Euphoria, greed and fear mark 2010s for commodities investors

The past decade — a humbling one for investors in commodities and raw materials — was a roller-coaster ride for mining stocks while chemicals saw a rise in popularity.

A brighter outlook for global economy could bolster cyclical stocks in 2020 as risk-on trades make a comeback. Bloomberg Intelligence commodity strategist Mike McGlone expects continued appreciation for gold, particularly compared to copper.

“If the past decade is a guide, gold is set to outshine copper and crude oil,” McGlone said. Meanwhile, its likely that chemical companies will continue their string of mergers and acquisitions, at least in 2020, to boost growth, according to Bloomberg Intelligence analyst Christopher Perrella.

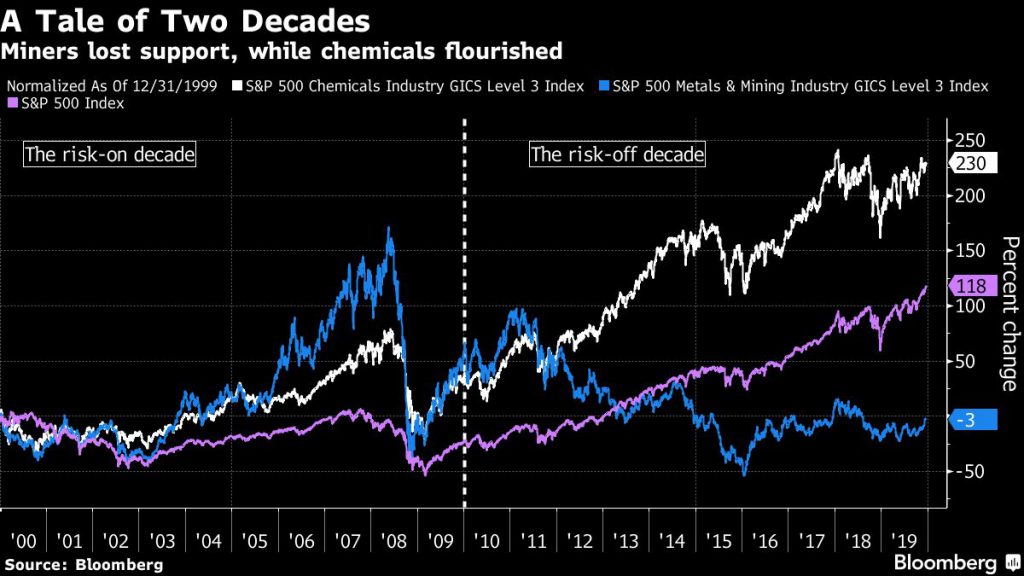

Looking back at the first 20 years of this century, it’s really been a tale of two decades for the raw materials sector: risk-on bets before the 2008 financial crisis, followed by risk-off investing as the “fear trade” dominated investor sentiment.

The performance of metals stocks versus chemicals makers over the past two decades shows how materials investors got hooked on growth stocks. The S&P 500 Chemicals Index gained about 33% from 2000 to 2009, while the S&P 500 Metals Index surged about 52%, coinciding with gold’s bull run. But after the 2008 financial crisis, the returns reversed course, leading to a 150% gain in chemicals from the start of 2010, against a slump of 36% in metal stocks, as gold fell from its peak.

Bull run

The gold rally that began around 2000 got a boost in 2002-2006 as a decline in the U.S. dollar raised inflation fears. Then bullion got supercharged after the 2008 crisis as investors ran for safety. The Fed’s quantitative easing coupled with Europe’s sovereign debt crisis in 2011-2012 carried spot gold prices to all-time highs of about $1,900 an ounce in September 2011.

During that bull run, gold miners started to overspend on acquisitions, anticipating higher demand for bullion. That led to mounting debt and billions of dollars in impairments, angering investors. Then when gold reversed, miners saw a mass exodus by investors, leaving some companies unable to service their debt and forcing most to slash costs to survive. The upshot was abysmal performance by the gold miners in the last decade.

Copper is also tied to the global economy and its prices mimicked gold’s bull run and eventual decline, leading the whole metals and mining sector to one of its longest and toughest slumps.

Flock to growth

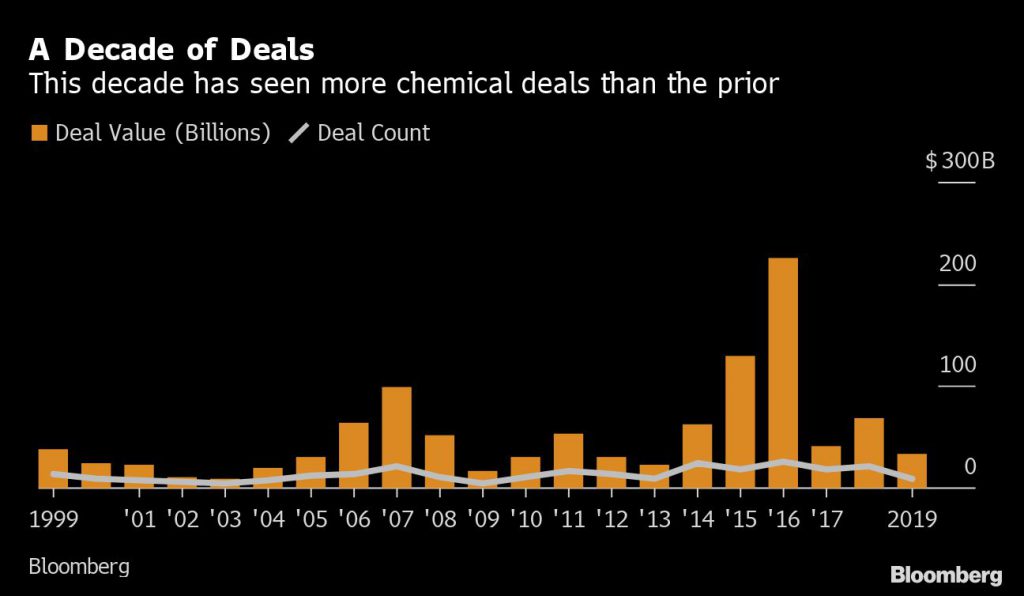

Chasing returns, investors in the sector sent their money where they saw growth, which led chemicals makers becoming even more popular after 2012. The chemical industry has always been among the favorite sectors for growth-oriented commodities investors, as companies relied on M&A to adapt to changing product cycles and gain market share. The sector climbed more or less steadily since 1999 but the move became more pronounced after the financial crisis and once miners fell out of favor. The focus on M&A became a major theme, and 2016 saw the most completed deals in the past two decades, according to data compiled by Bloomberg.

Along with a plethora of deals, the decade also ushered in a handful of the highest-profile reorganizations and restructurings in the past 20 years, transforming the industry. These included DuPont de Nemours Inc. and Dow Chemical Co.’s mega-merger in 2015, to create DowDuPont Inc., which was eventually broken up into three separate entities a couple of years later, creating even more deal making. Other mega-deals included China National Chemical Corp.’s buyout of Syngenta AG, fertilizer giant Potash Corp.’s merger with Agrium Inc., Bayer AG’s takeover of Monsanto Co. and Sherwin-Williams Co.’s takeover of Valspar Corp.

Even the U.S.-China trade dispute hasn’t dented much momentum in the group, as investors piled into specialty chemicals makers due to their diversified portfolio. The biggest returns since 2009 in the chemicals sector have come from Sherwin-Williams, PPG Industries Inc. and Ecolab Inc., which returned 846%, 354% and 331%, respectively, excluding dividends.

(By Aoyon Ashraf)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments