Column: Another Yunnan power blow to China’s aluminum output

The Chinese province of Yunnan has ordered its aluminum smelters to take another round of production cuts to stabilize power supplies.

The province’s hydro-electric grid has struggled with prolonged drought and low reservoir levels.

Power-hungry aluminum producers in Yunnan and neighboring provinces were already operating at reduced capacity, some of them since September, dragging down China’s national output.

The latest cuts will impact around 740,000 tonnes of annual production capacity, adding to the million tonnes already offline, according to industry consultancy Mysteel.

The aluminum market has taken the news in its stride. London Metal Exchange (LME) three-month metal has edged up to a current $2,465.00 per tonne but is a way off January’s high of $2,679.50.

Right now the market can take a relaxed view of Yunnan’s problems with visible inventory accumulating on both the London markets and in China.

But with Chinese demand expected to enjoy a strong post-holiday, post-covid bounce, that could change very quickly.

More power woes

Yunnan has become a major aluminum hub in recent years as Chinese operators have relocated from coal-powered provinces to lower their carbon footprint.

Aluminum capacity has grown to around 5.25 million tonnes, making it the fourth largest provincial producer after Shandong, Inner Mongolia and Xinjiang.

On paper Yunnan can churn out as much metal as North and Latin America combined, but only if there is sufficient power to feed smelters’ electrolysis production lines.

After the latest mandated curtailments, operating capacity in the province will fall to below 3.30 million tonnes, according to analysts at Citi.

Combined with rolling power restrictions in neighboring Guizhou and Sichuan provinces, also largely hydro-powered, the cumulative impact will be a fall in China’s annualized operating rate to below 40 million tonnes for the first time since March 2022, the bank said. (“Metal Matters,” Feb. 21, 2023)

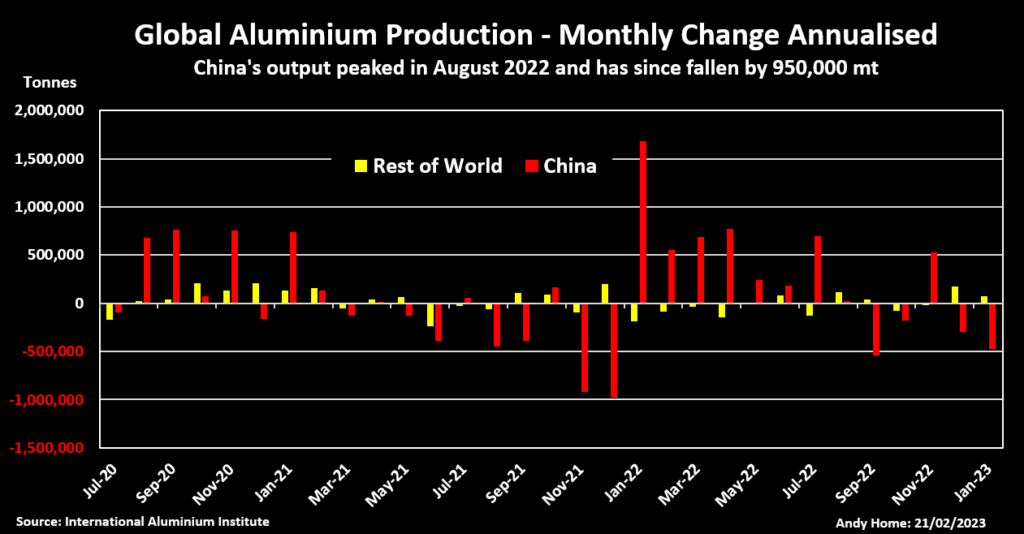

Annualized output in China, the world’s largest producer of aluminum, peaked at 41.46 million tonnes in August last year, according to the International Aluminium Institute (IAI).

January’s estimated annualized production was 40.50 million tonnes, a drop of almost one million tonnes over the last five months.

China’s monthly production figures have been volatile, reflecting the interplay of capacity curtailments, restarts of smelters hit by previous rounds of power rationing and new capacity coming online.

However, it is evident the rolling power crunch in the Yunnan-Guizhou-Sichuan production hub has dragged on national output and the impact is likely to increase as more capacity is ordered offline.

Stocks cushion…for now

The price reaction to Yunnan’s latest drought has been muted on both the London market and the Shanghai Futures Exchange (ShFE).

Registered inventory on both exchanges has risen fast, cushioning the supply chain from the loss of Chinese production momentum.

LME warehouses have registered 237,325 tonnes of inflow so far this month, bringing the headline stocks total to 581,300 tonnes, up by 134,050 tonnes or 30% on the start of the year.

Europe’s industrial sector continues to contract even as the services sector recovers and weakness in end-use markets has been accentuated by a destocking cycle along the aluminum supply chain.

China, meanwhile, is emerging from the seasonal lull in downstream activity over the Lunar New Year holidays and ShFE stocks have mushroomed from 95,881 tonnes at the end of December to 291,416 tonnes.

That is still below last year’s seasonal peak of 348,315 tonnes in early March and could quickly disappear if Chinese demand recovers as expected.

Indeed, Citi’s view is that aluminum offers the best China recovery trade among the base metals over the next three months. The bank’s short-term price forecast is $2,700 per tonne with upside potential to $3,000.

Goldman Sachs is also in the bull camp, forecasting an average price of $3,125 per tonne this year as Chinese demand recovery collides with domestic production constraints. (“Aluminum: Reopening Deficit,” Jan. 15 2023).

Green dilemma

Everything, depends on how long power rationing will last in Yunnan and its neighbors.

The rainy season will only start in May and it is possible, Citi says, that the transition from El Nina to El Nino weather patterns in the Pacific will mean more drought trouble for southwest China.

That could delay smelter restarts or even lead to further cuts.

Aluminum smelters in Yunnan compete with other power-hungry sectors such as silicon, which has also seen producers relocate capacity to the “green” south.

All industrial sectors have to vie with Yunnan’s obligations under China’s East-West Power Transmission Project, which means that exports to other regions sometimes take priority over internal requirements.

Too much green industry is chasing too little green power straining regional grid dynamics.

The answer is more green power in the form of solar not hydro. Solar generation capacity will dominate Yunnan’s new power installations over the next couple of years, according to Citi.

“We expect Yunnan’s power supply to gradually stabilize in the next 2-3 years not because of the climate but with the help of more renewable power to come,” the bank said.

Until then, a metal critical to future decarbonization is increasingly vulnerable to the changing weather patterns associated with global warming.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Barbara Lewis)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments