Frugal billionaire seen as tough negotiator for copper funds

(Bloomberg) —At first glance, the prospect of a new business-friendly president in Chile augurs well for the economy and in turn for bondholders in giant state copper miner Codelco.

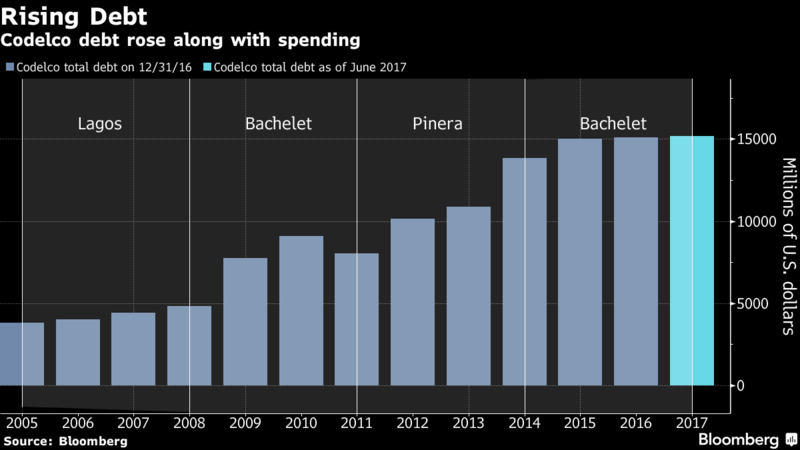

But looks can be deceiving. During his first term as president, Sebastian Pinera, the billionaire front-runner in Sunday’s election, was so frugal when it came to funding Codelco that the state-owned company’s debt levels jumped 84 percent, despite high copper prices.

Pinera is now pledging to cut public spending and reduce Chile’s fiscal deficit at a time when Codelco is locked into a record investment program to overhaul its aging deposits. While Codelco has funding guaranteed through 2019, it will have to negotiate with the government in 2020 for money to complete investments needed to remain as the world’s biggest copper producer. Any gaps would have to be plugged with new bonds.

The candidate is calling for “deep reflection” to define a new capital allocation system for Codelco. “It seems reasonable to set an amount of investment that can be financed by the state and the company then prioritizes the plan based on that,” his mining coordinator, Francisco Orrego, said by email.

“If Pinera wins, the negotiation will be quite complex,” Guillermo Holzmann, a political analyst and a professor at Universidad de Valparaiso, said by telephone. “He will require more efficiency and will demand results in terms of transparency, productivity and profitability.”

Codelco has cut costs and reduced the size of its investment program from more than $20 billion to $18 billion during President Michelle Bachelet’s term, when copper prices slumped to four-year lows before recovering.

It will need $4 billion annually over the next five years. Rising copper prices mean it will be able to finance a larger share of the investments itself, with each additional cent per pound bringing as much as $35 million in cash flow, the company said. But it will still require funding from the state, and maybe from the debt markets.

“Codelco has made a great effort to reduce costs and optimize investments,” a Codelco official said in a written answer to questions. “But the contribution of the state is necessary to support investment so we can have the right capital structure and we can keep developing the projects ahead.”

‘Golden Eggs’

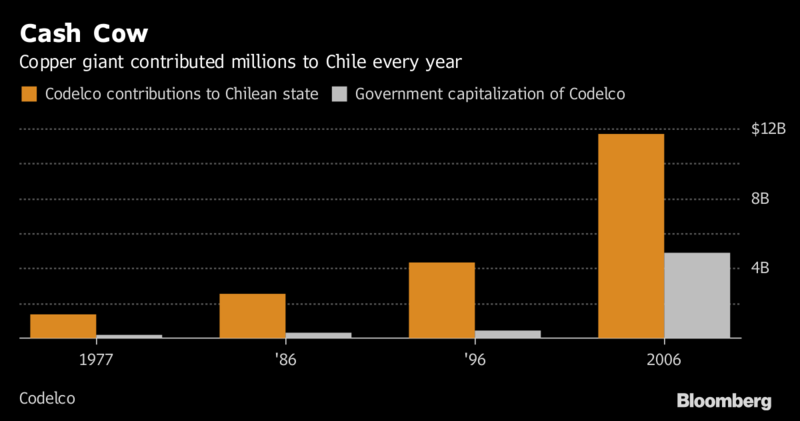

Codelco hands over all of its profit to the Chilean state, which then decides whether it reinvests some in the company. A multi-year capitalization plan has been introduced to ensure the company has funding beyond the end of Bachelet’s term in March 2018.

“Codelco will severely jeopardize its financial health if governments keep taking almost all of its cash generation, obliging the company to raise debt to assure its long term continuity,” said Alejandra Fernandez, Fitch director of corporate ratings.

All the signs indicate a mix in funding under the new government, she said.

“There is a quite general awareness in the country that Codelco needs a more structural capitalization plan that allows it to finance its investment needs through 2026,” Fernandez said by phone from Santiago. “To do otherwise would be to kill the goose that laid the golden eggs.”

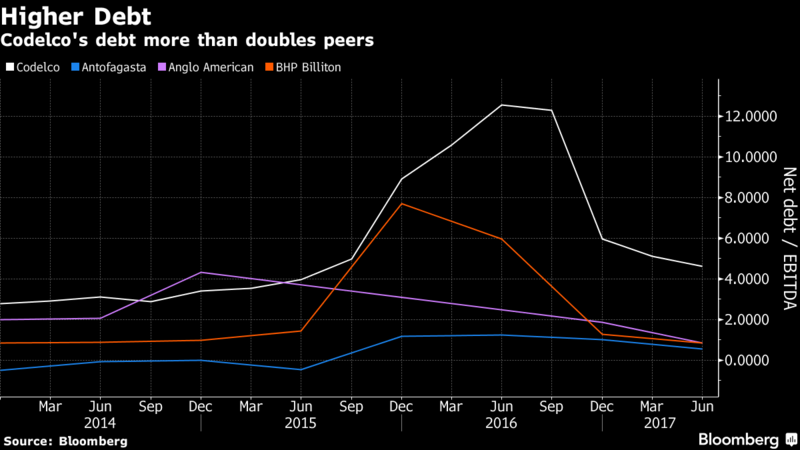

Codelco’s total debt has risen to about $15 billion, from $8 billion at the end of 2011, when copper prices were at record highs. Its ratio of debt to earnings before interest, taxes, depreciation and amortization is more than double that of peers such as Antofagasta Plc., BHP Billiton Ltd. or Anglo American Plc. The company’s debt is expected to increase by $1 billion in 2019 and 2020, according to Fitch estimates.

“Codelco will probably need some additional financing through capital markets to complete the financing of its projects,” the company said. “This will depend on market conditions and on the approval of projects that are being evaluated today.”

Should Pinera win, there is one other issue that he must deal with — a law dating from the dictatorship of Augusto Pinochet that forces Codelco to pay 10 percent of its revenue to the Chilean armed forces. In 2016, the company reported its first half-year loss and had to get into debt to pay for the army’s share of the copper sales.

“The company’s standalone credit profile has weakened in the last few years,” Fernandez said. “It has to do with the debt generated through large cash requirements such as high capital expenditure, taxes, and the reserved copper law in a context of low copper prices.”

Pinera is leading the polls with 44.4 percent support ahead of the first round on Nov. 19, more than double any other candidate. If no candidate wins a majority, the two leading contenders will go to a run-off on Dec. 17.

Bargaining Chip

Codelco bonds have returned 31 percent since Bachelet took office, in line with the average among global mining notes tracked by Bloomberg. In Pinera’s first term as president from 2010 to 2014, the bonds also returned 31 percent, matching the peer average.

Bachelet’s government sold government bonds worth $3 billion to finance Codelco, but Pinera is unlikely to be so generous, according to Patricio Navia, a political scientist with New York University.

“I don’t see the government borrowing money to fund Codelco because that would make them appear as fiscally irresponsible,” Navia said by telephone. “Pinera will demand reforms in Codelco before he approves ambitious capitalization plans. Within his inner circle there’s the perception that there is still room for cuts in Codelco.”

The future of Codelco’s funding will ultimately depend on the balance of power in Congress. Even if Pinera wins the presidency, his chances of holding a majority in the senate are slim, Navia said.

“I suspect a Congress where left-wing parties and Christian Democrats have a majority will be more interested in a more ambitious capitalization program,” Navia said. “Pinera could use Codelco as a bargaining chip in exchange for support for things he really wants to go through.”

(Story by Laura Millan Lombrana with assistance by Sebastian Boyd).

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments