Vale’s reality check for nickel’s electric vehicle dreams: Andy Home

LONDON, Dec 12 (Reuters) – Nickel is one of the materials expected to win from the coming electric vehicle (EV) revolution.

Electric vehicles will be powered by lithium-ion batteries, which need cobalt and nickel. Indeed, as cobalt’s potentially fragile supply chain comes under ever-increasing scrutiny, battery-makers are likely to try to use less of the stuff in favour of more nickel.

So it might seem strange that the world’s largest nickel producer is actively curtailing capacity at mines and refineries.

Yet that is precisely what Brazil’s Vale is doing, removing around 100,000 tonnes of supply over the next two years.

While “everyone knows there are great opportunities” for nickel in the EV sector, “prices are not there”, according to Vale Chief Executive Fabio Schvartsman, speaking at an investor event last week.

It’s a wake-up call for the nickel sector. The future may be electric and bright, but the present reality is a dull one of low prices and legacy stock overhang.

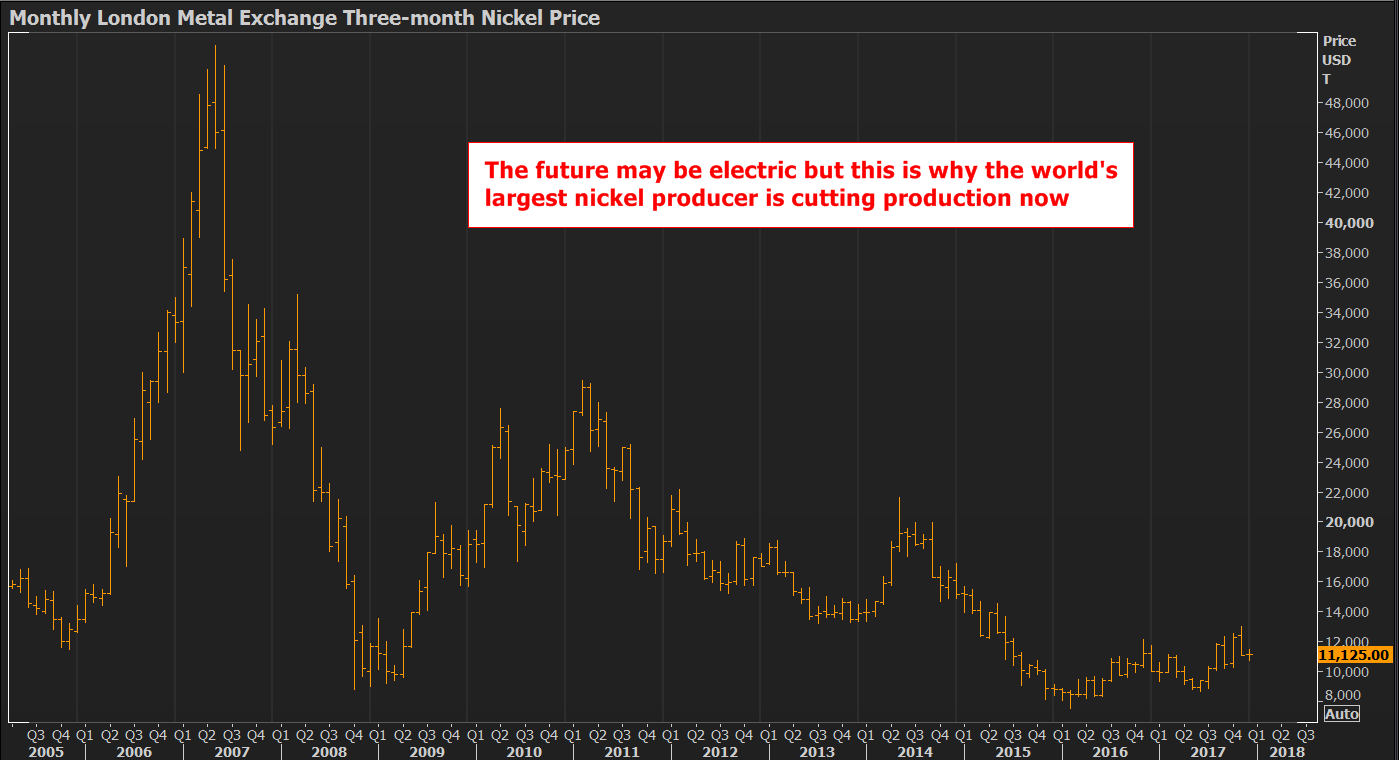

Graphic on LME nickel price 2005-2017

The weight of past exuberance

The prices of lithium and cobalt have gone stratospheric over the last year or so as supply chains struggled to catch up with the new demand driver that is the EV.

It took a while for the world to realise that nickel was the third key metallic input into the new generation of batteries, but when it did, last month, the nickel price jumped to a two-year high of $13,030 per tonne on the London Metal Exchange (LME).

The market has since given back some of that initial exuberance with LME three-month metal currently trading around $11,100 per tonne.

But historical context is everything in this market.

It’s a wake-up call for the nickel sector. The future may be electric and bright, but the present reality is a dull one of low prices and legacy stock overhang.

Just over three years ago nickel was trading above $20,000 per tonne. Six years ago it was close to $30,000 and 10 years ago, the nickel price peaked at over $50,000 per tonne.

The flip side of that extraordinary bull market of 2006-2007 was a surge in supply, both conventional from existing producers such as Vale and unconventional in the form of China’s development of new nickel-pig-iron production technology.

The nickel market has been living with the consequences of overproduction, high stocks and low pricing ever since.

The International Nickel Study Group estimates the global refined nickel market is on course to register a second consecutive year of supply deficit after last year’s 44,000-tonne shortfall.

But the cumulative surplus over the 2012-2015 period was almost 500,000 tonnes.

That’s why LME stocks are still so large.

Despite a lot of daily “noise” and an underlying rotation of the type of nickel stored in LME warehouses, the headline figure of 375,564 tonnes is barely changed on the start of the year.

And the LME price is still at levels that are causing real pain for even the world’s largest producer.

Two of its core six nickel production units will have cash costs above $10,000 per tonne this year, even including by-product credits.

Taking the lead – belatedly

That is about to change.

“Each and every asset must be cash-flow positive at low nickel prices,” according to Jennifer Maki, executive officer of Vale’s base metals division.

This statement of intent translates into an overhaul of its nickel business, leading to a dramatic reduction in projected 2018 output from a forecast 308,000 tonnes this time last year to a revised 263,000 tonnes.

The nickel market has been living with the consequences of overproduction…

Two Canadian mines have already been placed on care and maintenance, namely Stobie in its Sudbury operations in Ontario and Birchtree in Manitoba.

A nickel refinery in Taiwan is also going onto care and maintenance, while another smelter-refinery will close in Manitoba next year.

The aim is to reduce costs and balance future investment against market conditions.

It’s precisely the sort of producer leadership that has been lacking in the nickel market, which is another reason why the price has yet to stage any sustainable recovery.

True, Vale’s leadership role has been thrust upon it by market reality and its new focus on cost discipline is arguably a couple of years too late.

Bear in mind that Glencore’s similar action in the zinc market, mothballing around 500,000 tonnes per year of mine supply, has been running for two years.

But for the nickel market, it’s a case of better late than never.

Testing the EV story

None of which negates the positive narrative around future nickel usage growth in the battery sector.

Emphasis on the word “future” in that sentence. Right now, nickel’s fortunes are still beholden first and foremost to its usage as an alloying agent in stainless steel.

The amount of nickel absorbed into EV battery production will undoubtedly grow, although as with everything in the EV story, there are as many forecasts as to how much as there are analysts.

Vale argues that it is keeping optionality in its nickel portfolio by producing less in the current low-price environment so it can produce more when demand and price recover.

If that sounds familiar, it’s because Glencore Chief Executive Ivan Glasenberg was saying something very similar just prior to shutting zinc mine capacity at the end of 2015.

In the interim, Vale is going to give us all an interesting experiment in just what the EV story means for nickel.

One of its most problematic operations is that in New Caledonia.

Planned and built in the immediate aftermath of that 2006-2007 price spike, what was once known as the Goro project came on stream years late and over budget and has been struggling to achieve nameplate capacity ever since. Cash costs this year are expected to come in at $10,153 per tonne.

Now Vale needs to invest another $500 million in the project and is looking for a joint-venture partner to help. Added incentive comes in the form of the cobalt Goro produces as a by-product.

The company has received “good interest” in a potential stake, according to CEO Schvartsman.

But, as he added, “the proof of the pudding is in the eating”.

“We are going to see if the market really believes if nickel is something that is important for the future of EVs.” Will all the future promise “translate into someone who is eager to invest with us to have more nickel in the future”?

It’s a good question.

Vale and the rest of us will find out the answer soon enough.

Without a new partner, this symbol of previous nickel price exuberance looks set to follow other parts of Vale’s nickel business into care and maintenance.

Column by Andy Home

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments