Darnley Bay Resources: Bringing an old zinc district back to life

Darnley Bay’s Pine Point Project

Several zinc mines have shut down in the past few years due to depletion, and the warehouse inventory levels of the base metal have been steadily declining. The market is finally waking up and starting to look at zinc companies again. Thibaut Lepouttre of Caesars Report profiles Darnley Bay Resources, one of the companies hoping to fill the supply gap.

Source: Thibaut Lepouttre for The Gold Report

Darnley Bay Resources Ltd. (DBL:TSX.B) acquired a past-producing zinc asset in receivership and will publish a new PEA within the next few months.

Pine Point produced almost 10 billion pounds of zinc, and it hasn’t been mined out

In October of last year, Darnley Bay entered into an agreement with the court-appointed receiver of Tamerlane Ventures to take possession of the Pine Point zinc project, located less than 50 kilometers east of the Hay River in the Northwest Territories.

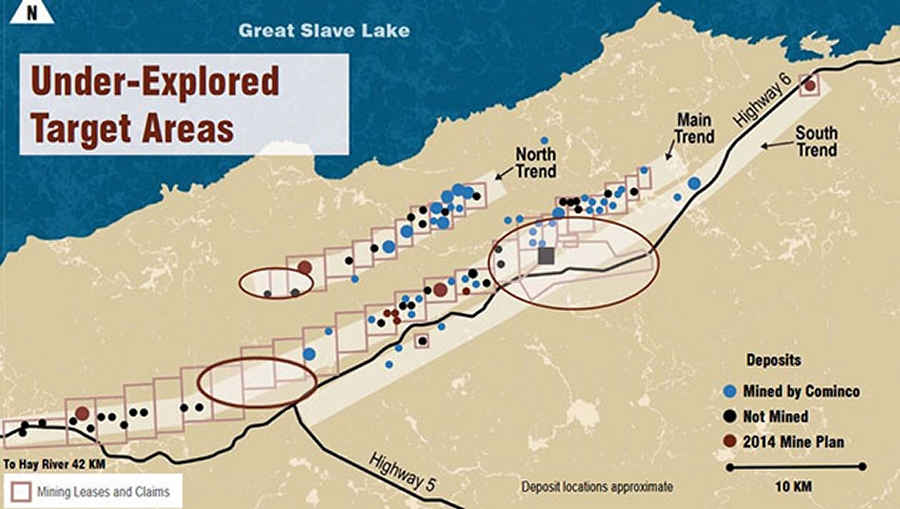

The project isn’t just one big zinc zone, but actually consists of in excess of 40 zinc-lead deposits over a total strike length of almost 70 kilometers. Of these deposits, ten have been the subject of an NI-43-101 report, compiled for Tamerlane Ventures, which owned the asset before going into receivership.

The acquisition terms are actually very straightforward—the receiver probably really wanted to get it off its books and recoup a part of the losses. Using a valuation of CA$0.20 per share, which is where Darnley Bay priced its most recent hard dollar private placement, Darnley Bay paid a total consideration of approximately CA$8M to acquire 100% of the asset in a mix of cash and stock.

Pine Point is a historic producer, and the district has been known for its zinc and lead assets for almost 100 years when Cominco started to explore the tenements before the Second World War and started to sink a shaft. The company discovered almost 100 different zinc-lead deposits, but it took until 1964 before large-scale production started after Cominco completed a resource estimate with 21.5 million tonnes of 11.2% ZnPb. And that’s a really good average grade!

As said, the project isn’t just one large pit, but Cominco actually started to mine 46 separate open pits, as well as two underground deposits, over a 35-kilometer long trend. In the 23 years after starting to mine in 1964, Cominco mined and processed a total of 64 million tonnes at an average grade of 7% zinc and just over 3% lead for a total zinc production of almost 10 billion pounds.

The Tamerlane PEA is outdated, but gives a good first impression

In 2014, Tamerlane Ventures commissioned an updated technical report on the Pine Point project that included a mine plan based on one underground and nine additional open-pit zones. The original plan was to truck a preconcentrated lead-zinc product from all these pits to the mill on the proposed processing site.

Cominco had drilled a total of 1.31 million (!) meters in almost 20,000 drill holes, so Tamerlane (and now Darnley Bay) have access to approximately $150M worth of drilling, which would have cost hundreds of millions of dollars in today’s world. This gives Darnley Bay a head start as it will now also be able to analyze the historical data searching for potential new pits that could now be economic at current zinc and lead prices.

Using a zinc price of $0.95/lb and a lead price of $1/lb, the after-tax NPV8% of the property, based on an 1,800-tonnes-per-day operating plan and a payability of 85% for the zinc and 95% for lead, came in at CA$112M.

Another important feature of Pine Point is the excellent quality of the zinc and lead concentrates. The 2014 study indicated the average lead grade in the lead concentrate would reach up to 72%, while the average zinc content in the zinc concentrate would be 62%. This would be absolutely fantastic, considering the accepted zinc levels for “clean” concentrates are 48–52%.

Delivering a 62% concentrate could result in a premium pricing, as it would allow the zinc smelters to blend the high-quality concentrate from Pine Point with lower value concentrates. For instance, Nevsun Resources Ltd. (NSU:TSX; NSU:NYSE.MKT) is still having issues to produce a generally accepted zinc concentrate, which sent its share price much lower. This really emphasizes how important it is to produce a quality zinc concentrate, and an end product with a 62% zinc grade would be highly sought after.

The main contributor to a higher net present value in the upcoming preliminary economic assessment (PEA) will be the cheaper Canadian dollar. Back in 2014, Tamerlane’s consultants used an USD/CAD exchange rate of 1.00 to calculate the economics of the property. With a current exchange rate of 1.30, some of the local costs will be much lower than in the 2014, while the recalculated NPV—keeping all other parameters unchanged—would increase from CA$112M to CA$145M.

Darnley Bay has a plan to control the potential water inflows

The main issue associated with the Pine Point deposits is the water inflow. The project is located just 10 kilometers from the Great Slave Lake, and Tamerlane researched several options to make sure the pits and underground mines don’t flood. Tamerlane has also drilled wells at several locations to test the groundwater flow, and engineering firm Thyssen confirmed to the company it should be able to control the water inflow.

Although Tamerlane originally planned to use a ground freezing technology, it changed that plan, and a plan to use grout technology is being investigated. This technology has improved rather substantially in the past decade and could be a huge help for Darnley Bay.

But in order to avoid the initial capital expenditures associated with using grout or ground freezing, Darnley Bay will very likely focus on the open pits. Not only will that be a cheaper path toward a meaningful production rate, it will also allow the company to start developing the underground deposits by using internally generated cash flow from the open-pit mining. Also keep in mind the planning and interpretation of the water flows has also greatly improved since mining started more than 50 years ago, and we would expect any strategy to control water flows to be much more efficient now.

The timeline from here on

It’s really important to know the R-190 underground deposit, as well as the mill, infrastructure and tailings area, has already been permitted, and this will allow Darnley Bay to hit the ground running.

The company has engaged JDS Engineering to complete a PEA, which should be ready within the next few weeks. This PEA will give us a first “tangible” overview of the up-to-date economics on the property.

The company has started to build a strong technical team, and has hired several key people. CEO Jamie Levy basically had to build the company from scratch and while we are sure this caused some headaches at the beginning, it allowed him to hire the people who could really help the project forward, rather than having to deal with “legacy management.”

The fresh start and clean slate also attracted Rob McEwen and Lukas Lundin to the story, who invested several million dollars into Darnley Bay Resources.

We would also expect the company to conduct some more drilling on the property and we’re looking forward to seeing the exploration plans for 2017. Darnley Bay raised CA$5M in flow-through funds in the December–January financing, and this cash will have to be spent on the ground this year. This should further boost the confidence in Pine Point as an asset, and pave the way to complete a feasibility study.

Conclusion

JDS Engineering is working hard to complete an updated preliminary economic assessment on the Pine Point zinc project. This new PEA will be completely different from the 2014 technical report due to the weaker Canadian dollar, the higher lead and zinc prices, as well as the extra deposits that could/will be added to the mine plan. According to the old PEA, the after-tax NPV8% at $1.15 zinc and $0.95 lead was estimated at US$194M, which would be in excess of CA$250M using today’s USD/CAD exchange rate.

That’s also the first target we would be aiming for, and should the updated PEA reveal an after-tax NPV8% of less than CA$250M (US$195M), we would be quite disappointed.

The PEA will be just the first step, and from then on it’s up to Jamie Levy and his team to create more value for Darnley Bay shareholders. With in excess of CA$5M in the bank, Darnley Bay remains well capitalized and should be able to make tremendous progress at Pine Point in 2017.

Thibaut Lepouttre is the editor of the Caesars Report, a newsletter and mining portal based in Belgium that covers several junior mining companies with a special focus on precious metals and base metals. Lepouttre has a Bachelor of Law degree and two economics masters degrees that have forged his analytical approach to the mining sector. Considered a number cruncher, Lepouttre focuses on the valuations of companies and is consistently on the lookout for the next undervalued mining company.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure:

- Thibaut Lepouttre: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Darnley Bay Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector.

- The following companies mentioned in this article are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

- Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

- This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

- From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview/article until after it publishes.If you would like to comment on the content of this article or any of the companies discussed in this article, or if you would like to be interviewed by The Gold Report, please contact Melissa Farley of The Gold Report at [email protected], 707-981-8999 ext 334.

IMPORTANT DISCLOSURES

The Gold Report, The Energy Report, The Life Sciences Report and Streetwise Reports do not render general or specific investment advice and do not endorse or recommend the business, products, services or securities of any industry or company mentioned in this report.

From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the “Learn More About Companies in this Issue” section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

OTHER DISCLOSURES

Streetwise – The Gold Report, The Energy Report, The Life Sciences Report and Streetwise Reports are Copyright © 2017 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments