Column: Zinc turbulent as low stocks clash with expected surplus

Zinc’s early-year rally has quickly fizzled out as the market prices in a looming supply surge.

London Metal Exchange (LME) three-month metal rose 16% to a five-month peak of $3,512 in late January but has since tumbled all the way back to $3,040, just 1% higher than it was at the start of the year.

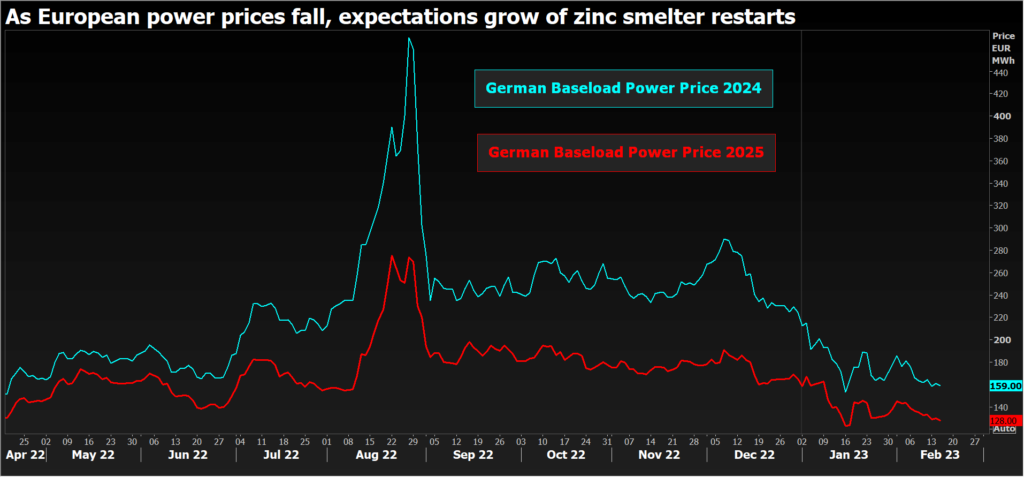

With Europe’s winter energy crisis abating and power prices falling, there are growing expectations that idled zinc smelter capacity will restart.

Chinese smelters are also powering up capacity thanks to abundant supplies of raw materials and the resulting healthy processing fees.

The abrupt price turnaround this month is the market reassessing the potential for a significant supply recovery and a return to zinc surplus after two years of shortfall.

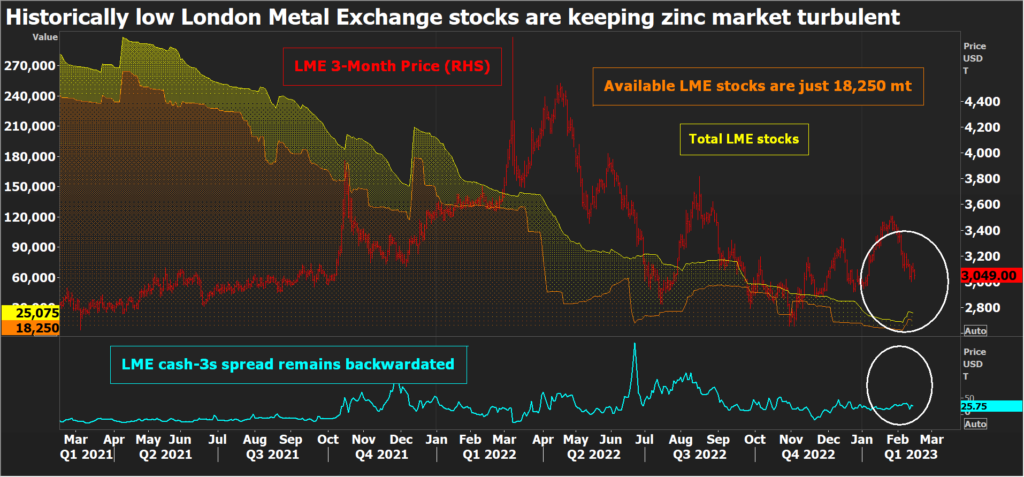

LME short position holders could really do with seeing some of that surplus now. Exchange inventory remains extremely low resulting in persistent time-spread turbulence.

The disconnect between cash-date reality and future expectations is likely to persist until there is a meaningful rebuild in exchange stocks.

Turbulent tom

The LME’s arcane tom-next spread , which is what a short pays for rolling their position from tomorrow to the next day, is the epicenter of the current rolling squeeze.

“Tom” has turned unruly since the start of February, trading out to a backwardation of $16 per tonne last week, the tightest the spread’s been since last October.

The premium might be wider still were it not for the controls imposed on all the LME’s deliverable contracts in the wake of last year’s nickel meltdown.

Tom-next is subject to a daily backwardation limit, set at 1% of the previous day’s cash settlement price, which is helping keep the full cash-to-three-months backwardation contained at around $30 per tonne.

The LME’s rolling cash date is currently a congested area. The exchange’s latest positioning report shows four dominant long positions on cash zinc as of Monday. Combined they accounted for a minimum 200% of available stocks.

One entity controlled 40-50% of actual on-warrant inventory.

All of which serves to underline just how depleted LME zinc stocks are.

Stocked out

LME zinc stocks total just 25,075 tonnes, less than one day’s worth of global consumption. On-warrant stocks, against which dominant positions are measured, stand at 18,250 tonnes.

There has been a mini rebuild over the last few days with the cash squeeze drawing in 11,575 tonnes of metal at LME warehouses in Singapore.

There may be more lurking in the warehousing shadows. The exchange’s monthly off-warrant stocks report showed 37,526 tonnes of shadow zinc inventory in Singapore at the end of December.

This is metal that is being stored with the contractual option of LME warranting, meaning it is the most likely source of last week’s inflows with more potentially available for delivery.

However, total LME inventory – both registered and shadow – was still just 68,115 tonnes at the end of December, down by 154,673 tonnes on the year and a far cry from the early 2010s, when LME stocks were consistently over 800,000 tonnes.

Consecutive years of supply deficit have drained the zinc bank, particularly in Europe, which has seen multiple capacity curtailments by smelters struggling with high power prices.

There is zero registered zinc at LME warehouses in Europe. Nor was there any off-warrant metal as of last December.

European smelter restarts

Europe remains the point of maximum global supply-chain tightness.

Physical premiums have softened slightly due to weaker demand and better availability of non-European metal, according to Fastmarkets. But Northern European premiums are still hovering around $500 per tonne over LME cash and Italian consumers are paying a range of $550-600 for the delivery of duty-paid zinc.

High European power prices have caused the idling of three zinc smelters with combined capacity of around 465,000 tonnes and led to many others operating at reduced rates.

However, the regional energy market appears to have weathered its winter crisis with baseload prices a long way off their August highs.

European smelter margins have turned positive again, according to Citi, which calculates a positive cash margin of around $250 per tonne for a typical operator, compared with a net loss of $840 at the power price peak in August. (“Metal Matters,” Jan. 18, 2023)

The bank now thinks the market is pricing in significant smelter restarts sooner rather than later and has just downgraded its short-term zinc price forecast to $2,900 from $3,500 per tonne. (“Metal Matters, Feb. 15, 2023)

Citi is forecasting a modest supply surplus of 70,000 tonnes this year, compared with a Reuters poll median forecast for a small 19,500-tonne supply deficit.

Everything hinges on how much European supply returns and when.

Any excess production, however, will take time to make its way to the market of last resort. LME zinc pricing is going to remain volatile for a while yet as shorts betting on a return to surplus have to navigate today’s low-stock reality.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Kirsten Donovan)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments