Glencore is the tempting devil sat on mining’s shoulder: Gadfly

The mining industry these days resembles that old cartoon about a person torn between prudence and temptation.

On one shoulder, a white-clad angel is whispering about the virtues of capital discipline, shareholder value and generous dividends. On the other sits Glencore Plc Chief Executive Officer Ivan Glasenberg, clad in red and promising to buy or build everything in sight.

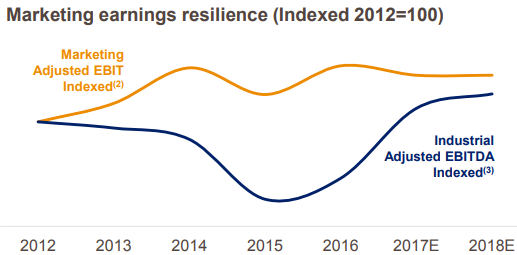

The reason for that contrast was laid out clearly at the start of a Glencore investor presentation Tuesday. Uniquely among its peers, Glencore derives a substantial slice of its earnings from trading commodities, rather than producing them. When mining is weak, marketing can take up the slack, and vice versa, as this company chart shows:

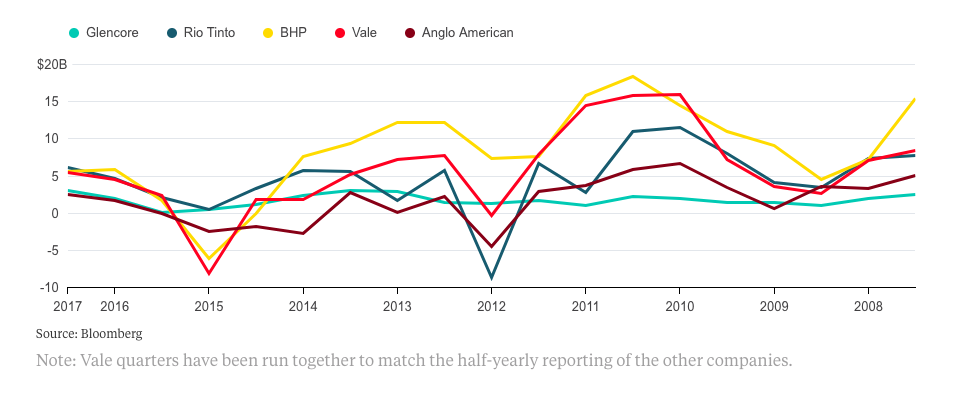

Another way of thinking about this is that whereas BHP Billiton Ltd., Rio Tinto Group and Vale SA all saw a gap of more than $20 billion between their record-high and record-low earnings half-years over the past decade, just $3 billion separated Glencore’s peak and trough. In an industry that’s been characterized by boom and bust since the first gold rush, trading has kept Glasenberg’s income on a steady path.

Everything in Moderation

While its rivals have seen Ebit surge and sink, Glencore’s has remained stable for a decade.

As any bond investor knows, consistency has its virtues. While other miners are still banished to the naughty step that shareholders sent them to after the vast destruction of value from the recent commodities boom, Glasenberg is getting his toys out again.

Capital spending in 2018 will be $4.8 billion, the company said Tuesday, as Glencore works to more than double its production of cobalt, add about 40 percent to its crude oil output, and lift copper, zinc, nickel and lead by about 20 percent to 25 percent each.

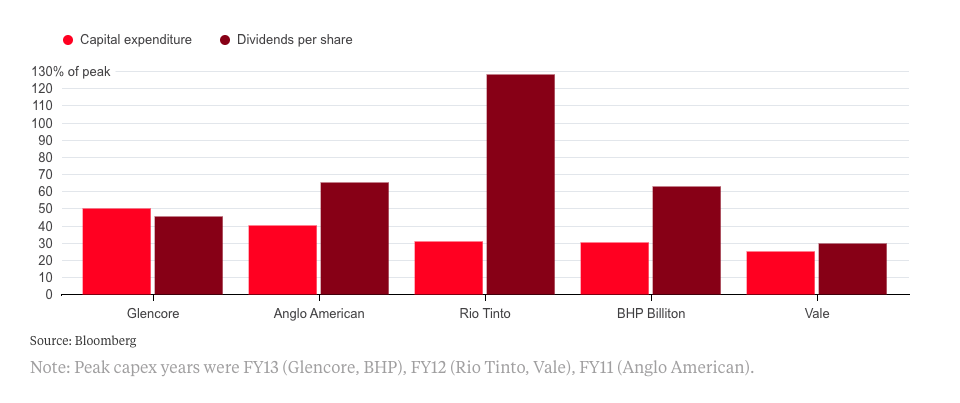

That’s in marked contrast to rivals. Forecast capex for Rio Tinto is 70 percent below former peaks, even though dividend payments have already exceeded previous records. Anglo American Plc and BHP are paying out dividends at about two-thirds of peak levels, but capex is again down 60 percent to 70 percent. Only Vale — listed in the less-dividend-hungry U.S. and Brazil, and with the heaviest debt burden among conventional miners — matches Glencore’s stinginess when it comes to rewarding shareholders, and its capex budget is just a quarter of its highest levels.

Return to normalcy

Why should all this bother the rest of the mining industry? Surely it’s Glencore’s business what it does with its money?

The problem is that the world’s miners operate in a sort of global version of the prisoner’s dilemma. Collectively, their earnings tend to be best when supply is tight, spending slight, and prices high — more or less the conditions they’ve experienced over the past 18 months or so.

The temptation for any individual company, though, is to ramp up supply in the face of higher prices and capture the largest possible market share. When everyone starts behaving like that, the resultant indiscipline tends to destroy profits for the whole industry.

Well, almost. Every miner caught a glimpse of their own mortality at the end of 2015, but the resilience of those trading earnings meant that Glencore’s recovery has been quicker than most — so no wonder its spending is on the rise, too.

Rivals still nursing bruises from the crash should reflect on the unique qualities of Glasenberg’s business before yielding to the temptation whispered in his spending plans.

Peter Grauer, the chairman of Bloomberg LP, is a senior independent non-executive director at Glencore.

Story by David Fickling.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments