Price of gold to head sideways this fall: Casey

What a way to start October. Gold slipped mightily, easily falling through US$1,300 on Oct. 4th to bottom at US$1,269 per oz. before closing the day at US$1,283, down 2.3%. That took it back to pre-Brexit levels, erasing a move that had been consolidating for three months. The next day it lost another US$14.

Silver did even worse. After leading gold the last few months silver fell off a cliff, losing almost US$1.40 to close at US$17.80 per oz., a 7% single-day decline. As is often the case silver has been trading like its cousin gold, only with wilder gyrations – and this move was no exception.

Clearly, the call that the ‘summer correction is over’ and that autumn would be golden is not panning out. So what is the new call?

It’s looking like a sideways season for gold through the rest of the year.

The near-term outlook is fairly bearish, as down spikes rarely occur in isolation. Disappointed longs will sell and anxiety over what’s ahead for gold means a not particularly significant event could catalyze an outsized gold response. Uncertainty over the US election and anxiety over the December rates decision will keep gold capped until those milestones are over.

That being said, there are still a lot of gold bulls out there who will buy into dips, muting the slide. From a chart perspective, there is significant support in the US$1,250-$1,260 level. That is the pre-Brexit support platform and could well represent the new normal for the rest of 2016.

It’s important to note: at US$1,260 per oz. gold is still up 16% this year. Even if it feels like gold’s rise happened ages ago, precious metals have mostly held onto their gains – and those gains were big enough to absorb corrections.

Corrections will continue. Gold in particular will react to economic data (like the jobs report that came out two days later, its narrow miss causing much confusion for gold traders) and to the election (Hilary rising is one reason gold is sliding, even though her spending plans actually support the yellow metal) and to US corporate earnings (which have now declined six quarters in a row), all the while pricing in a December rate hike (expectations of a hike boosted the US dollar 1.3% in the first week of October, amplifying gold’s slide).

A rate hike does seem increasingly likely. Hawkish Fed members are getting more aggressive in pushing for a move; Jeffrey Lacker, for instance, is openly arguing for a raise right now so that the Fed is ahead of inflation. And while data continues to show an anemic recovery, in many ways we’re right back where we were a year ago: the Fed has talked about a hike for so long that they almost have to move to retain credibility, unless data turns decidedly down.

So gold’s ascent will have to wait until the biggest of these questions – the election and the December rate hike – are answered.

But consider this: while it would be more fun if gold would just start rising again right now, this new sideways-for-a-while setup has two benefits.

First, the markets now have two full months to price in a rate hike. Gold, stocks, bonds – they should all adjust between now and December so that the hike, if it happens, does not cause chaos.

Second, it gives investors two months to act. Gold and silver companies are down across the board, from big majors to junior explorers. That means opportunities you liked but missed before they moved in the first phase of the bull market are back at better entry points.

The case for the general gold bull market remains intact. US equities are overpriced, which means stocks fail to offer security or value. Bonds are overpriced and even a fairly mild rise in yields would hammer prices, erasing capital that yields will take a long time to repay.

On a day-to-day basis, US data releases will drive gold. For example, the non-manufacturing PMI beat of 57.1 was the main reason gold slid on October 5th. That number suggests a services sector expanding nicely, if the rate can hold up, and that matters since services account for something like 70% of the US economy.

Following that was the September jobs report. Consensus expectation was for 169,000 new jobs; the actual number was 156,000. Coming days after gold’s big slide, the narrow miss left traders confused and saw gold gain, slide, and gain again before the day was done.

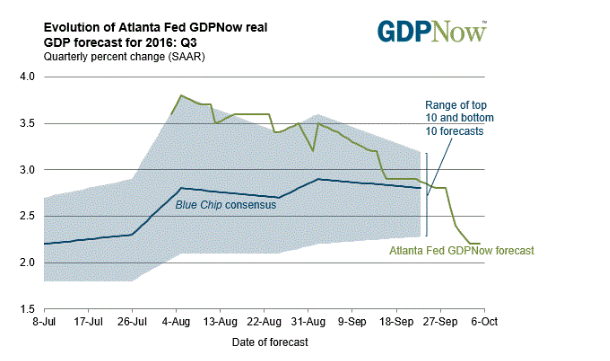

Zooming out from specific data points, things still look shaky. The Federal Reserve of Atlanta just updated its GDP Now forecast by downgrading its expectations for Q3 GDP growth to just 2.2%. Only two months ago the service was expecting 3.8% growth in the quarter. The IMF too slashed expectations; its forecast for US GDP growth in 2016 is just 1.6%.

Hike or no hike, the world remains grounded in negative real rates, which means no incentive to hold cash or bonds (unless you want to play bonds for price, a game that appears increasingly risky). Inflation seems to be on the rise, amped by OPEC’s oil output agreement that boosted the price of oil. Equities are expensive. And gold offers security and value in the face of all that.

It just seems now that we may need to wait until January for gold to really go again.

If you have questions about this article, please contact your Sprott financial advisor at 800-477-7853.

Creative Commons image by Håkan Dahlström

More News

Miners escape from attacked coal mine in Russian-controlled Ukraine, official says

April 06, 2026 | 12:31 pm

Panama moves to unlock copper from First Quantum mine

April 06, 2026 | 11:03 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments