Gensource Potash (TSXV:GSP) – trading for pennies on the dollar – literally

When we last wrote about Gensource Potash, the company just signed an offtake worth C$500 million with Yancoal Canada Resources, a wholly-owned subsidiary of Yanzou Coal Mining Company (YZC), a US$6 billion company and majority owned by state-owned Yankuang Group. The news propelled Gensource into the spotlight; the scrappy junior was able to secure a deal that creatively leapfrogged C$65 million in spending. Nevertheless, the company still trades at a paltry C$14 million, leading us to believe this is one of the most undervalued companies in Canada. This is especially infuriating to us being large shareholders of the company.

Regardless, the boys from Saskatchewan are still grinding away. Since the acquisition of the Vanguard project from Yancoal, Gensource has released an updated 43-101 resource, and more importantly, a preliminary economic assessment (PEA). Before we delve into some serious and robust economics of the PEA, let’s go over the steps Mike and Rob took to get here.

Lazlo, From Flagship To Icing On The Cake

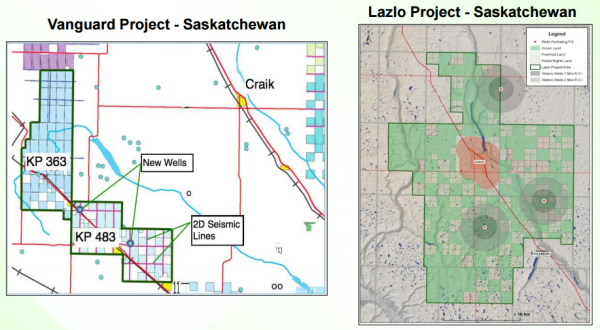

Up until the transaction with Yancoal, Gensource was working diligently on the Lazlo project. The company was working on defining a formal 43-101 resource, which would have been backed into an internal ‘scoping’ study for a prefeasibility study (PFS). All that was left was to drill two wells and some additional 2D seismic, at a cost of around C$5 million. From the last quarter of 2015 and the first quarter of 2016, the company was able to raise over C$2 million to put towards Lazlo. In the hardest of capital markets, Mike and company were able to move ahead.

In April 2016, Gensource came to a transformational agreement with Yancoal Canada and acquired the Vanguard project while agreeing to an off-take. The acquisition did not take away from the company’s overall strategy, but it did put Lazlo on the backburner for the time being.

Gensource acquired two permits covering 63,800 acres of land, and significant geological data. There has been over C$4 million in field work completed on the leases, including: two drilled wells, cored, logged and assayed for potash; 110 kilometers of 2D seismic, extensive geological and engineering work. Vanguard was more advanced than Lazlo, and since the engineering was already completed for Lazlo, Gensource was able to apply that work to Vanguard and release a PEA less than two months after the announced acquisition.

C$500 Off-take, C$212 Million NPV, Minimal Environmental Footprint

That is correct. Gensource’s Vanguard boasts an after-tax NPV8 of C$212 million and IRR of 16.86%.

But one of the most important takeaways from the PEA is the projected capex of C$247 million. As we mentioned in our last report, this cost is significantly lower than the traditional potash mine, which comes with an average price of C$4.2 billion. The lower price tag is the result of the utilizing selective dissolution versus the traditional conventional underground mining and solution mining. To read more about the methods, click here for the original write-up; but to summarize, selective dissolution evolved from solution mining and features some key differences by employing newer technology that eliminates a lot of unnecessary layers and steps. Thus, a company can return profits on smaller scale operations.

We mentioned that the capex was an important takeaway, but the single most important highlight is the minimal environmental impact Vanguard will have. First, unlike traditional potash mining methods, selective dissolution does not leave mountains of salt tailings.

Source: goingeast.ca, Potash tailings dominating the skyline

When a traditional potash mine is decommissioned, it will take hundreds of years before the site is reclaimed. Natural rain is relied onto slowly dissolve the mountains of salt, while injection wells are kept in operation to dispose of any excess brine created during the process. In selective dissolution mining, no salt tailings are brought to surface; it is simply left in the underground caverns where the potash is contained.

Furthermore, selective dissolution does not use fresh surface water. The traditional potash mine goes through billions of litres of water, and in dry southern Saskatchewan, you can imagine the kind of pushback farmers and environmentalists will have. Selective dissolution utilizes existing saline water found in the deep formations, which is continuously recycled in the mining process.

We imagine Yancoal’s sale of the Vanguard project to Gensource and the subsequent off-take stems from the troubles it is having with its Southey project, located just north of Southey, Saskatchewan. The $3.6 million project is currently working towards an environmental impact statement (EIS), but is already being met with significant pushback from the locals, the majority of which are farmers that do not want to share precious water and have mountains of salt next to their precious crop.

Moving Forward, The Gensource Way

Gensource has around C$1.7 million in cash, which is more than enough to cover the C$1.24 million payment to complete the Yancoal transaction. The next major catalyst on the horizon is the feasibility study (FS), which will require two more wells, some more seismic, and further engineering and environmental work. This will cost the company ~C$3 million, which means Gensource will probably need to raise money in the near future to keep to its torrid schedule.

In even the worst of markets, Gensource has been able to secure financing so this should be no problem. We also believe Gensource will be able to secure construction financing – with a C$500 million off-take secured, we imagine YZC’s bank or another conglomerate will step to the table, but this of course will be closer to FS completion or after October 2016.

Let’s not forget about Lazlo. As Vanguard progresses, this also proves up Lazlo’s viability, which we already know exists as it is carbon copy of Vanguard. We believe Gensource will option Lazlo to a major chemical player and will be carried to construction. Lazlo only needs two wells and seismic to get a prefeasibility study, and can get to a full feasibility with another C$10 million in spending. Being almost identical in terms of geology, Lazlo can easily achieve economics similar to Vanguard. Lazlo truly is a free call option.

Is Gensource undervalued? The answer is a resounding yes. The company currently has a market cap of C$14 million, but has a C$500 million off-take, and an after-tax project NPV8 of C$212 million.

Gensource will be the next producer of potash in Saskatchewan because it is economically robust, but most importantly, will appease environmentalists and farmers alike. We will continue accumulating shares and pounding the table.

Palisade Global Investments Limited holds shares of Gensource Potash. We receive either monetary or securities compensation for our services. We stand to benefit from any volume this write-up may generate. The information contained in such write-ups is not intended as individual investment advice and is not designed to meet your personal financial situation. Information contained in this report is obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The opinions expressed in this report are those of Palisade Global Investments and are subject to change without notice. The information in this report may become outdated and there is no obligation to update any such information.Do your own due diligence.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments