The company, which plunged the most in 15 months on Friday, extracts all of its coal from the Powder River Basin of Wyoming and Montana. Unlike some rivals, it sells exclusively to electricity generators. And despite White House efforts to roll back regulations to boost the industry, Cloud Peak faces the daunting task of keeping enough power-plant customers amid the onslaught of competition from cheap natural gas and the growth of wind and solar power.

On Thursday, Cloud Peak projected 2018 earnings of $75 million to $100 million before interest, taxes, depreciation and amortization — a measure of profitability watched closely by analysts. That’s below the $116 million estimate from Jeremy Sussman of Clarksons Platou Securities. Among the company’s headaches: it expects mining costs to keep on rising because it has to remove more and more earth to get to the coal in its massive, open-pit mines.

“We will obviously do everything we can to manage costs across the organization,” Cloud Peak Chief Executive Officer Colin Marshall said on a call with analysts.

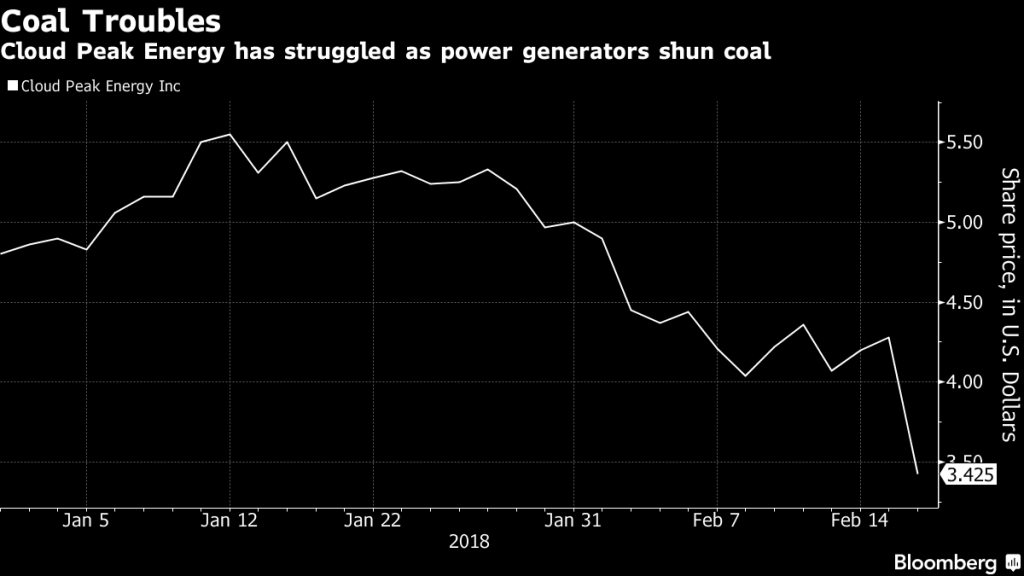

Nonetheless, shares fell as much as 24 percent on Friday, the most intraday since November 2016. They were trading at $3.39 as of 3:51 p.m. in New York.

The big problem for Cloud Peak and fellow miners is there are fewer and fewer customers. Between the end of 2011 and 2017, America’s coal-fired power plants lost 15 percent of their generating capacity, from 306 gigawatts to 261 gigawatts. Another 12.5 gigawatts of plants are scheduled to close this year, making 2018 potentially the second-biggest year on record for retirements, according to Bloomberg New Energy Finance analyst Colleen Regan.

On Friday, FirstEnergy Corp. added to the pain, announcing plans to sell or shutter its 1.3-gigawatt Pleasants Power Station in West Virginia by 2019.

What’s more, Could Peak can’t really benefit from the industry’s brightest spot of the past year: metallurgical coal. Rivals including Arch Coal Inc. and Peabody Energy Corp. that dig up that variety of coal — which is used in steelmaking and found, among other places, in Appalachia and Australia — have felt a boost thanks to strong demand from China and other international markets. Arch has climbed about 30 percent in the past 10 months and Peabody has gained more than 70 percent in the 10 months.

Met coal

Those moves are “definitely all about met coal,” Sussman said by email.

Metallurgical coal, however, offers limited upside. Of the 785 million tons of coal dug up in the U.S. in 2017, only 7.6 percent of it was metallurgical, according to Andrew Cosgrove of Bloomberg Intelligence.

Cloud Peak, which offers only thermal coal, is down almost 20 percent in the last 10 months. Similarly, Foresight Energy LP is down more than 30 percent and Alliance Resource Partners LP, which sells primarily thermal coal, is down 17 percent.

Against that backdrop, Cloud Peak on Thursday posted fourth-quarter adjusted Ebitda of $19 million, missing the $25.3 million average of seven analysts’ estimates compiled by Bloomberg. It also said that a new credit facility would be “significantly smaller” than its $400 million one that matures in February 2019.

MKM Partners analyst Daniel Scott lowered his earnings estimates for Cloud Peak for both 2018 and 2019. He also reduced his price target for shares — he has the equivalent of a hold rating — to $4 from $4.50, citing the “difficult thermal coal environment.”

“We stay on the sidelines while we wait for domestic thermal coal stockpiles to adjust to a new normal,” Scott said in a note Friday.

(Written by Joe Ryan and Tim Loh)

Comments