Disruption in potash production – revisiting a stale sector

The Potash Price Tag In Saskatchewan

Many years ago, I drove through Saskatchewan. My memories of the experience, much like the region’s landscape, are rather non-descript. The landscape stretched out completely flat for miles ahead, my drive almost entirely devoid of any signs of human activity. A few cars occasionally passed and every so often I would spot another church or small graveyard. Perhaps I am exaggerating a bit, but of all of Canada’s provinces, Saskatchewan seems to fall through the cracks of Explore Canada.

Saskatchewan is a landlocked province, far removed from the oceans. Extreme swings in temperature are the norm, with the region generally experiencing harsh winters and hot summers. It was not always like this however. Harkening back to approximately 390 million years ago, southern Saskatchewan was submerged in water, and the province sat adjacent to the equator. At some point, all of that water evaporated, and as the Earth aged, the seabed was covered over by sedimentary deposits.

That is a very simplified explanation of what happened, but it provides the fundamental reason for why there is such a huge stash of potash in Saskatchewan.

Potash in Saskatchewan can be likened to oil in Saudi Arabia. Vast and plentiful, and controlled by a select few. In potash’s case, the control rests with multi-billion dollar companies Potash Corp (POT), Agrium (AGU) and the Mosaic Company (MOS)

This oligopoly emerged and has endured, primarily because of the huge capital expenses necessary to develop a potash mine.

According to Potash Corp, approximately $3.2 billion is needed to develop a conventional two million tonne mine and mill in Saskatchewan. Add the costs of infrastructure needed for transportation and marketing, and the price tag rises to almost $5 billion.

Disregarding infrastructure, the breakdown on costs is 30% to mine development and 70% to facilities. Mines are prodigiously expensive because potash reserves are usually trapped 3,000 to 3,500 feet underground, where conventional mining techniques cannot be utilized.

Mining Methods

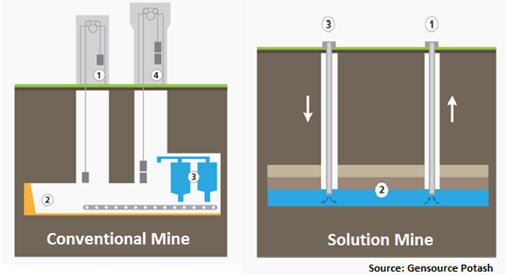

To access potash reserves, both conventional underground mining and solution mining is utilized. In conventional mining, the ore is mined like traditional mines and transported underground via conveyors. The ore is eventually hoisted up, where it is transported to a mill.

In solution mining, saltwater (brine) is injected into the potash-bearing rock, which dissolves the potash, leaving everything else intact. This ‘pregnant’ solution is then pumped out to surface to either a pond or crystallizers, where the potash is extracted.

Both methods come with unforgiving price tags. So this inevitable raises the question of why no other methods are used.

Saskatchewan Potash Controlled By Archaic Oligopoly

Simply put, the big players have invested far too much capital to consider changing their ways. Their operations are driven by a traditional model that incorporates several layers of distribution, much of which is frankly unnecessary. Since the industry is controlled by an oligopoly, investors do not care that older, more expensive technology is being utilized, so long as the producers continue to churn out cash.

Just look at the last time a potash mine came into operation:

It has been 45 years since a potash mine came into production in Saskatchewan. K+S is slated to have their 2 million tonne per annum Legacy Project come online soon, but costs for that project have ballooned to over $3 billion, and there are rumblings that costs will rise further.

This offers a prime reason why investors studiously avoid junior potash companies. No junior potash company in Saskatchewan has ever achieved commercial production; the only opportunity for success seems to be a sale to one of the industry behemoths.

However, this is exactly the type of contrarian opportunity we are on the hunt for. Maybe there are one or two companies who can grind it out and even get to production.

Bringing The Potash Sector Into The 21st Century

During our research, we came across Gensource Potash Corp (TSXV:GSP), a small potash company headed by Mike Ferguson, the man behind the development of Potash One’s Legacy Project, which was eventually acquired by K+S in 2010 for $427 million.

One of the first things we review when we look at exploration and development companies is the quality of the management team. Mike alone brings enough pedigree to give Gensource Potash Corp serious credibility in the marketplace; however, the company also recently brought aboard the rock star of potash (if there is one…), Dr. Mark Stauffer. We will leave it to you to do a quick google search on him, but his most recent accolade was serving as the Chairman of Allana Potash Corp, which was acquired by fertilizer giant Yara International for $110 million.

Mike Ferguson knows what it takes to work hard and develop a potash project in the traditional sense, and understands that it is near impossible in these markets to do so. However, Mike and his team are bringing a new technology to the fore, which could revolutionize the way potash is mined and extracted. This new technology, which is already proven and has been used in the United States, substantially decreases the amount of capital needed to develop a potash deposit, and gives Gensource the latitude to target smaller deposits that would normally be considered uneconomic.

Selective Dissolution

Selective dissolution evolved from solution mining, but features some key differences and employs newer technology that eliminates a lot of unnecessary layers and steps.

First, the selective dissolution utilizes horizontal drilling to create caverns where targeted potash exists. Then brackish ground water is used as the input, not fresh surface water as is applied in solution mining.

The brackish water is made into extraction brine, saturating it in salt, which dissolves the potash in the caverns. The brine is pumped out of the horizontal caverns to the surface, and through crystallization the potash is removed. The potash is dried for sale while the leftover brine is returned to the caverns to dissolve more potash; a cycle that is repeatable.

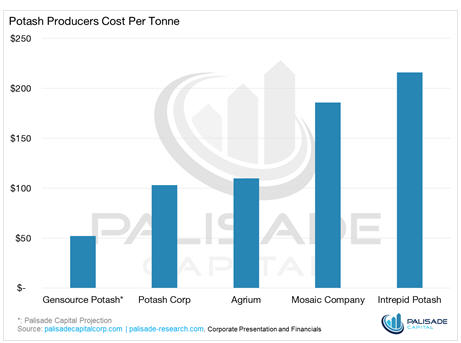

In addition to using brackish ground water, selective dissolution does not generate huge piles of salt by-product. The process eliminates the need for tailings and saves enormous amounts of energy compared to when evaporation-crystallization is used. All of this leads to substantially lower operating costs on a per tonne basis. Here’s the current landscape of producers after we crunched the numbers:

As mentioned previously, the older potash mines required significant capex to get started. The minimum production rates at the mines had to be above two million tonnes per annum to ensure that operations would be profitable. This has resulted in the construction of vast complexes, which typically take on the order of five to ten years to complete. Using selective dissolution, projects can return profits at just 250,000 tonnes per annum, with a development horizon of less than three years.

Gensource’s Lazlo Project and Business Plan

For all of the reasons mentioned above, capex for selective dissolution potash projects is a fraction of conventional mining and solution mining.

Gensource’s 100%-owned Lazlo Project has conditions that are perfect for selective dissolution. The property sits in the Davidson Sub-Basin, where the Legacy Project is located – obviously an area that Mike and his team are intimately familiar with. The Lazlo Area can support several projects, but Gensource’s initial project will have a design capacity of 250,000 tonnes per annum. Once a plant site is built, ‘satellite’ deposits can be easily integrated into the project at a fraction of start-up costs, meaning the company will be able to expand operations using existing cash flow.

Gensource is currently working on defining a formal 43-101, which will be backed into an internal ‘scoping’ study for a prefeasibility study in January 2016. First production is slated for the end of 2017, at a conservative price tag of $65 million.

Of special importance is the fact that Gensource has already secured an off-take agreement for 150,000 of the planned 250,000 tonnes per annum of production. This has boosted the company’s profile and attracted the notice of the larger players, but unfortunately it has not yet resulted in liquidity infusion. Our expectation is that the company, as it progresses through its studies, will garner more and more attention. At present, however, the company has a market capitalization of just C$8.4 million and is still an excellent, undervalued contrarian play.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments