Gold demand – Q4 recovery fails to mitigate full year declines in 2017

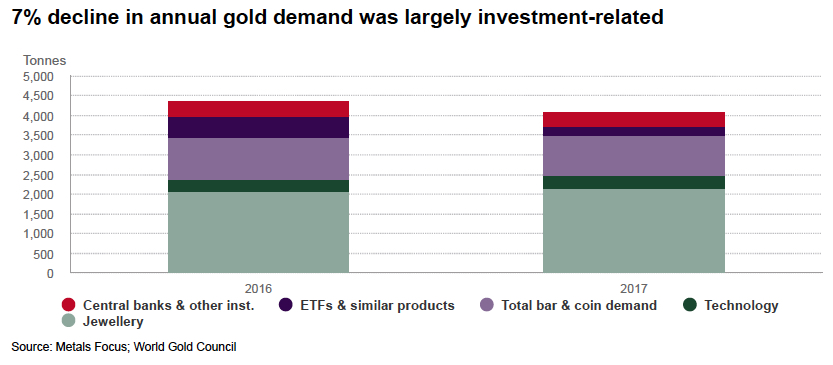

Gold demand rallied in the closing months of 2017, gaining 6% year-on-year in Q4 to reach 1,095.8 tonnes (t). However, overall demand for the full year fell by 7% to 4,071.7t, compared with 2016, according to theA late rally in physical gold buying failed to prevent a drop in full-year demand last year to its lowest since 2009, the World Gold Council said on Tuesday, as weaker fund investment outstripped a bump in jewelry consumption.s latest Gold Demand Trends report.

Inflows into exchange-traded funds (ETFs) continued steadily throughout the year, totalling 202.8t, but lagged behind the exceptional levels seen in 2016. Similarly, although central banks continued to add to reserves, purchasing 371t in 2017, buying was down 5% year-on- year.

Full-year bar and coin demand fell 2% as US retail investment dropped sharply. However, the year saw a recovery in both jewellery and technology demand, each making modest gains compared with 2016, as improving economic conditions lifted consumer sentiment in India and China, and an increase in gold-containing technology, such as smartphones and tablets, boosted demand.

Positive annual ETF inflows add 202.8t to demand in 2017, however this was around one-third of 2016’s inflows. European-listed gold-backed ETFs accounted for 73% of net inflows, with investors keenly attuned to geopolitics and negative interest rates.

2017 saw the first annual increase in jewellery demand since 2013

Bar investment was broadly stable, while coin investment slid 10%. Weakness in the sector, down 2% to 1,029t compared with 2016, was largely explained by a sharp drop in US demand to a 10-year low of 39t, which exceeded strong gains in both China and Turkey.

2017 saw the first annual increase in jewellery demand since 2013, but the sector remains weak in a historical context. Relatively stable prices and improving economic conditions paved the way for growth, but demand remains soft compared with long-term average levels. India and

China eclipsed other markets, together accounting for 75t of the 82t (4%) increase in global full-year demand.

Official gold reserves swelled by 371t in 2017, 5% down on 2016 levels. Turkey joined Russia as the most prominent of the central bank buyers.

The US dollar gold price was up 13% and institutional investors, especially in Europe, continued to add gold to their portfolios as a hedge against frothy asset prices and geopolitical uncertainty

The technology sector recovered in 2017, up 3% to 333t compared with 2016, ending a 6-year downtrend. The volume of gold used in electronics and other industrial applications grew steadily throughout the year, thanks to the increasing prevalence of new-generation features in smartphones, vehicles and laptops.

Alistair Hewitt, Head of Market Intelligence at the World Gold Council, commented:

“It’s not surprising to see overall gold demand down given the backdrop of monetary policy tightening and strong equity markets in 2017, but the market is not in bad shape. The US dollar gold price was up 13% and institutional investors, especially in Europe, continued to add gold to their portfolios as a hedge against frothy asset prices and geopolitical uncertainty. “Jewellery demand picked up as economic conditions improved in China and a policy change in India removed a barrier to demand, while next-generation smartphones boosted gold demand from technology companies.”

Mine production inched to a record high of 3,269t in 2017, while recycling fell 10%, leading to total supply dipping 4% to 4,398t. The introduction of stringent environmental controls in China saw a 9% fall in mine production in the region, whilst the ongoing concentrate exports ban continued to impact output in Tanzania. Total net de-hedging in 2017 reached 30t, bringing to an end three consecutive years of modest net hedging.

The key findings included in the Gold Demand Trends Full Year 2017 report are as follows:

Full Year 2017 figures:

- • Overall demand for FY 2017 was 4,072t, a fall of 7% compared with 4,362t in 2016

- • Total consumer demand in FY 2017 rose by 2% to 3,165t, from 3,102t in 2016

- • Total investment demand fell 23% to 1,232t in FY 2017 from 1,595t in 2016

- • Global jewellery demand grew 4% to 2,136t, from 2,054t in the same period last year

- • Central bank demand was 371t, down 5% compared with 390t in 2016

- • Demand in the technology sector increased by 3% to 333t from 323t in 2016

- • Total supply was down 4% to 4,398t, from 4,591t during 2016

- • Recycling fell 10% to 1,160t compared with 1,295t in 2016

Q4 2017 figures:

- • Overall demand was 1,096t, an increase of 6% compared with 1,036t in Q4 2016

- • Total consumer demand fell by 10% to 906t, from 1,006t in the same period last year

- • Total investment demand was up 41% to 286t compared with 202t in Q4 2016

- • Global jewellery demand grew 3% to 649t, from 630t in the same period in 2016

- • Central bank demand slowed 38% to 73t compared with 118t in Q4 2016

- • Demand in the technology sector increased 5% to 88t compared with 84t in Q4 2016

- • Total supply was up 1% to 1,095t, from 1,080t in the same period last year

- • Recycling grew 8% to 277t compared with 257t in Q4 2016

The Gold Demand Trends Full Year 2017 report, which includes comprehensive data provided by Metals Focus, can be viewed at http://www.gold.org/research/gold-demand- trends and on our iOS and Android apps. Gold Demand Trends data can also be explored using our interactive charting tool http://www.gold.org/data/gold-supply-and-demand/gold- market-chart.

You can follow the World Gold Council on Twitter at @goldcouncil and Like on Facebook.

|

ENDS For further information please contact: Stephanie Mackrell World Gold Council T +44 207 826 4763 |

Kate Savage Edelman T +44 203 047 2587 |

More News

Column: Iran war exposes fragility of Western aluminum market

March 09, 2026 | 04:22 pm

Venezuela acting government sends mining reform bill to legislature

March 09, 2026 | 04:08 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments