors on edge, especially if there are any developments in the negotiations with China and Canada.

Gold Market

This week spot gold closed at $1,192.50 down $6.50 per ounce, or 0.54 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.36 percent. Junior-tiered stocks slightly underperformed seniors for the week, as the S&P/TSX Venture Index came in off 1.49 percent. The U.S. Trade-Weighted Dollar Index rose 1.03 percent for the week.

| Date | Event | Survey | Actual | Prior |

| Sep-25 | Conf. Board Consumer Confidence | 132.1 | 138.4 | 134.7 |

| Sep-25 | New Home Sales | 630k | 629k | 608k |

| Sep-26 | FOMC Rate Decision (Upper Bound) | 2.25% | 2.25% | 2.00% |

| Sep-27 | Hong Kong Exports YoY | 8.3% | 13.1% | 10.0% |

| Sep-27 | Germany CPI YoY | 2.0% | 2.3% | 2.0% |

| Sep-27 | GDP Annualized QoQ | 4.2% | 4.2% | 4.2% |

| Sep-27 | Durable Goods Orders | 2.0% | 4.5% | -1.7% |

| Sep-27 | Initial Jobless Claims | 210k | 214k | 202k |

| Sep-28 | Eurozone CPI Core YoY | 1.1% | 0.9% | 1.0% |

| Sep-29 | Caixin China PMI Mfg | 50.5 | — | 50.6 |

| Oct-1 | ISM Manufacturing | 60.0 | — | 61.3 |

| Oct-3 | ADP Employment Change | 185k | — | 163k |

| Oct-4 | Initial Jobless Claims | 210k | — | 214k |

| Oct-4 | Durable Goods Orders | — | — | 4.5% |

| Oct-5 | Change in Nonfarm Payrolls | 185k | — | 201k |

Strengths

- The best performing metal this week was silver, up 2.89 percent as traders loaded up on almost 10 million ounces in a span of one minute on Friday. Gold traders and analysts are bullish on the yellow metal for a sixth straight week, as measured by Bloomberg’s weekly survey, even as gold heads for its sixth month of losses.

- Jewelry stocks in India performed well this week after unexpected news that import duties will not be raised on gold. Sandeep Kulhalli, vice president at Titan, a jewelry company, said that “by keeping the duties at the same level, the customer sentiment toward gold buying will be positive during the festive season.” As gold prices fall to six-week lows, physical demand saw an uptick in China, the world’s largest consumer of the precious metal. Peter Fung, head of dealing at Wing Fung Precious Metals in Hong Kong, told Reuters that “cheaper gold prices led to increased buying in both Hong Kong and China. Shanghai premiums increased on Friday, reflecting higher demand.”

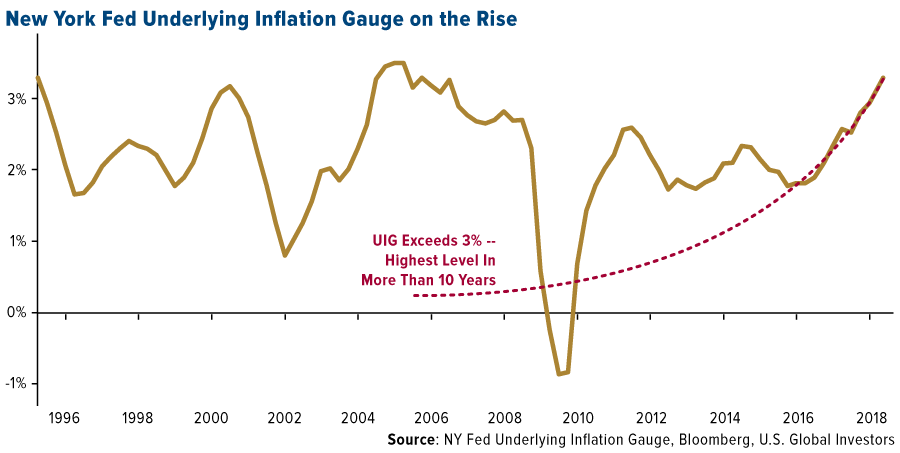

- Inflation in Germany unexpectedly rose to a four-month high, suggesting that the interest rate in the eurozone will rise further above the European Central Bank’s target, reports Bloomberg. Consumer prices rose to 2.2 percent this month, exceeding the 1.9 percent level in August, driven by rising energy costs. U.S. inflation also continues to rise. The Federal Reserve Bank of New York notes that the gauge detects cyclical turning points in underlying inflation and has a better track record than the consumer price series. As of June 30, the gauge was at 3.33 percent, above the current generic 10-year Treasury yield of 3.06 percent.

Weaknesses

- The worst performing metal this week was platinum, down 1.32 percent as HSBC forecast an ongoing surplus for the metal. Gold fell below $1,190 on Thursday, continuing its sixth straight month of losses. According to Bloomberg, the U.S. dollar strengthened this week, causing gold futures to fall to their lowest level in six weeks, after a rise in U.S. durable goods orders. Should this trend carry on, the yellow metal will hit its longest losing streak in 30 years.

- Sibanye Gold’s two largest unions are on strike over pay after prior wage talks in July failed to reach an agreement. Thousands of South African job cuts have resulted in the lowest number of mining-industry jobs since 2009, creating a highly charged atmosphere for these negotiations. The situation currently remains unresolved, while other unions came to agreements with South African mining companies last week.

- Continental Gold lost three employees at its Berlin Project in Colombia following an attack by former members of the Revolutionary Armed Forces of Colombia (FARC). In addition to the geologists who were fatally wounded, several other workers were injured. West African gold miners were similarly impacted after a roadside bomb killed eight soldiers in Burkina Faso. These attacks highlight the potential dangers miners and companies face by operating in regions with a prevalence of violence.

Opportunities

- Barron’s Andrew Bary writes this week that the out-of-favored gold now deserves a place in investment portfolios. Compared with stocks and other financial assets, gold appears to be inexpensive and gold stocks are at their most discounted level in over 20 years relatively. Keith Trauner, co-portfolio manager of the GoodHaven mutual fund, says that “virtually every government in the world is trying to promote inflation partly because there is so much sovereign debt” and with so much debt governments have only three choices: default, restructure or inflate the currency. Trauner notes that most governments will choose inflation, which has historically been positive for the price of gold. Central banks have purchased a total of 264 metric tons of gold so far this year to reach the highest level in six years.

- Several mergers and acquisitions have been announced this week in the mining space. Bonterra Resources has completed its acquisition of Metanor Resources solidifying a strategic step in acquiring the only permitted mill in the Urban-Barry gold camp. Kirkland Lake Gold announced that as a result of the above acquisition, they now own a 9.44 percent interest in Bonterra. Great Panther Silver has entered into a scheme implementation deed with Beadell Resources, which will acquire a 100 percent stake in Beadell’s Tucano gold mine in Brazil. The mine is expected to produce around 130,000 ounces of gold in 2018. Gold giants Barrick Gold Corp and Randgold Resources announced their merger, which will create the world’s largest gold mining company. Mark Bristow is set to become the CEO of newly combined company. Barrick also entered into a $300 million mutual investment agreement with Shandong Gold, China’s largest producer, which will further strengthen the relationship between the two miners.

- At the Precious Metals Summit in Colorado last week, RBC’s panel of global research and sales, announced their top stock picks for the year. Those names include Tristar Gold, Regulus Resources, Sunshine Silver, Dolly Varden, Oklo Resources, Maverix Metals and GT Gold. The event was attended by a large number of corporate development teams, especially more senior miners who are on the hunt for new assets to add to their portfolio.

Threats

- Although many central banks are gobbling up gold, Turkey continues to sell its gold. The Central Bank of Turkey saw gold reserves fall 16.1 percent, or 83.5 tons, from August to September. Then, reserves fell $821 million from last week to this week. Turkey’s economy continues to experience turbulence as the lira has plummeted so far this year.

- 10-year Treasury yields turned negative for European buyers this week due to mounting costs to convert payments from euros into dollars. Bloomberg writes that the three-month cross-currency basis dropped to minus 40 basis points overnight, from about minus 16 points on Wednesday, marking the biggest single-day decline since 2009. A similar change happened for Japanese-based investors. Three-month yen cross-currency basis swaps fell to minus 54 basis points on Thursday, and as a result, 10-year Treasuries now yield minus 0.08 percent for hedged Japanese buyers. This could result in fewer buyers of U.S. debt. Stan Druckenmiller, billionaire investor, joins a growing list of investors who have predicted that our massive debts will trigger the next financial crisis.

- Marko Kolanovic of JPMorgan Chase & Co. says that a backlash could be brewing again the U.S. dollar as other countries look to weaken the dollar’s hold over the global financial system. In speaking with Bloomberg, Kolanovic says that “with the current U.S. administration policies of unilateralism, trade wars, and sanctions increasingly affecting both friends and foes, the question arises whether the rest of the world should diversify away from the risks of the U.S. dollar and dollar-centric finance.” The International Monetary Fund released its quarterly report on Friday showing that the dollar’s share of global reserves has fallen for the sixth straight quarter to the lowest since 2013. Gold tends to benefit from a weaker dollar and appears to be cheap, according to JPMorgan. Global trade is continuing to lose some steam amid the tariff battle between the U.S. and China, according to Bloomberg. Freight and logistics company DHL said that its trade indicator fell this month to the lowest level since 2016 and indicated a slower pace of growth in the coming months.

Blockchain and Digital Currencies

Strengths

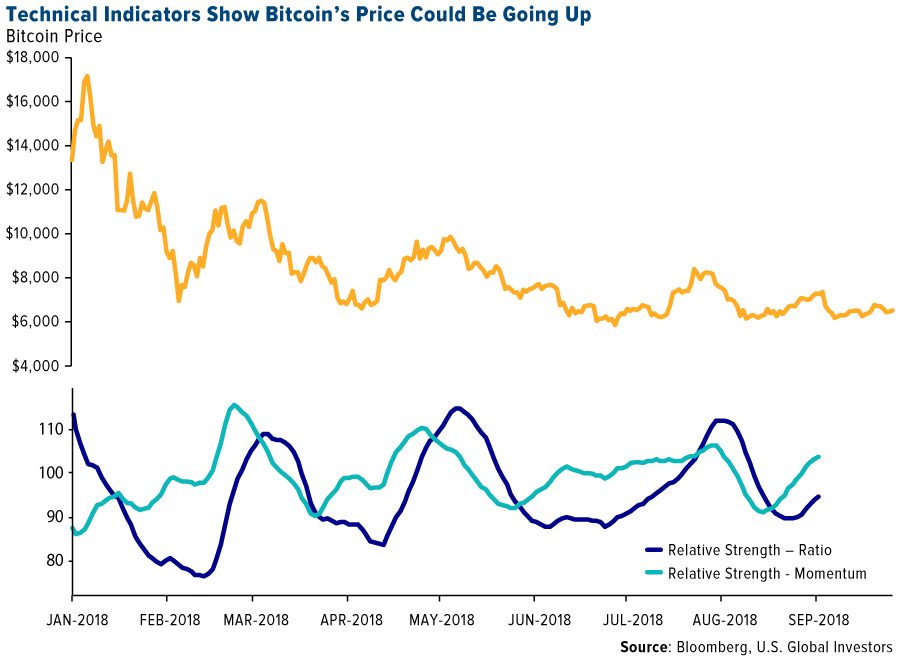

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 28 was Eternal Token, which gained 943.93 percent. Based on an analysis of RIG trend lines, bitcoin bulls are looking at a leading technical indicator in hopes that bitcoin reverses course from its recent slump. The indicator, which is a combination of RSI and momentum studies, crossed the relative strength index (RSI) gauge. As Bloomberg reports, bitcoin’s price rose the past three times the two gauges crossed.

- Circle, the cryptocurrency finance company backed by Goldman Sachs, announced that it has gone live with its stablecoin called the USD Coin (USDC), reports MarketWatch. It will run on an open-sourced consortium, meaning there is no single issuer, creating openness and interoperability, according to Circle. Jeremy Allaire, founder and CEO of Circle, stated that more than 20 companies, including wallets, exchanges and software applications will announce or launch support for USDC, the article continues.

- The largest digital currency mining company in the world, Bitmain, released its first public financial statements to the Hong Kong Stock Exchange this week, reports MarketWatch. Bitmain reported $2.8 billion in revenue in the six months ending June 2018, according to the financial statement, which is an increase of 10-fold since the same time frame in 2017. The Beijing-backed company also confirmed its plans to go public.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended September 28 was VeriME, which lost 56.02 percent. Many users remain confused about how cryptocurrencies are viewed by the U.S. Internal Revenue Service (IRS) and, as a result, are not properly reporting their holdings for taxation, according to News BTC. Only around 800 individuals reported holding digital currencies between 2013 and 2015, which is suspect given that Bitcoin rose from $13 to $430 during that period. “A lot of people treat Bitcoin as cash, or the same as Apple Pay,” explained Sarah-Jane Morin, a partner at Morgan Lewis & Bockius. Bitcoin is considered a commodity by the IRS and, as such, gains and losses must be reported on every transaction. For those who have not properly tracked their transactions up to this point, Mortin warns against playing the “audit lottery,” instead encouraging users to make their “best effort” to report gains and losses.

- Nobuaki Kobayashi, an attorney and bankruptcy trustee in Tokyo, recently offloaded 25.98 billion yen ($230 million) of bitcoin and Bitcoin Cash, potentially contributing to a recent price drop. Charged with liquidating the defunct exchange, Mt. Gox Kobayashi also sold $400 million worth of bitcoin at once in March. While creditors who expect to be repaid in fiat currency may appreciate these sell-offs, cryptocurrency investors are concerned about whether other, bigger Mt. Gox trustee-related sell-offs are on the horizon.

- Monero, a coin intended to add an additional level of anonymity for users, was found to have “a burning bug” in its code, which could potentially allow hackers to steal funds from crypto exchanges, according to News BTC. This bug has since been patched; however, concern remains about such a major vulnerability going undetected for as long as it did. Bigger exchanges with more to lose may be hesitant to trust this smaller coin.

Opportunities

- Google announced the reversal of part of its cryptocurrency ad ban that was implemented back in March. Now, regulated crypto exchanges will be allowed to buy ads in the U.S. and Japan, while initial coin offerings (ICOs), wallets and trading advice remain banned for advertisement, reports Seeking Alpha.

- The Financial Action Task Force (FATF) is expected to release a global set of anti-money laundering (AML) standards for cryptocurrencies in October. Marshall Billingslea, president of FATF, admits that current AML standards are “very much a patchwork quilt or spotty process.” The previous, non-binding FATF resolutions were approved in June 2015. According to Cointelegraph, FATF began developing the revised, binding AML rules in June of this year. Once the “gaps” in global AML standards are closed and the new regulations are uniformly applied, Billingslea thinks digital currencies will be “a great opportunity.”

- AT&T is the latest major corporation to launch a suite of blockchain services targeting diverse industries, writes Coindesk.com. On Wednesday the world’s largest telecommunications firm stated in a news release that these new blockchain solutions will be largely focused on supply chain processes, and can help businesses automate and digitalize processes.

Threats

- According to financial intelligence analysts from Washington D.C., North Korea appears to be evading U.S. sanctions using cryptocurrencies, reports News BTC. The country is also allegedly developing its own “native crypto asset to further assist moving money across borders,” the article reads. The analysts explain the way North Korea would use a “mixer” of cryptos in such a way to cover its tracks, which includes sending the same kind of digital currency back to its original source.

- A new report from research firm Diar shows that if you live in the U.S. or do business here, the government is most likely tracking your cryptocurrency transactions. In the report, which cites public records, the group notes that U.S. government agencies have spent $5.7 million hiring contractors that perform blockchain analysis, reports CCN.com, which means linking an individual’s identity to their crypto funds. But what about the tools or coins that tout anonymity for its users? “The vast majority of cryptocurrency users leave enough of a trail that, equipped with the right tools, investigators can determine to whom a particular wallet belongs,” the article reads.

- The Securities and Exchange Commission (SEC), which previously shut down PlexCoin’s crypto scheme, is now seeking further action against its founders, reports Coindesk.com. “The SEC submitted a document to the New York Eastern Court on Tuesday, requesting to file a motion for sanctions against the two founders, Dominic Lacroix and Sabrina Paradis-Royer,” the article reads. According to the submission, the two PlexCoin founders had been ignoring earlier court orders regarding both accounting and repatriation of assets, as well as evidence discovery.

Energy and Natural Resources Market

Strengths

- With three quarters under our belts, crude oil is leading the commodities scorecard, rising 23.7 percent year-to-date. The commodity has outperformed as a result of better-than-expected supply curtailments out of the Organization of the Petroleum Exporting Countries (OPEC) and Russia. Additionally, the re-imposition of U.S. sanctions on Iran, which has taken 2 million barrels of exports offline, has allowed the U.S. to greatly expand its exports without upending the global market balance.

- The best performing sector for the last three quarters was the S&P 1500 Oil & Gas Refining and Marketing Index. The index rose 21.7 percent, benefitting from greater crack spreads as landlocked U.S. and Canadian crude was available at greater discounts. The demand side also delivered a new gasoline all-time consumption record over the peak summer driving season.

- The best performing major natural resource stock for the same period was Ecopetrol SA. The Colombian integrated oil and gas producer and refiner rose 84.1 percent. The company outperformed on three fronts: greater political stability following the presidential election in Colombia, a new long-term labor agreement with its union and the ramp up in margins expected from the introduction of its revamped refinery unit after a decade-long upgrade process.

Weaknesses

- Lumber is the worst performing commodity so far in 2018. The commodity dropped 23.1 percent, mainly over the past three months, amid mounting concerns on the U.S. housing sector. U.S. housing data has turned negative this year as a result of higher mortgage rates and increased raw materials costs.

- The worst performing sector year-to-date was the NYSE Arca Gold Miners Index. The index dropped 20.8 percent, tracking the decline in gold prices which have been the major casualty of the trade war-led rally in the U.S. dollar.

- The worst performing stock for the period was Freeport-McMoRan Inc. The Arizona-based producer of base and precious metals dropped 26.6 percent. The stock has suffered from a decline in the prices of both copper and gold, while attempting to finalize its negotiations with the Indonesian government over its share in its cornerstone asset, the Grasberg mine, which owns the title as the largest gold mine and second largest copper mine in the world.

Opportunities

- Some oil traders expect to see $100 crude coming as suppliers struggle to fill the Iran gap. “The market does not have the supply response for a potential disappearance of 2 million barrels a day,” said Mercuria Energy Group co-founder Daniel Jaeggi. The U.S. announced plans in May to reimpose sanctions on Iran’s oil exports and is “incredibly serious” about its measures, said Trafigura Group co-head of oil trading Ben Luckock.

- Supply tightness in the spot metals market continues as Zinc spot premiums rise to near 2-year highs. Premiums for zinc deliveries in Shanghai rose sharply as inventories have dropped 79 percent since peaking in March. The rise in spot premiums suggests major industrial users of the metal are pre-purchasing material ahead of what could turn to be a major rally in metals into the peak seasonal demand period of the Chinese New Year.

- The Federal Reserve may slow down the pace of rate hikes, decelerating the rally in real rates and the U.S. dollar. In his testimony, Federal Reserve Chairman Jerome Powell guided toward a more cautious approach as rates get closer to a 3 percent neutral level, suggesting we may only see two or three rate hikes next year. A slower rate hiking cycle should weigh on the U.S. dollar and, conversely, should provide a boost to commodities and risk sectors such as energy and materials.

Threats

- Six months after Trump’s claim “trade wars are good, and easy to win,” investors watched the fallout this week after the U.S. levied tariffs on second round of goods, according to Bloomberg. China dashed prospects for a resolution, warning Trump his threats of further tariffs are blocking any potential talks, suggesting the conflict may well drag on toward the U.S. midterms in November.

- The unrelenting rise of U.S. crude production could add pressure to West Texas Intermediate (WTI) prices and widen the differential to Brent. The rapid increase in volumes has put pressure on crude export infrastructure, increasing midstream costs, thus lowering the net revenue received by producers. The Energy Information Administration (EIA) reported U.S. crude production hit fresh records of 11.1 million barrels per day, making the U.S. the largest global producer ahead of Russia and Saudi Arabia.

- The latest U.S. refinery data is bearish as total commercial inventories rise above the seasonal norm. With fall refinery maintenance season well underway, refined product inventories should be dropping. Instead, they have been increasing, implying lower commercial demand for fuel and distillates as the summer peak driving season wrapped up.

China Region

Strengths

- Singapore’s Straits Times Total Return Index notched a 1.27 percent gain for the week, while Vietnam’s Ho Chi Minh Stock Index rose 1.42 percent in the same time.

- Energy was the top-performing sector for the week in Hong Kong’s Hang Seng Composite Index, rising 4.66 percent as Brent crude oil prices moved to new 52-week highs.

- Vietnam’s economy expanded 6.98 percent in the third quarter from a year ago, essentially in line with estimates of 7.01 percent growth.

Weaknesses

- The Hang Seng Composite Index dropped 1.23 percent for the week, while the Philippines’ Stock Exchange Index fell 1.44 percent and India’s SENSEX and NIFTY Indices fell 1.67 and 1.91 percent, respectively.

- Properties & Construction dropped 4.70 percent for the week, while Consumer Services and Information Technology fell 3.53 and 3.01 percent, respectively.

- Thailand’s exports reading for the August measurement period were up only 5.8 percent, down from July’s 8.3 percent growth rate.

Opportunities

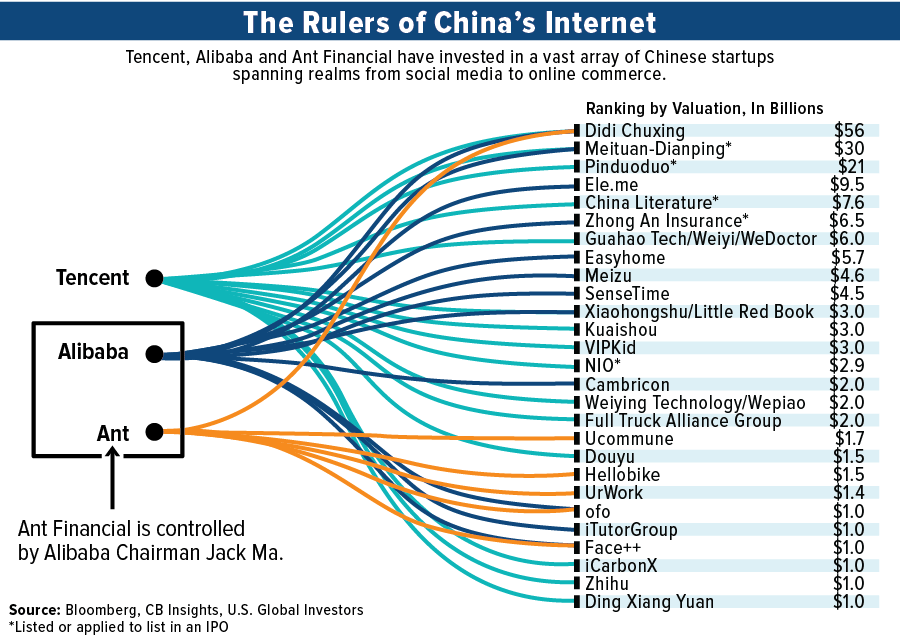

- Move over, Uber et al. Have you heard of Bytedance? This Chinese startup is potentially holding the crown for the world’s most valuable, at a whopping $75 billion valuation, according to a recent Bloomberg News report. The news-aggregation-powered-by-artificial-intelligence-turned-search-and-social-media-like business has—impressively—the article observes, come this far without taking money from either Tencent or Alibaba.

- But speaking of startups, take a gander at this beauty of a chart, mapping out a web of connections and investments from those two well-known Chinese tech juggernauts into numerous startups, like so many unicorn eggs placed amid so many different baskets, or something like that. Just look at the chart. Look, Ma, a unicorn farm!

- FTSE Russell announced plans to begin including Chinese A-shares in its major benchmarks commencing June of 2019 and phasing in through March of 2020, drawing billions more in investment dollars toward the Chinese mainland equity markets and continuing internationalization of the renminbi.

Threats

- Trade war concerns remain central, although rhetoric will likely quiet down over the upcoming holiday week in China.

- The Chinese yuan is once again just a hair’s breadth away from 6.90.

- Elsewhere in the region, both the Indonesian rupiah and the Philippine peso fell (climbed) to new lows (highs) this week, although the peso did pull back a bit from its lows earlier in the week. Both countries’ central banks raised rates, and Indonesia continues to work to push exporters to keep more money in the country.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 3.9 percent. MOL Hungarian Oil and OTP Bank were the strongest contributors to the outperformance of the Budapest exchange. MOL gained almost 8 percent over the past five days and OTP Bank gained 3.6 percent after stock was upgraded to a “buy” rating by Raiffeisen Centrobank.

- The Turkish lira was the best performing currency this week, gaining 4.1 percent against the U.S. dollar. Turkish President Recep Tayyip Erdogan is in Germany on a state visit. Turkey’s relationship with Germany worsened after the failed coup attempt two years ago that prompted Ankara to react with strong measures, including jailing journalists, soldiers and public servants, including several German citizens.

- Industrials was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1 percent. Economic sentiment dipped during September, falling 3.9 percent to 101.3, after reaching positive values over the past two months. On a positive note, the government announced the further relaxation of capital controls with no restrictions on cash withdrawals from ATMs.

- The Czech koruna was the worst performing currency this week, losing 1.8 percent against the dollar. The central bank raised its benchmark rate to 1.5 percent, but noted that it will be careful of hiking again in the near future.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- The European Union decided to set up a new payment channel that would enable legal trade with Iran without encountering U.S. sanctions. According to the plan, a legal entity will be created to facilitate legitimate financial transactions with Iran, allowing European companies to continue trading with Iran in accordance with the European Union law. They could be open to other global partners as well, said Federica Mogherini, the EU’s foreign policy chief.

- The Czech central bank hiked interest rates on Wednesday for the third time in a row and the sixth time since April 2017, when the cap on the currency was removed. The Czech Republic has a solid rate premium now over the euro-area and a strong economy, making domestic fixed-income markets attractive.

- According to Bloomberg, the U.S. Congress is unlikely to pass any new sanctions on Russia before November, including a proposal that would affect Russia’s sovereign debt and energy projects. With a lack of new sanctions and higher oil prices Russian equites could rally further.

Threats

- Eurozone economic confidence weakened further in September to a15-month low. The economic sentiment index dropped more than expected to 110.9 from 111.6 in August on trade protectionism and political uncertainty. The confidence level was notably revised down in the industry and consumer sectors, only partially offset by an increase in the retail trade and construction sectors.

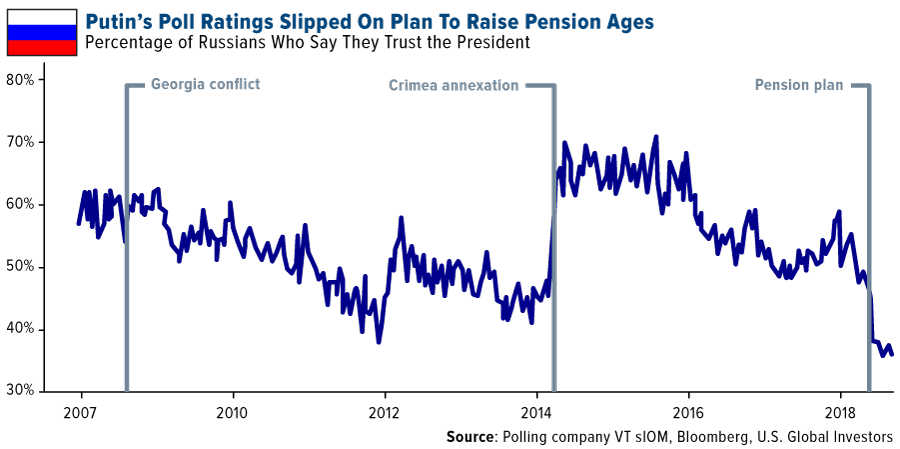

- Current regional elections in Russia show that Vladimir Putin’s United Russia party lost governorships in three regions. Putin’s approval rating slumped to the lowest in more than a decade after the government announced a plan to increase the retirement age for men and women. The unpopular reforms also led to protests earlier this month, with over 1,000 arrested in nearly 40 cities across Russia.

- The Italian government planned to shrink the budget deficit in 2019 to 0.8 percent of the country’s GDP; however, the new administration proposed to run a deficit of 2.4 percent of GDP. This new deficit gap is still below the EU’s requirement of less than 3 percent. However, a higher deficit will make the process of servicing national debt more expensive for Rome, which stands at 130 percent of GDP. Italian banks have been big buyers of local government bonds, and if local bonds go down in value, banks will suffer.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments