Eurozone is no bargain market, despite higher gains in US: David Stevenson, Fleet Street Letter

Rip-roaring market valuations in the US are supported by ever-expanding corporate and government debt.

Corporations borrow cheaply and use the money to drive their share prices higher.

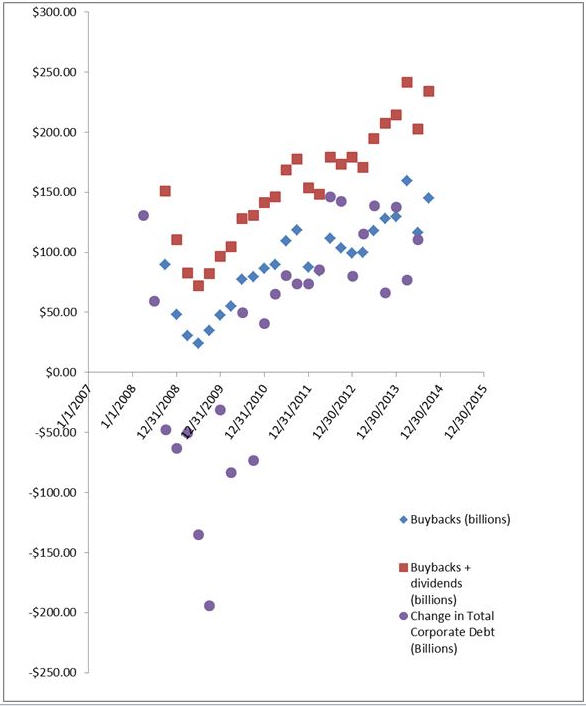

Just look at corporate debt rise in tandem with stock buybacks and investor payouts over the last few years (data: S&P Dow Jones Indices and Board of Governors of the Federal Reserve System).

Europe’s stock market and economic numbers have lagged the US in performance.

Europe’s stock market and economic numbers have lagged the US in performance.

In January 2015, the ECB stepped in with over 1 trillion euros planned for bond buybacks, a program based on the Fed’s Quantitative Easing.1

Many investors see lagging performance in EU stock markets and the ECB’s new stimulus program and believe that Europe could catch up with US stock-market performance.

Is there more opportunity for bargains in European markets?

David Stevenson is the driving force behind the Fleet Street Letter, Britain’s “longest-running investment society.” He is a former fund manager from the City of London.

David warns that things are looking over-priced in Europe too, even if yield-seeking investors might find higher dividend yields there.

David also discusses why he’s bearish on the future of Europe’s currency union and why silver has been in his sights as a contrarian investor.

Click here for full audio (Mp3) >

David, you’re based out of the UK and you are a contrarian investor. Can you talk about some of the past great contrarian opportunities in the UK and in the EU that you’ve experienced over the last 10 years or so?

David Stevenson: I think 10 years might be a bit long. I think the market has been very volatile over that period. Obviously we saw a build up to the Great Financial Crisis when markets were very strong and that was the time that I became very wary of stock market levels and then of course the Great Financial Crisis prompted a massive decline. I have to say that, probably along with a lot of other people, I hadn’t appreciated that there would be a recovery as quickly as there has been.

But what it has done is thrown up a number of value opportunities which we take advantage of in the Fleet Street Letter.

We’re now reaching a point where the value opportunities are less numerous than they were and I think that applies, Henry, to any stock market – it applies to the UK just as much as it applies to the United States.

So we’re now reaching a point where, for the contrarian value investor, it’s time to take stock and possibly reassess whether there are going to be as many opportunities going forward as there have been over the last five years.

Is the fact that markets in Europe have somewhat lagged the performance of North American markets an indication that there is more value to be had in European markets right now?

I would tend to put it the other way around and say that maybe it means there’s less value to be had in the US market.

That has now become very expensive in some areas and European markets have rallied too. I mean there’s the UK which is actually also near all-time highs. In Germany for example, you see the markets going through its previous highs, so it’s not like Europe and the UK have been sort of ‘sitting on the sidelines’ because they’ve both been performing pretty well. It’s just that the US has gone even faster.

Many years ago, Henry, I had started in the markets and was looking at companies on value criteria. I remember one analyst telling me he was appalled that I was contemplating something for around four times sales.

Now if you look these days across companies at prices to sales, a ratio of four times is almost commonplace and it’s indicative, I think, of the extent to which markets have jumped up on the back of external influences like central bank policies and low interest rates – or nil interest rates.

It’s a reflection of how far the manipulation, if you like, has driven markets to levels that could be unsustainable.

Do you think that central banking is impacting the economy and creating these bubbles in stock market valuations to the same extent in Europe as it is in the United States? How do you think it’s going to play out going forward?

Sure. The European Central Bank (ECB) decided to go down the same quantitative-easing floundering route as have been following the US, the UK and Japan.

I think the ECB is certainly saying it will try to do the same thing. It is having the same effect on asset prices. So while that still has a little way to go in terms of the policy implementation, in terms of the effect on stock market and pricing valuation I would suspect that Europe has gone quite a long way down the road to where it’s going in terms of stock market levels.

But I think it would be a mistake to assume that the ECB is going to drive European stock market a great deal higher from this point.

Does this lead you to own gold and silver right now as a protection against the potential fallout from these policies?

We’ve been quite optimistic about gold, if you like, as long-term insurance policy in the portfolio against financial crisis. It’s obviously also an insurance against inflation at the moment. There isn’t very much of that around, though inflation expectations are starting to pick up again.

Silver I think is the more interesting of the two. We’ve been very bullish about silver, not just because of its precious metal element as a ‘safe haven’ but also because it is an amazing metal in its own right.

It has so many applications in a lot of areas. It conducts heat for thermal application. It has electrical conductivity, light reflectivity, with use in everything from refrigerators to solar power. It’s a metal that has great industrial use and yet inventories are coming down progressively and mining supply of the metal is topping out.

So the metal is now moving into a shortage situation on an annualized basis and that can lead to a significant recovery in the price of the metal and silver producers over the next few years.

Why do you think the euro has gotten cheaper compared to the dollar when the ECB has pursued less aggressive central-bank policies than the Federal Reserve, until recently?

I think that’s now reversing with the ECB’s QE (Quantitative Easing) policy. I think the euro has also suffered from problems within the single-currency euro union. The fear that Greece might at some point pull out, causing a fragmentation of the single currency is one of the significant factors for the euro weaknesses.

Now, whatever anybody is telling you today or tomorrow about Greece, the fact is that the country is bust and it’s not going to get any better fast.

That said, there has been a little bit of a rally in the euro against the dollar and against the pound recently and that is something that is likely to continue for a little bit.

What is governing in terms of pricing? It’s that stock market prices have gone up – company share prices were being helped because of a weaker euro, as a weak euro would boost profits. Within the economies themselves, I think we will start to see a little bit of an increase in inflationary expectations returning, not least because the oil price is recovering again and that’s going to filter through.

So I think if you add up the whole euro picture, the euro itself probably could have a period of volatility and after that it could well decline.

I’ve actually been a bear of the euro structure for a very long time. I think it’s a dangerous concept to bring so many disparate countries together under the same currency banner and there are a lot of things still going wrong down the track.

So I take it that you don’t see a lot of contrarian buying opportunities related to Greece at the moment. You think that this is going to go from bad to worse?

Yeah, I just think you don’t know what currency they’re going to end up holding and therefore it’s probably not worth taking that sort of risk.

There was quite steep buying of Greek bonds a few months ago which has paid off but I think it isn’t a risk worth taking. I would tend to avoid that.

One thing you also mentioned of course was the UK and there the recent scene has been influenced by the general election which the conservatives —the more to the right of the mainstream parties — have been reelected with an overall majority. They can now implement the sort of business-friendly policies which the stock market is going to like. So that has been short-term support for the sterling and that’s probably a reason why the pound has continued to be fairly firm.

In the last bubble in 2007 and 2008, we saw that the EU economy and stock market were very dependent on the health of the US economy. Will any problems with the stock market rally in the US likely cause some kind of crash in the EU as well?

I think it’s almost inevitable. When Wall Street sneezes, everybody else catches a cold. My belief is that at some point the US market could correct in a thunderous and fairly unpleasant way and that is going to be felt around the world.

I’m old enough to remember 1987 and Black Monday and what happened then. What happened in Wall Street hit London a few minutes later. It really was a question of the sort of global stock market contagion which hit very fast.

Who knows how long-lasting it would be? When you actually look back at something like 1987 you do see at the time that there was some performance in the markets. But I think no doubt that if the US markets were to fall very sharply, we would see ramifications around the world.

What are some differences with investing in contrarian opportunities in the UK and the EU relative to investing in the US and Canada? Is there anything that US investors should know if they’re thinking of entering European markets?

I think the principles remain the same around the world. I judge things in terms of valuation, in terms of yield, in terms of price-to-book value, in terms of debt levels, and cash generation and I apply the same criteria to stocks wherever they are.

The comment that I would make is that there are less opportunities to pick up income stream in the United States than there are in Europe or the UK. Dividend yields in the UK and Europe are much higher. That means payout ratios are higher.

There are some figures produced by markets over a very long period of time that show the difference between when dividends are being reinvested into your investments and not reinvested and the difference is absolutely staggering.

If you basically get a decent dividend stream for a company, and you re-invest that in the stock, that’s amplifying the return over a 20 or 25-year period by a massive multiple.

That is an opportunity you’re going to have with high dividend yields. In the United States, there aren’t these dividend yields. In the UK and in Europe, if you’re selective and if you look around, you can find them.

Henry Bonner: Thank you for sharing your thoughts with us David and I look forward to speaking with you again.

David Stevenson: Great. Thanks a lot.

P.S.: Spots for Sprott’s upcoming Natural Resource Symposium are filling up fast! Learn how to become a better contrarian investor at our natural resources and precious metals conference this summer. Join an elite group of investors July 28-31 in at the Fairmont Hotel Vancouver. Click here for the full details!

Having started a career in the City with Morgan Grenfell Investment Management, David Stevenson joined Oppenheimer in 1983, starting as a UK fund manager before working for Hill Samuel, Cigna and IAI International and BNP Securities.

For a full introduction to David, visit the Fleet Street Letter website.

1 http://www.cnbc.com/id/102556078

By Henry Bonner ([email protected])

Read online >

This information is for information purposes only and is not intended to be an offer or solicitation for the sale of any financial product or service or a recommendation or determination by Sprott Global Resource Investments Ltd. that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy based on the objectives of the investor, financial situation, investment horizon, and their particular needs. This information is not intended to provide financial, tax, legal, accounting or other professional advice since such advice always requires consideration of individual circumstances. The products discussed herein are not insured by the FDIC or any other governmental agency, are subject to risks, including a possible loss of the principal amount invested.

Generally, natural resources investments are more volatile on a daily basis and have higher headline risk than other sectors as they tend to be more sensitive to economic data, political and regulatory events as well as underlying commodity prices. Natural resource investments are influenced by the price of underlying commodities like oil, gas, metals, coal, etc.; several of which trade on various exchanges and have price fluctuations based on short-term dynamics partly driven by demand/supply and nowadays also by investment flows. Natural resource investments tend to react more sensitively to global events and economic data than other sectors, whether it is a natural disaster like an earthquake, political upheaval in the Middle East or release of employment data in the U.S. Low priced securities can be very risky and may result in the loss of part or all of your investment. Because of significant volatility, large dealer spreads and very limited market liquidity, typically you will not be able to sell a low priced security immediately back to the dealer at the same price it sold the stock to you. In some cases, the stock may fall quickly in value. Investing in foreign markets may entail greater risks than those normally associated with domestic markets, such as political, currency, economic and market risks. You should carefully consider whether trading in low priced and international securities is suitable for you in light of your circumstances and financial resources. Past performance is no guarantee of future returns. Sprott Global, entities that it controls, family, friends, employees, associates, and others may hold positions in the securities it recommends to clients, and may sell the same at any time.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments