Column: LME’s Russian aluminum dilemma set to become more acute

The London Metal Exchange (LME) is coming under renewed pressure to exclude Russian aluminum from its warehouse system.

Norwegian producer Norsk Hydro has called for the exchange to reconsider its decision last November to continue accepting deliveries of Russian metal.

With Russian brands accounting for 80% of warranted aluminum stocks at the end of June, the LME contract is at risk of losing its benchmark status, Hydro warned.

There are no government sanctions on Russian aluminum and the LME said in response that “we note that all metals of Russian origin continue to be consumed by a broad section of the market.”

Russian producer Rusal has also hit back with its own warning that excluding its brands from the LME would be “highly destructive” to the market structure.

The company said it “continues to witness a broad acceptance of its low-carbon aluminum to a wide range of global consumers from across the world.”

The problem for Rusal and the LME is that one of the biggest consumers – China – may be losing its appetite.

The market of first resort

Although there are no official sanctions against Rusal, the company’s geographical sales mix has shifted in response to punitive import duties in the United States and self-sanctioning by some consumers, particularly in Europe.

Some metal has indeed been delivered to the LME as the market of last resort but inflows have so far been modest.

LME warranted stocks of Russian metal amounted to 218,000 metric tons at the end of June, which is small relative to Rusal’s four-million-ton per year production capacity.

That suggests that Rusal and its trading partners have been largely successful in redirecting shipments to consumers in Asia, particularly China.

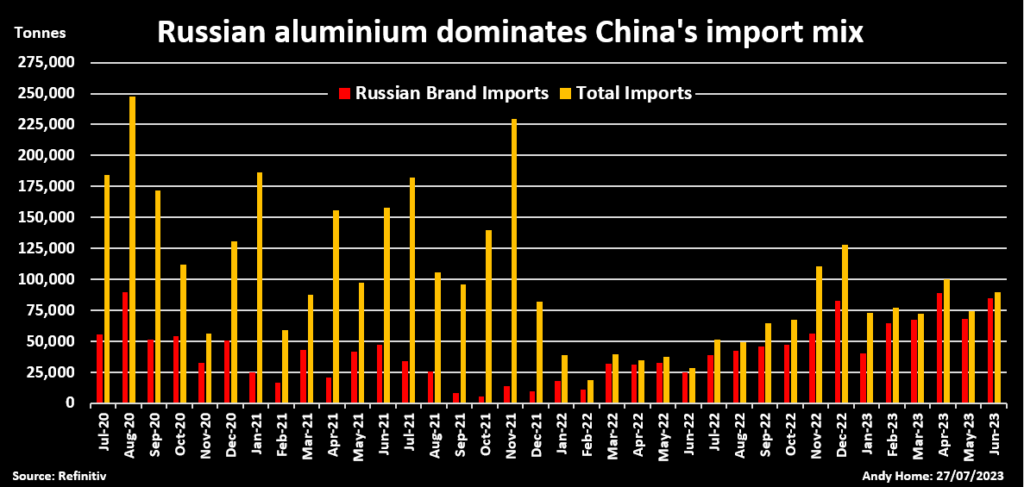

China imported 462,000 metric tons of Russian-brand primary aluminum last year, up from 291,000 metric tons in 2021. The pace has accelerated over the first half of this year, imports of Russian metal jumping by 177% year-on-year to 414,000 metric tons.

Indeed, Russian brands accounted for 85% of China’s total primary metal imports in the January-June period.

The country has emerged as the market of first resort for Russian metal since the invasion of Ukraine in February 2022.

Reverse flow

There are signs that China’s appetite for Russian aluminum, or indeed any primary metal, is now fading.

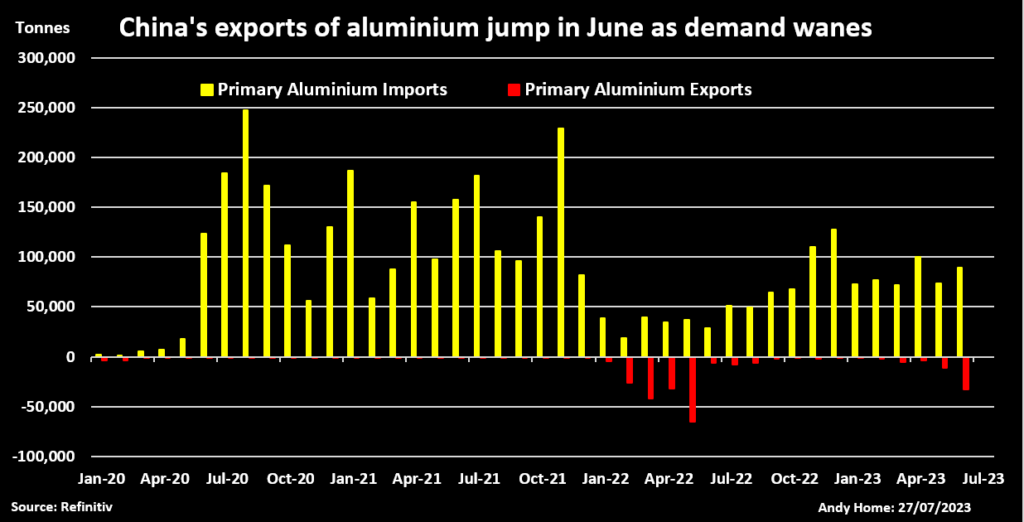

China exported 33,000 metric tons of primary aluminum in June, more than it exported over the first five months combined and the largest single-month tally since May 2022.

China’s tax structure works against direct exports by the country’s smelters, meaning there is a high probability that June’s outbound flows reflected a turnaround of metal that had been imported only as far as the country’s bonded warehouses.

It’s a curiosity of China’s trade statistics that movement into and out of bonded warehouses shows up as imports and exports respectively.

Analysts at Goldman Sachs note that “feedback from traders” suggests that some 175,000 metric tons of “imports” this year have been placed in the bonded zone rather than being moved into the onshore market. (“Metals: What’s going on?”, July 21, 2023)

Given China’s import mix in recent months, there is a high probability that any metal now leaving bonded warehouses is Russian brand.

The top two destinations for June’s “exports” were Japan (10,000 metric tons) and South Korea (20,500 metric tons).

The South Korean flow is worth noting. LME warehouses in the port of Gwangyang have so far received the lion’s share of Russian-brand deliveries onto LME warrant.

China cranks up production

June’s so-called exports may turn out to be a blip but there is good reason to think not.

China was running short of commodity-grade aluminum in the first months of the year as drought in hydro-rich Yunnan province led to power rationing and smelter curtailments.

China’s aluminum run-rate fell by an annualized 636,000 metric tons over the first quarter, according to the International Aluminium Institute.

Moreover, the country’s aluminum smelters delivered more metal in molten rather than in ingot form. First-half production of ingot slid by 9% from year-earlier levels, according to consultancy AZ Global.

The combination of lower outright production and a higher ratio of hot-metal deliveries served to tighten up the hard-metal part of the supply chain, incentivizing imports from the rest of the world.

However, as drought conditions ease in the south of the country, national production has come roaring back to the tune of a 750,000-metric ton annualized increase over the second quarter.

The rebound in production is not being matched by any similar pick-up in usage. China’s demand for aluminum and most other industrial metals has failed to live up to expectations this year with manufacturing activity contracting and the troubled property sector still flat-lining.

The reverse flow of aluminum in the June data suggests a shift from onshore shortfall to surplus may already be materializing.

More LME deliveries?

If so, there is a double risk that China’s imports of Russian metal tail off and some of the units already sitting in the country’s bonded zones get redirected to other markets.

How easily they can be absorbed is a moot point.

Apart from the issue of who is and who isn’t prepared to accept Russian metal, aluminum demand is weakening just about everywhere as higher inflation mutes construction activity and automotive sales.

It’s why the LME three-month aluminum price sank to a year’s low of $2,127 per metric ton earlier this month and why it remains stuck near the bottom end of its recent range, last trading at $2,210 per metric ton.

Time-spreads are super loose, the benchmark cash-to-three-months period trading in a wide contango of $40 per metric ton.

Both outright price and spreads suggest there is surplus aluminum on its way to the LME system.

The LME can only hope that not too much of it is Russian, if it is to avoid being caught in the middle of an increasingly polarized aluminum industry.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Jane Merriman)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments