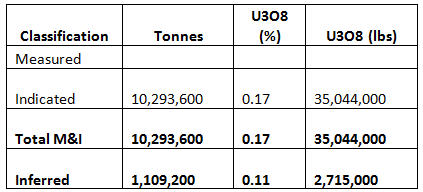

Current uranium market fundamentals strong – future is even brighter

With Japan finally restarting some of its nuclear reactor fleet (two reactors have come online since August) and China continuing its breakneck reactor build-out (with 29 reactors in operation and 22 under construction), the one commodity in the natural resource space that is actually carrying some positive fundamentals today is uranium.

Bloomberg recently noted that the bonds of at least two uranium producers, Cameco Corp. (CCJ, TSX:CCO) and Uranium One Inc., have been kind to investors, “…demand for nuclear power comes roaring back from the Fukushima disaster, powering the bonds of Canadian uranium producers to top returns among their beleaguered commodity peers”.

China is far from alone in its quest to expand reactor capacity. According to the World Nuclear Association, there are currently more than 60 reactors under construction worldwide, across 15 different countries. Russia and India both currently have six reactors under construction; the United States has five, South Korea has four, and the United Arab Emirates also has four. Even Saudi Arabia, the oil behemoth of the world, is getting into the nuclear power game. The Saudis are planning to construct 16 nuclear power reactors over the next 20 years, at a cost of more than $80 billion. The first reactor is expected to come online by 2022.

As this global build-out in nuclear reactors continues, competition for the primary supply of the base material for the nuclear fuel component, “U3O8”, is set to heat up.

To secure primary uranium supply and deliver on its long-term contracts with the big global utilities, Cameco will have to face off with corporations backed directly by the governments of the some of the most powerful countries on earth.

Uranium One, for example, is owned by Rosatom, an entity controlled by the Russian government. The export of nuclear goods and services is a major pillar of Russia’s economic and policy objectives; there are over 20 nuclear power reactors either confirmed or planned for export construction.

Meanwhile, the quasi state-controlled French outfit, AREVA (ARVCF, EPA:AREVA), recently announced a major investment into the company by China National Nuclear Corporation (CNNC). CNNC International, a major subsidiary of CNNC, is also said to be on the lookout for assets in Australia, Canada, and Kazakhstan.

The global build-out in nuclear reactors is going to cause a lot of jockeying for position between many countries, utilities, and other organizations. With each new standard 1GW nuclear reactor consuming, on average, 400,000 lbs of U308 annually, the need to obtain critical long-term uranium supplies for nuclear fleets will unleash a scramble among planners to secure high-quality uranium ore bodies in safe political jurisdictions for future development.

Canada hosts the highest-grade uranium deposits in the world. To put this in proper perspective, let’s take a look at Cameco’s McArthur River mine. The average grade of the reserves at McArthur River is 14.87%, which equates to $10,600 per ton – that is the functional equivalent of having 9.75 ounces per ton of gold at current spot prices. That figure would be almost 6 times greater than the highest-grade gold mine in the world.

In light of the recent macro news, Uranium Investing News put together a “Top 5 List” based on the largest uranium deposits, at a single property, where a Canadian junior company holds a majority interest in the project. The rankings take into account the grade of each deposit and the contained pounds of U308 present therein, based on published NI 43-101 mineral resource estimates.

The Top 5 were:

Resource:

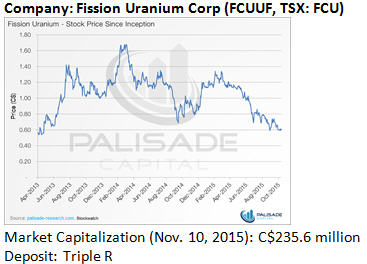

While Fission Uranium and Denison Mines cancelled their proposed merger, the deal did shed some light on how uranium in the Basin is currently being valued. Had the deal closed, Denison would have issued 1.26 shares for each Fission share, implying a value of C$424 million or ~$3.00/lb. This is significantly less than the average of $9.00/lb settled upon for the three most recent transactions in the Basin: Rio Tinto’s acquisition of Hathor Exploration in 2012, Cameco acquiring majority ownership of the Millennium project in 2012, and Denison acquiring Fission Energy in 2013.

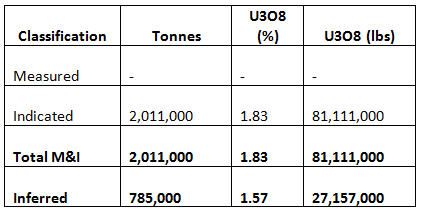

The Triple R deposit is the second largest undeveloped uranium deposit in the Athabasca Basin. Fission Uranium recently completed a Preliminary Economic Study (PEA) for the project, highlighted by a projected OPEX of USD$14.02/lb. Triple R has the potential to be the lowest cost source of uranium in the world.

Wheeler River is Denison’s flagship exploration property and is home to the Phoenix deposit and the Gryphon zone. The project contains many high priority exploration target areas, the most important of which are the unconformity and basement targets in the Gryphon area. Wheeler River is the largest undeveloped project in the Basin and consists of 19 mineral claims totaling 11,720 hectares in northern Saskatchewan. Denison has 60% interest in the JV and has been the operator since November 10, 2004. The other partners are Cameco (30%) and JCU (10%). A PEA is currently underway for the project, and with the inclusion of its newer discovery, Gryphon, Denison should soon be able to boast about greatly improved economics.

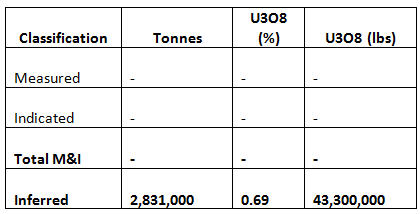

Kivalliq’s flagship project is the 100% owned Angilak Property in Nunavut. Since acquiring the Angilak Property in 2008, Kivalliq has invested $55 million into the project.

Like Wheeler River, it appears Angilak should be host to multiple discoveries, with noteworthy results from soil samples at the RIB Trend. Recent Dipole holes indicate anomalies and basement-hosted uranium mineralization, further confirming that Dipole-RIB Trend deserves more drilling. Kivalliq’s YAT target, located in between Lac 50 and Dipole, has also returned significant samples. In any other market, Kivalliq would have multiple drills going.

The company has been flying under the radar primarily due to its location; however, the pounds in the ground do not lie. Accompanied by management’s commitment to finding and advancing discoveries, Kivalliq comes with the greatest optionality among its peers.

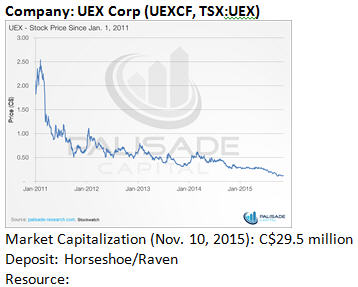

Horseshoe and Raven are located in the Hidden Bay property, which is the seventh largest undeveloped uranium resource in the Athabasca Basin. According to its PEA, Hidden Bay’s base case scenario (US$60/lb uranium) would yield an estimated C$246 million in EBITDA.

The property also enjoys its close proximity to milling facilities operated by Cameco and AREVA, which would significantly reduce the capital requirements of the project if a toll milling agreement can be reached. In addition to the known deposits at Hidden Bay, several other brownfields exploration targets have emerged that are currently being explored.

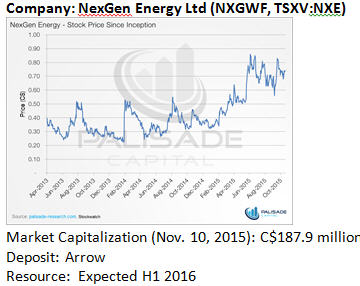

Company: NexGen Energy Ltd (NXGWF, TSXV:NXE)

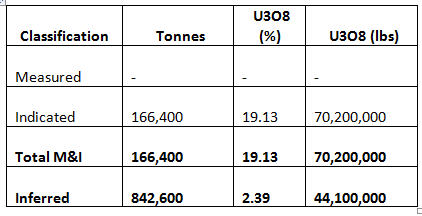

NexGen Energy’s flagship projects are Radio and Rook 1, both highly prospective and garnering significant market attention. The 100%-owned Rook 1 is home to the Arrow Zone discovery which is along the strike of Fission’s Triple R deposit. Through exploration and drilling, Arrow has shown some of the highest grades and thickest intercepts in Saskatchewan.

Conclusion

Savvy investors are accumulating positions in uranium-oriented stocks now. As the spot price of U308 moves past US$45/lb, the herd of the unwashed masses will follow.

Earlier in this article we mentioned the term optionality, which is the upside potential of an asset based on the appreciation of the underlying commodity price. In addition, the possibility for more discoveries through exploration provides a very strong added catalyst for these stocks.

We would like to highlight two companies with great optionality: Fission Uranium and Kivalliq Energy. Fission Uranium’s stock price has been floundering since the cancellation of its merger, trading at $1.63/lb. Considering the takeout was priced at $3.00/lb, investors are selling because they no longer see a viable exit via acquisition. The company should have enough flow-through dollars to fund its winter exploration and, for us, it is business as usual. Chairman and CEO, Dev Randhawa, will persevere and continue to prove up the project and create value for his shareholders.

Kivalliq Energy is another company with strong fundamentals and trading at a significant discount. Led by Jim Paterson, the company is only being awarded a market capitalization of $0.30/lb. The company also has strong exposure to the Athabasca Basin, owing to its interest in the Hatchet Lake Project and Genesis Property.

Even in this difficult bear market, Jim Paterson and company are soldiering on and aiming for multiple discoveries at the Angilak Property. We believe that Kivalliq is the company that will benefit the most from an increase in uranium price.

Lastly, we like following the ‘smart money’. Kivalliq has a sophisticated investor base, with Ross Beaty’s Kestrel Holdings owning ~14% of the company’s outstanding shares. As one of the mining sector’s most prolific and successful investors, Ross Beaty is not someone to be ignored. Ross is the founder of Pan American Silver Corp.; additionally, he was the second-largest shareholder in Augusta Resources, acquired by Hudbay Minerals last year for $555M, and he served as the chairman of Lumina Copper, which was acquired by First Quantum for a sum of $470M.

Disclosure:

Disclosure: We are long Kivalliq Energy

We were not paid by any of these companies to write this report, but we work with Kivalliq Energy in a merchant banking capacity and we stand to benefit from any volume this report stands to generate. The information contained in such publications is not intended as individual investment advice and is not designed to meet your personal financial situation.

Information contained in this report is obtained from sources we believe to be reliable, but its accuracy cannot be guaranteed. The opinions expressed in this report are those of Palisade Capital and are subject to change without notice. The information in this report may become outdated and there is no obligation to update any such information.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments