What drives China to Africa?

China National Gold was interpreted by Reuters (in a September 2013 interview with CNG’s Executive Vice President, Jerry Xie) as able to finance substantial capital costs and search for acquisition targets. This verbal flexing of CNG’s financial muscles was reported less than twelve months on from CNG’s collapsed takeover bid of the Tanzania operations of mining colossus, Barrick Gold.

CNG kept good on their promise later in 2013, when the corporation acquired Soremi, a copper mining subsidiary located in the Republic of Congo. First the flexing, then the killer blow.

Travel forward to late May 2017 and Chinese state-owned firm Chinalco is set to become the highest stakeholder of Guinea’s Simandou Mine. A deal worth around $1.1 – 1.3 billion has been agreed between Chinalco and partner Rio Tinto, which will see the former assume control of the latter’s 46.6% stake in the mine, with Chinalco already possessing its own 41.3%. The deal’s sum will be payable once Simandou, which has been a stalled project for over a year, is jump-started into gear and producing commercially. The deal also accounts for output.

The Simandou Mine is an iron ore deposit of great potential, with estimations of the mine’s reserves numbering around 2.4 billion tonnes of ore, grading 65% iron metal (Fe). For resource-hunter China, investment into the rejuvenation of Simandou, and the concomitant completion of the deal upon resumed production would both be mere cogs in the Chinese machine that has been expanding beyond its own borders in search of major mining and mineral assets since the introduction of a strategy that was launched—and blessed by the Government of China—in 2006. This strategy involved urging (with some empowerment) numerous domestic state-owned and private companies in China to explore and pursue mining deals across the global network.

Nestled deep within the Guinean interior, the Simandou Mine is four hundred miles from capital city Conakry. Much of that distance is dense, forested hills, and a government plan to connect the mine with Conakry, which will involve the construction of a 400-mile-long railway, thirty-five bridges, sixteen miles of tunnels, and a deepwater seaport, is estimated to cost approximately $23 billion, according to the Guinean government. Such a monumental infrastructural—and structural—upgrade will see its value to the country increase exponentially if the Simandou Mine is revived and able to meet and then exceed government wishes of annual production of 100 million tonnes of the ore.

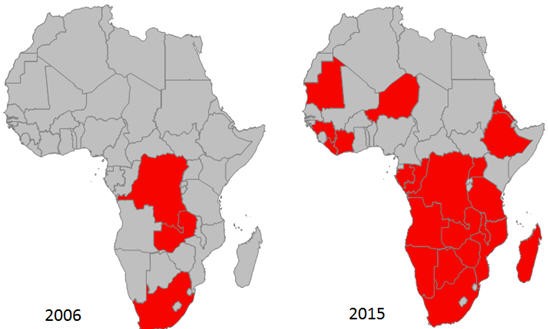

China National Gold and Chinalco are hardly reinventing the wheel these days by investing heavily in mining Africa. Since the 2006 call to action, Chinese-led mining activity on the African continent has–as evidenced in the source below–experienced rapid expansion. It began with a handful of southern and central African nations, but has now engulfed almost every country in the southern and central region, as well as penetrating a handful of west-African countries (including, of course, Guinea) above the Equator. Over 120 China-based companies now have active interests in this resource-rich land.

Figure 1 Chinese expansion of mining projects in Africa, 2006 – 2015

The mining machine has not slowed down through to 2017, either. And there are plenty of mining/mineral assets besides iron ore that China needs in order for its foundries to stay hot. Fortunately, Africa is a hotbed of industrial nutrients. South Africa, for example, produces over 51% of the world’s chromium; it is also the world leader in the production of manganese, and of ilmenite. South Africa is a top-5 global producer of rutile and zirconium. And that’s not to mention its renowned status as a gold-producing nation.

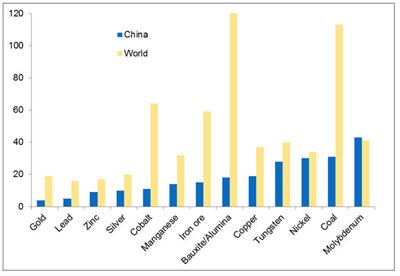

Figure 2 China’s ‘burn rate’ of resources compared with the rest of the world. Many of the country’s resource rates are dangerously low, triggering the need for global conquest.

Zimbabwe (lithium), Morocco (phosphates and phosphates reserves), Mozambique (ilmenite, zirconium, tantalum), Rwanda (tantalum leader), Botswana (diamond and other gemstones), and Democratic Republic of the Congo (cobalt, copper, diamond, tantalum) are all world leaders or top-5 countries for the production of ingredients that China seeks insatiably. And Chinalco’s latest target, Guinea, is a top-5 bauxite producer with world-leading bauxite reserves.

Not only is Africa abundant in the resources that China seeks, but the resources themselves are often to be found on greenfield sites, reducing if not removing the need for a company to contest with previous infrastructure. The cost of reviving Simandou is likely to be high.

There does, unfortunately for Guinea and its government, linger a list of potentially pernicious problems with regards to their objective: construction of the railway and its other components. The sooner Chinalco seeks to resurrect Simandou, the sooner the railway will have even more demand, since this will be the most effective method of transporting the iron ore to the aforementioned seaport. While speed is of the essence for Guinea, as Ibrahima Kassory Fofana (an advisor to President Alpha Conde) made clear in a recent comment to Reuters, such a tactic might not appeal to Chinalco.

“I have indications that they won’t start until 2025. That wouldn’t be acceptable.” – Fofana.

In the scheme of China’s 2006-begun strategy, eight years is a long time. 2.4 billion tonnes of iron reserves, graded at around 65% Fe, currently has a premium market value of around $110 billion. A game- and industry-changing figure. A figure that cartoonishly transforms eyes into dollar signs. A figure that could, over the course of the next eight years until 2025, fluctuate. Given the stagnation of Rio Tinto’s Simandou activity, experts in the mining industry have suggested that the time of the iron ore Supercycle might have passed already for Guinea, with large iron ore deposits in Australia (fourteen of which are owned by Rio Tinto) replete with global supply for numerous years.

Would, therefore, Chinalco be wise to sit on their property, and monitor the status of 1. the Australian iron ore industry; and 2. the premium price of iron ore graded around 65% Fe? China is the world’s foremost producer and consumer of steel, and its need to do both is unlikely to diminish any time soon. A long term control of resources could be financially and industrially prudent, compared with merely having an eye on short term shareholder value. Perhaps, for now, while their initial annexing movements might seem aggressive, and certainly fall in line with the Government of China’s strategy, Chinalco’s next move will see them unleash their financial broadsides outside of Africa while they plan how to proceed with the largest iron ore mine on Earth.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments